The lifestyle inflation trap: why your raise isn't making you richer

Getting that promotion probably won't make you wealthy. In fact, it might be doing the exact opposite.

Research shows that salary increases averaged 1.7% globally in 2024, yet only 30% of employees express satisfaction with their compensation. The highest income earners increased their spending by 6.7% in a single year, with the biggest jumps in dining out (+8%) and transportation (+7%).

Meanwhile, that seemingly innocent $200 monthly lifestyle boost after your last raise? It's costing you $168,800 over 20 years when you factor in opportunity costs.

This isn't about living like a monk - it's about understanding why our brains sabotage our wealth-building efforts, and what we can do about it.

What is lifestyle inflation? The psychology behind your spending habits

Lifestyle inflation happens when your spending rises to match your income increases. That celebratory dinner becomes a weekly habit, the reliable car gets replaced with a luxury SUV, and the starter apartment gives way to a bigger place in a pricier neighborhood.

Here's what's happening in your brain: every time you upgrade your lifestyle, you get a temporary happiness boost. But your brain quickly adapts to this new normal through "hedonic adaptation" - suddenly your fancy new apartment feels ordinary, and you're eyeing the next upgrade.

The newest research has updated the old "$75,000 happiness plateau" idea. 85% of people experience rising happiness up to $500,000 annually, but those 15-20% who plateau around $100,000 are often the ones chasing happiness through aggressive lifestyle inflation. People feel happiest day-to-day when earning between $60,000-$75,000 annually. Beyond that, daily happiness doesn't improve much, even though "life satisfaction" might continue climbing.

Your brain literally treats shopping like a drug. When you're about to buy something, your brain releases the same dopamine as it does with cocaine. The anticipation is often more pleasurable than actually owning the item - which explains why so many impulse purchases end up gathering dust.

Fun Fact: Your brain releases the same dopamine when you're about to buy something as it does when you actually use cocaine. The anticipation of the purchase is often more pleasurable than actually owning the item.

The Psychological biases that sabotage your wealth

Several powerful psychological forces work together to fuel lifestyle inflation:

Self-Licensing: your brain gives you permission to spend after you've worked hard. "I deserve this $3,000 watch because I worked 70-hour weeks!" It's like your hard work becomes a moral get-out-of-jail-free card for financially questionable decisions.

Effort justification: the more effort something took to achieve, the more valuable we think the reward should be. Went through medical school? Survived law school? Your brain inflates the value of your salary and whispers that you "deserve" to live accordingly.

The Diderot effect: one elegant purchase makes everything else look shabby. Buy a beautiful couch? Suddenly your coffee table looks cheap. Upgrade the table? Now the lamp seems outdated. Before you know it, you've redecorated your entire living room because of one "small" purchase.

Mental accounting: you treat money differently based on its source. Hard-earned salary gets carefully budgeted, but bonuses become "fun money" blown on frivolous purchases, even with outstanding debt.

Projection bias: when excited about a potential purchase, you project that excitement into the future, overestimating long-term joy. That expensive gadget feels life-changing... until it's unused in a drawer three months later.

These biases create a vicious cycle: the initial "reward" purchase becomes your new normal, requiring even bigger rewards to feel special.

The devastating financial impact

Let me show you exactly what lifestyle inflation costs with a real-world scenario:

The $1,042,000 mistake: consider a software engineer who gets a $50,000 raise and increases spending by $2,000 monthly. Seems reasonable, right? Wrong. After taxes, the actual take-home increase is only about $30,000, so they're spending 80% of their real raise. Over 20 years, this "modest" upgrade costs over $1,042,000 in opportunity costs.

Here's the brutal math: That $2,000 monthly lifestyle inflation doesn't just cost $2,000 × 12 × 20 = $480,000 in direct spending. When you factor in lost investment returns at 7% annual growth, the true opportunity cost explodes to over $1,042,000. They didn't just lose the $480,000 spent - they lost the chance to have over a million dollars.

A mistake that can push your retirement away

Your retirement timeline depends on two factors: how much you need to accumulate (based on your expenses) and how fast you're accumulating it (your savings rate). When you get a raise, spending too much of it hurts you on both fronts.

You need to save at least 50% of every future raise to maintain your current retirement timeline. This is because:

- It keeps your savings rate stable or improving - If you were saving 20% before, and you save 50% of a raise while spending the other 50%, your overall savings rate stays roughly the same or improves slightly.

