Love and ledgers: making sense of income gaps in modern relationships

Sequel of the movie "Thor: love and thunder", "Love and ledger" talks about how Thor learns to manage his finances and tax returns across multiple planets. Good luck managing interplanetary tax treaties!

Although that could definitely-maybe be an interesting plot, I'll talk about something quite different today: money and relationships.

Conflicts about money and finances can be particularly destructive for both the quality and longevity of relationships. In fact, nearly half of all couples argue about money regularly, and for 25% it's their biggest relationship challenge. Some research indicates finances were the primary reason for conflict in 40% of disagreements in long-term relationships. But here's what nobody tells you - it's not really about the money. It's about what the money means. As some studies suggest, subjective perceptions of financial matters can be more important for marital harmony than objective economic status.

Fun fact: Household bankruptcy is a serious issue. In 2023, the U.S. alone saw over 750,000 bankruptcy filings, a 23% increase from the prior year. Key contributors include excessive debt - U.S. household debt topped $17 trillion in 2023 - medical expenses (accounting for nearly 66.5% of U.S. filings ), job loss, and low savings.

Before you can manage income gaps, you need to know what you’re really dealing with. It’s more than just comparing paychecks - it's about how those financial differences feel and what they mean in the relationship.

What Is income disparity, really?

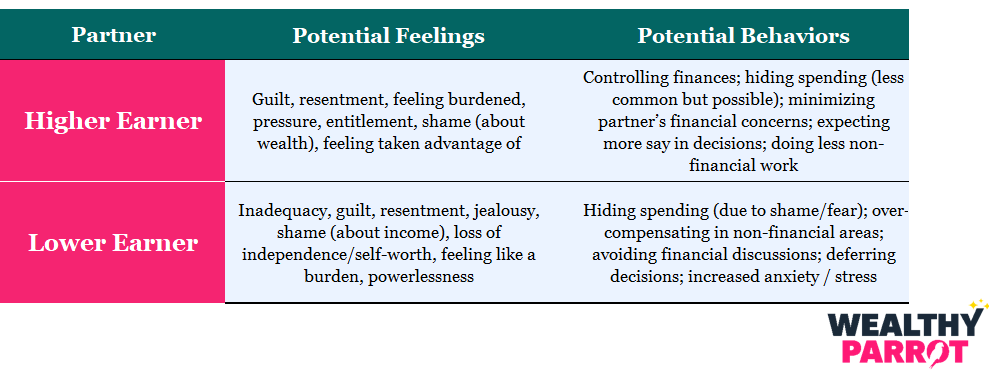

At its core, income disparity means one partner earns - or has - significantly more money than the other. But the emotional weight of that difference matters just as much as the numbers. It can show up as guilt, resentment, shame, or pressure, especially if one person feels like they’re not pulling their weight or the other feels overly responsible. The key issue isn’t always “how much” one earns - it’s how that gap plays out emotionally and practically in the relationship.

Researchers Peetz, Meloff, and Royle (2023) found that financial conflicts often boil down to two overarching dimensions: "concerns about fairness" and "concerns about responsibility". If one partner perceives the other as financially irresponsible, or if contributions feel unfair, that's when the real trouble brews-

Recent research studying couples in China found something fascinating: 57.93% of couples had completely different perceptions about their partner's financial planning abilities. That's more than half! The same study confirmed that the greater the perceived discrepancy in financial planning, the lower the marital satisfaction.

Income differences show up in many ways, and they’re not always obvious. A few common examples:

- One partner is the main breadwinner while the other focuses on caregiving, freelancing, or part-time work.

- One is temporarily or permanently unable to work due to health issues.

- A sudden change, like a job loss, shifts the financial balance.

- Both earn similar salaries, but one has inherited wealth - or significant debt.

Even when take-home pay is close, the overall financial picture can feel uneven. And when that imbalance starts to affect power dynamics, stress levels, or sense of fairness, it becomes a relationship issue - not just a money one.

Fun Fact: In Germany, couples with children under 16 have an average gender wealth gap of €36,000, compared to €20,000 for childless couples. It's not just about income - it's about how life events compound financial disparities over time.

Gender roles, social norms, and income expectations

Money is loaded with meaning, especially when you factor in cultural expectations about who should be earning what. Even today, a lot of couples are navigating financial realities with one foot stuck in outdated gender norms.