- It prevents lifestyle inflation from derailing your plan - The biggest retirement killer isn't market crashes; it's gradually increasing your spending and thus the amount you need to accumulate.

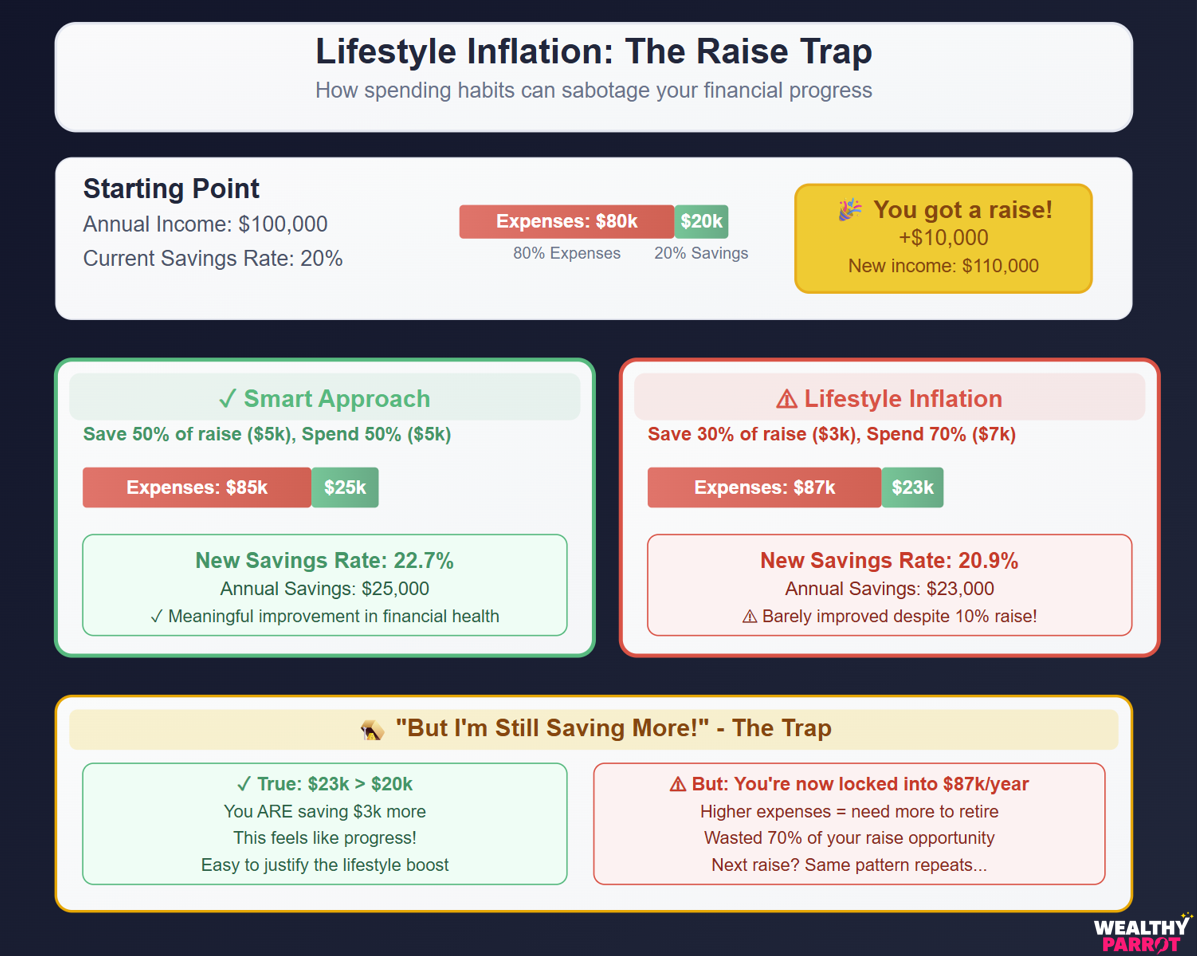

Spend more than half, and you're literally pushing retirement further away. Currently saving 20% of income? You can spend up to 50% of your next raise without delaying retirement. Spend 70%? Congratulations, you just added years to your working life. Too complicated? Let's see with an example:

Let's say you make $100k and save 20% ($20k annually):

- Current expenses: $80k

- A $10k raise brings you to $110k

If you save 50% of the raise ($5k) and spend 50% ($5k):

- New expenses: $85k

- New savings: $25k

- New savings rate: 22.7% (improved!)

But if you spend 70% of the raise ($7k):

- New expenses: $87k

- New savings: $23k

- New savings rate: 20.9% (barely changed, but you need more money to retire)

Important note: It's absolutely okay to celebrate raises and promotions - you've earned it! The key is making it a one-time, reasonably-priced reward rather than a permanent lifestyle upgrade. Got a $10,000 raise? Celebrate with a $1,000 vacation or special purchase, then direct the other $9,000 toward your future self through investments and savings.

This principle holds globally - UK wages grow 4-5% annually, but similar lifestyle inflation patterns emerge worldwide.

Fun Fact: If you start investing $500 monthly at age 25, you'll have more at 65 than someone investing $1,000 monthly starting at age 35. The 10-year head start beats doubling the amount - that's the compound interest power lifestyle inflation steals.

The subscription vampire problem

The average US consumer spends $118 monthly on subscriptions but estimates only $86.

The international picture is equally concerning:

- UK households: £58 monthly

- Australian households: $55 AUD monthly average

- Global subscription market: expected to hit $6.4 trillion by 2030

Fun Fact: the average American has 12 paid subscriptions but thinks they only have 9. We literally forget about 25% of the money automatically leaving our accounts.

Studies such as one from CNET or even YouGov, report that American adults are wasting money every year on subscriptions they don't use, with Gen Z being the most forgetful generation, with their unused subscriptions costing them an average of $23 per month, or $276 annually.

Just a $75 monthly subscription increase costs $21,069 in opportunity costs over 20 years when you factor in 7% compound interest.

Professional spending traps: how your career sabotages your wealth

Different careers create distinct lifestyle inflation patterns driven by compensation structures, workplace culture, and professional expectations:

Legal professionals: BigLaw associates starting at $225K typically see 50-100% spending increases in year one. The progression from shared law school apartments to luxury studios ($3,000-6,000 monthly) happens fast. Professional image costs alone: $15K-30K annually for appropriate attire, networking events, and the "right" car for client meetings.

Medical professionals: Four physicians with identical $300,000 salaries showed vastly different wealth outcomes. Dr. Anderson, spending $80,000 annually, achieved financial independence in 11 years. Dr. Davidson, spending $200,000 annually, remained trapped in "golden handcuffs" despite identical income. When one physician upgraded mid-career from $120,000 to $200,000 spending, his required retirement nest egg increased from $3 million to $5 million.

Technology workers: Face unique challenges with stock compensation. Many base spending on peak stock valuations, creating vulnerability during downturns. The 2022 tech correction forced lifestyle adjustments as RSU values dropped 40-70%, demonstrating how lifestyle inflation funded by variable compensation creates financial fragility.

Finance professionals: Investment banking culture practically requires luxury spending - networking, entertainment, the right watch, exclusive memberships. These "professional image" costs reach $20K-40K annually.

The professional costuming tax: Across all industries, the hidden costs add up. Work clothes, impressive briefcases, networking dinners, cars appropriate for company parking lots - these aren't just personal choices but career investments that eat into wealth-building capacity.

This pattern repeats globally - profession-based peer groups create powerful spending norms that transcend income levels. When everyone in your circle drives luxury cars and lives in expensive neighborhoods, those choices feel necessary rather than optional.

What wealthy people actually do differently

According to a study done by researchers at Experian Automotive (and published on Forbes) 61% of households earning $250K+ don't drive luxury brands - they drive Toyotas, Hondas, and Fords.

The Ford F-150 pickup truck is the most popular vehicle among Americans earning over $200K annually. Warren Buffett has lived in the same modest Omaha home for 50+ years. Mark Zuckerberg drives a Honda Fit. Jeff Bezos drove a Honda Accord well after becoming a billionaire.

90% of millionaires drive cars costing less than $75K, while 86% of people driving "prestigious" brands aren't actually millionaires.

The lesson? There's a massive difference between being "rich" (high income, high spending) and "wealthy" (accumulated assets providing freedom).