For example, there’s still a strong societal script that casts men as the “providers.” So when a woman earns more, it can disrupt that narrative - and not always in a way that feels empowering. Research shows that men who strongly identify with traditional masculinity may feel especially unsettled in relationships where their female partner out-earns them. It's not just about income; it’s about what that income represents in terms of identity, power, and societal validation.

In these cases, income differences become emotional flashpoints. A woman might feel frustrated or disappointed if she sees her partner as not living up to the traditional “protector/provider” role. Meanwhile, a man earning less might wrestle with shame, even if the relationship is otherwise loving and supportive. It’s less about money, and more about what it means - to both partners.

Fun fact: until 1974, a married woman in the UK needed her husband's permission to open a bank account, and even single women couldn't apply for a loan without their father's signature. This changed in 1975 with the Sex Discrimination Act.

Here’s another twist: even when women are the primary earners, they still tend to do more housework and caregiving. This creates a “cultural lag” - where financial progress isn’t matched by progress in how domestic labor is divided. That can leave women feeling overextended and underappreciated, while men may feel unsure about how to contribute in ways that still align with their sense of purpose or identity.

And when it comes to public perception? Many still believe that most men prefer to earn more than their wives. Women’s preferences are more flexible, but even then, social pressure can muddy the waters. From an evolutionary psychology angle, some researchers suggest that men may be more sensitive to economic inequality when dating or marrying, possibly because of competition or concerns about future household stability. Women, on the other hand, might be more open to status differences if it means upward mobility.

All of this makes one thing crystal clear: when it comes to money in relationships, we’re not just managing budgets - we’re managing a legacy of social expectations. Navigating income gaps means unpacking not only what the money looks like, but also what it symbolizes in a relationship built on love, equality, and shared respect.

The wealth vs income distinction

Here's something most people don't realize: income and wealth are only moderately correlated. You can have two couples with the same household income but vastly different wealth situations. One might have inherited assets or existing savings, while the other is starting from scratch or dealing with debt. For most households and individuals, their self-occupied homes are the most significant wealth component in their portfolios.

This matters because wealth provides advantages that go beyond labour income:

- It's a safety net for rainy days.

- It can be used as collateral for investments.

- It generates its own returns over time.

- It can be transferred to the next generation.

- It often gets better tax treatment than earned income.

Fun fact: In most OECD countries, wealth inequality is about twice as high as income inequality. So when we're talking about couple dynamics, we're really dealing with multiple layers of financial complexity

The impact of money on relationship dynamics

As you have probably guessed by now, income gaps often come with power shifts - sometimes obvious, sometimes subtle. The partner who earns more may start taking the lead in financial decisions, which can unintentionally sideline the lower earner. This imbalance can leave one partner feeling unheard or undervalued, especially if there's already tension around traditional gender roles. Common themes in severe financial conflicts include arguments over "unfair relative contributions," "who pays for joint expenses," "discrepant financial values," "one-sided financial decisions," and "perceived irresponsibility".

Money problems are one of the top reasons couples argue - and break up. Add an income gap, and the pressure often multiplies. Worrying about bills, future plans, or who’s “pulling their weight” can ignite stress that affects every part of the relationship.

The bottom line? Unspoken power dynamics and financial stress are two of the most silent - but significant - relationship killers. The key is to bring those conversations out into the open, with honesty and empathy.

Talking openly about money - and what it means emotionally - can lead to stronger communication, clearer shared financial goals, and a better understanding of each other’s values and pressures. Instead of letting the income gap drive a wedge, many couples use it as a springboard for growth. They learn to value each other's contributions more fully, whether financial or not, and create a more balanced and resilient partnership.

But let's change gear a bit and put on our financial glasses, Wealthy Parrot is a personal finance blog after all. Kind of. Definitely.

Managing money together when incomes aren’t equal

When one partner earns more than the other, managing finances as a team takes extra thought, care, and cooperation. But with the right strategies - and a commitment to fairness - it’s absolutely doable. Here's how couples can make it work.