The lifestyle lock-in matrix: avoid financial quicksand

Not all spending is equal. Some upgrades are financial quicksand - once you step in, escape is nearly impossible.

- Green zone (low cost + easy to reverse): coffee upgrades, streaming services

- Yellow zone (low cost + hard to Reverse): homeowners association fees, private school commitments

- Orange zone (high cost + easy to reverse): luxury vacations, designer clothes

- DANGER ZONE (high cost + hard to reverse): bigger mortgages, luxury car leases

Counterintuitive truth: A $10K luxury vacation (Orange Zone) is less financially dangerous than a $300/month mortgage increase (Danger Zone). The vacation is one-time; the mortgage is a 360-month commitment restructuring your entire financial life.

The 2x Rule for strategic splurges: want that expensive gadget or luxury experience? Fine, but for every dollar you spend, invest an equal amount. Want a $2,000 vacation? Great - put $2,000 into your investment account first. This reframes splurges from guilty indulgences into financially responsible decisions that still move you toward wealth-building goals.

Before any major purchase, run it through this wealth-preserving framework:

- The True cost test: What's the real total cost including maintenance, insurance, taxes, opportunity cost, and your time? That $50,000 car might actually cost $150,000 when you factor in everything over its lifetime.

- The values alignment test: Is this purchase deeply aligned with your core values, or are you buying it because of social pressure, status anxiety, or stress relief? Be brutally honest.

- The opportunity cost test: If you invested this money instead at 7% annual returns, what would it be worth in 20 years? Is this purchase really worth sacrificing that future wealth?

- The flexibility test: Using the Lock-In Matrix, does this purchase increase your fixed costs and reduce your financial flexibility? Will it chain you to your current job, location, or lifestyle?

If a purchase fails even one of these tests, it's probably a wealth destroyer in disguise.

Behavioral Safeguards

The 24-48 Hour Rule: Implement mandatory waiting periods for discretionary purchases over predetermined amounts ($500, $1,000, etc.). This simple delay often prevents impulse buying driven by temporary emotions.

Value-Based Budgeting: Regularly review spending against core personal values. Expenses that don't align with what truly matters to you become obvious targets for reduction.

Social Environment Management: Curate your social circle to include people who share similar financial values rather than those who encourage competitive consumption. The "reference group" effect on spending is powerful and largely unconscious.

Smart spending priorities: what actually makes you happy

You can prioritize to spend in categories that will make you happy - backed by science.

Buy experiences, not things: That trip to Japan will bring you joy for years through memories and personal growth. That expensive watch? You'll stop noticing it in three months due to hedonic adaptation.

Spend on others: Gifts, charity, and spending on friends and family consistently provide a bigger happiness boost than spending on yourself. This effect works across cultures and even applies to children.

Buy time: Spending money to save time (housecleaning, meal delivery, outsourcing dreaded tasks) increases life satisfaction regardless of income level. Time is the ultimate luxury.

Many small pleasures beat few large ones: because of hedonic adaptation, frequent small joys (weekly coffee dates with friends, small hobby purchases) provide more lasting happiness than infrequent big purchases (expensive home renovation).

Match your personality: people who make purchases that align with their psychological profile report higher life satisfaction than those whose spending doesn't fit their personality - this effect is even stronger than the impact of total income on happiness.

The bottom line: your wealth or your lifestyle

Lifestyle inflation is wealth destruction with better marketing. But this isn't inevitable. You don't need superhuman willpower or a monk-like existence. You just need to understand that lifestyle inflation is a systemic challenge requiring systematic solutions.

The secret that authentic wealth builders know: your wealth isn't determined (only) by how much you earn - it's determined by how much of your income growth you resist converting to lifestyle inflation.

The choice is stark and binary: impressive lifestyle or impressive net worth. Research consistently shows you can't optimize for both simultaneously.

In a culture that screams "treat yourself" every time you get ahead, the real rebellion is maintaining disciplined lifestyle choices regardless of earning power. While everyone else upgrades their way to financial mediocrity, you'll be quietly building actual wealth that provides genuine freedom and options.

The professionals who break free from lifestyle inflation don't just build bigger bank accounts - they build bigger lives. They gain the ultimate luxury: choice. Choice in work, location, relationships, and how they spend their most precious resource - time.

Your next raise is coming. The question isn't whether you'll get more money. The question is: what will you do with it?🦜