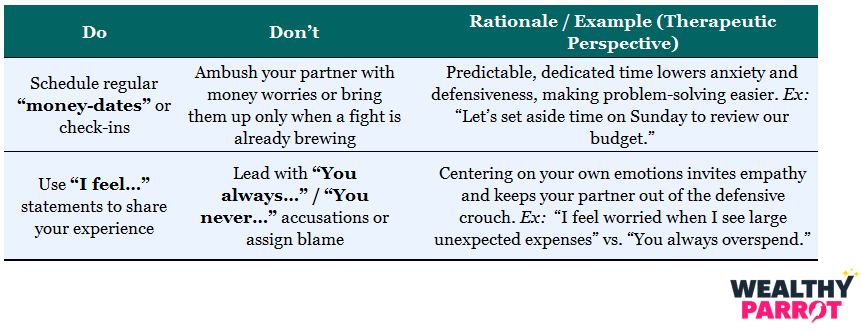

Start with the most important tool: honest conversation

If there’s one non-negotiable in managing money together, it’s open, judgment-free communication. Talking honestly about income, spending, savings, and financial values is the foundation for everything else. Money can carry emotional weight, especially if you and your partner grew up with different financial norms. That’s why creating a safe, respectful space to share is so critical. Try setting regular “money dates” to check in - talk about current expenses, future goals, or just how you're both feeling about your financial setup. When both partners are transparent and feel heard, it becomes easier to build trust and avoid resentment.

Build a shared vision for the future

Once you're talking openly, it's time to get aligned on goals. Start by discussing your individual dreams - maybe one of you wants to pay off loans, while the other is saving for a career pivot. Then shift to shared goals: travel plans, buying a home, starting a family, or preparing for retirement. The key is making sure both voices matter, even if one income is larger. Setting priorities together helps keep things fair, balanced, and focused on teamwork - not competition or control. Financial planning becomes less about "who earns what" and more about "what we’re building together."

Budgeting that feels fair (even when incomes aren’t equal)

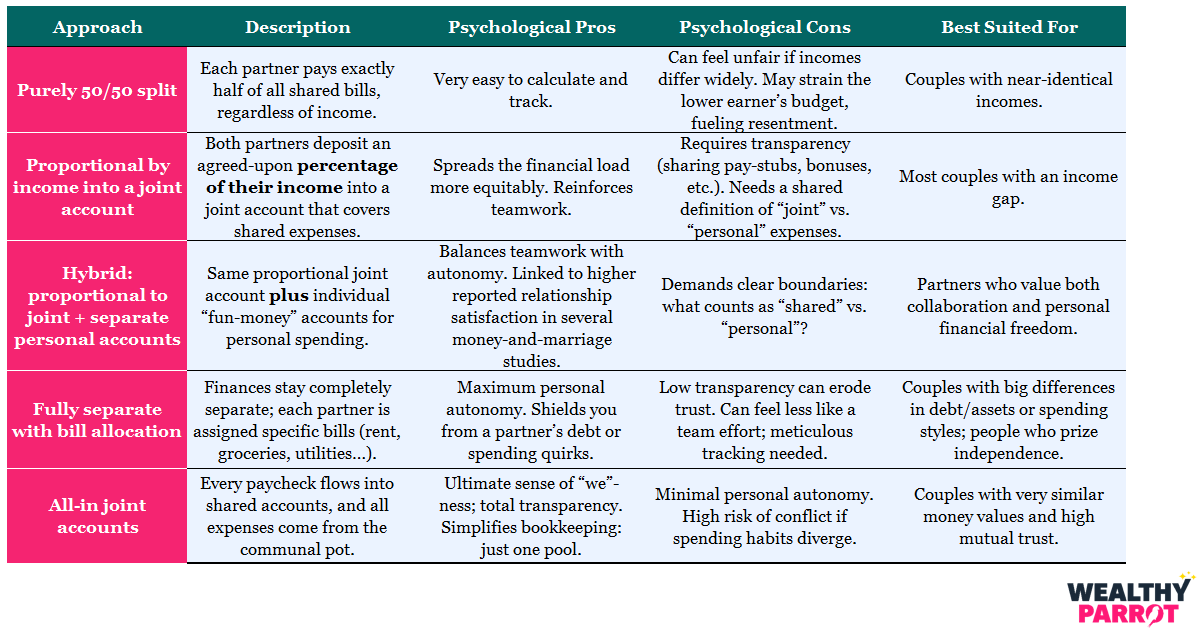

A good budget is more than just numbers—it’s a tool that helps couples stay on the same page, avoid financial strain, and build a future together. For couples with income gaps, fairness is key. That means ditching the one-size-fits-all approach and choosing systems that work for both partners.

It might seem “fair” to split everything 50/50, but if one person earns significantly less, that can quickly feel overwhelming and unfair. They may end up contributing most of their paycheck just to keep up, with little left for themselves. A smarter option? Proportional contributions. This means each person pays for shared expenses based on what they earn. For example, if one partner makes 60% of the total household income, they contribute 60% of the bills. It’s still teamwork - but tailored to your reality.

Use the 50/30/20 rule as a starting point

This popular rule suggests splitting combined after-tax income like this:

- 50% for needs (rent, groceries, bills)

- 30% for wants (fun stuff like dining out or streaming)

- 20% for savings and debt

This framework is a helpful guide, but it’s not set in stone. Adjust the percentages to fit your life - especially if you’re dealing with debt, planning for kids, or working with very different salaries. The key is reviewing your budget regularly, especially when something changes (new job, baby on the way, surprise expenses).

No matter how you structure it, a budget should work for both of you - not just one.

Fun Fact: Mathematical research on a "One-Third Rule" (splitting income equally between debt repayment, savings, and living expenses) suggests it can reduce bankruptcy risk by 20-30% compared to less structured approaches. However, for couples with income disparities, the proportional approach often feels more equitable as it directly accounts for different earning capacities.

Joint or separate? Finding the right way to manage accounts

When it comes to managing bank accounts as a couple - especially with income differences - there’s no one-size-fits-all solution. What works best depends on your personalities, financial habits, trust levels, and goals as a team. Here are the three most common setups:

1. All-in (fully merged accounts)

In this model, all money goes into joint accounts. Bills, savings, and spending are all shared. This setup can feel super unified and works well for couples who share similar spending habits and have a high level of trust. Some research suggests having a joint bank account correlates with fewer financial problems. But it requires total transparency - and it may feel a bit restrictive if either partner values independence.

There are the two other non-trivial aspect to consider. First, what if your account gets compromised? Due to either a major cyberattack, that email you should have not opened or simply some issues with the bank? Also, what if the assets of your partner get frozen due to a lawsuit? Even if you always behave according to law, issues can happen, and in that case having separate accounts (and different banks) will allow you to manage better expenses and money until all is fixed.

2. Totally separate

Each person keeps their own accounts and manages their own money. Shared bills are divided - either 50/50 or based on income. This method can be useful if one partner has debt, owns a business, or simply prefers more control over their finances. It also helps maintain a sense of autonomy, but can sometimes make teamwork feel more transactional.

Fun fact: Two-thirds of American married different-gender couples put all of their money together, compared with 50% of married men partnered with men and 45% of married women partnered with women.

3. The hybrid model

This is a popular middle-ground option. Couples open a joint account for shared expenses like rent, groceries, and utilities - funded proportionally based on income. At the same time, each person keeps a separate account for personal spending and savings. This system helps keep things fair while also preserving a sense of independence. It’s especially helpful for income-uneven relationships, giving both partners shared responsibility and personal freedom. In fact, research shows that couples using this hybrid approach often report higher relationship satisfaction.

Bottom line? The way you manage your accounts should reduce stress - not add to it. The right system supports both your finances and your emotional well-being.

Debt and savings: tackling the big picture together

When it comes to building a solid financial future, managing debt and saving wisely are two major pillars - and both are even more important in relationships with income gaps.

Debt: face it together

Start with full transparency about any existing debts - student loans, credit cards, car payments, you name it. Then decide, as a couple, how to handle them. Some options:

- Each partner handles their own debt.

- The partner with less debt covers more daily expenses so the other can focus on repayment.

- Tackle the debt together, especially if it’s tied to shared goals or happened during the relationship.

Prioritize high-interest debt first - it saves money and stress in the long run.

Fun fact: as many as 41% of American adults admit to hiding accounts, debts or spending habits from their spouse or partner. Even more shocking? 32% of Americans are keeping a financial secret from their partner, despite 75% reporting they are happy in their relationship.

Savings: build it brick by brick

Aim to save at least 20% of after-tax income when possible, and start with an emergency fund that covers 3-6 months of living expenses. Automating savings (like transfers on payday) makes the habit stick. Use joint savings accounts for shared goals - home, travel, a new car - while also discussing how each person is saving for retirement. Even if incomes differ, both partners should have a path to financial security. True fairness means more than splitting the rent. It’s about designing a system that reflects your realities-like helping a partner burdened with student debt or adjusting for who can save more at a given time.

Investing and planning for the long haul

Once your day-to-day finances are solid, look ahead. Investing together means aligning on long-term goals, risk tolerance, and timelines. You might approach investing differently - one of you might love stocks, while the other prefers to play it safe. That’s okay. A financial advisor can help you find middle ground and build a diversified portfolio that balances growth and security. Max out retirement accounts if you can, especially when there’s employer matching - it’s free money. And agree on the big stuff: when you want to buy a home, retire, or hit major life milestones. Shared vision = shared motivation.

Taxes, insurance, and the paperwork that matters

Beyond budgeting and saving, there are some big-picture logistical areas - like taxes and insurance - that can make a real financial difference for couples, especially when incomes are unequal.

Taxes: filing smart

If you’re married, filing taxes jointly can sometimes work in your favor - especially if there’s a big gap between your incomes. The lower earner’s income can help bring down the overall tax rate for the higher earner, potentially creating a “marriage bonus.” But joint filing isn’t always the best choice. It’s worth running the numbers both ways - “married filing jointly” vs. “married filing separately” - to see which saves you more. Tax software can help, or better yet, consult a tax pro. Tax regimes can influence whether couples benefit from keeping finances separate or joint.

Insurance: protect what matters

Marriage is a good time to review your insurance policies. That includes:

- Health insurance - Should you share a family plan or keep separate coverage?

- Life and disability insurance - Are your beneficiaries up to date? Do you have enough coverage?

Compare costs and benefits, especially if one partner has better employer-sponsored options.

For couples with more complex finances - like owning a business, having kids from previous relationships, or significant personal assets - it might be wise to discuss a prenuptial agreement. It’s not about lack of trust; it’s about protecting both partners and setting clear expectations.

Keep reviewing, keep talking

Your financial setup isn’t “set it and forget it.” Life changes - jobs shift, families grow, priorities evolve. Regularly revisit your budget, account structure, savings goals, and investment strategy together. These check-ins are more than financial tune-ups - they’re relationship maintenance. A flexible, evolving financial plan helps ensure that money supports your life, not the other way around. European research tracking couples over decades shows that major life transitions - union formation, having kids, divorce, inheritance - all significantly impact wealth accumulation patterns

Fun fact: the phrase “what’s mine is yours” first appeared in English literature in Shakespeare’s Measure for Measure (1604)… but even back then, the Duke made sure to keep the royal treasury under separate management!

Recognizing non-financial contributions

Income is just one way to contribute to a relationship. Caregiving, household work, emotional labor, and logistical support are all invaluable. It’s especially important for the higher earner to actively recognize and appreciate what their partner brings to the table - whether that’s raising children, managing the home, or providing emotional stability.

By valuing all forms of contribution, couples create a balanced partnership where no one feels invisible or undervalued - and where power isn’t tied to income alone.

When to see a professional

Despite a couple's best efforts, navigating income disparity can sometimes become overwhelming, leading to persistent conflict, emotional distress, or a stalemate in financial decision-making. In such situations, seeking professional help is not a sign of failure, but rather a proactive step towards improving the relationship and financial well-being

Conclusion

Income differences in relationships touch more than just finances - they impact emotions, identity, and the balance of power. Left unaddressed, these gaps can create stress and miscommunication. But with honest dialogue and intentional strategies, couples can turn these challenges into opportunities for deeper connection.

The foundation is open, empathetic communication. When partners talk openly about their financial pasts, goals, and fears, they build trust and strengthen their bond. Practical tools - like proportional budgeting, hybrid bank accounts, and shared goal-setting - make financial collaboration feel fair and manageable.

Equally important is recognizing non-financial contributions. Caregiving, emotional support, and household management are essential forms of value, especially in relationships with income gaps.

When needed, professional support can help couples navigate tough spots. Ultimately, income disparity doesn’t have to divide - it can unify, if approached with respect, teamwork, and love.