The mouse trap: how Disney built a $91 billion empire

Hey there, savvy investors! Pop quiz time: What's Disney's biggest money-maker? If you said "movies," congratulations - you just fell into the same trap as 99% of people. Plot twist: Disney's theatrical films contributed less than 10% of their whopping $91.4 billion revenue in 2024. Surprised? You should be!

Here's the kicker: Disney's theme parks alone raked in $34.1 billion - that's more than triple what the entire global box office earned. Meanwhile, everyone's arguing about whether the latest Marvel movie was good enough while Disney executives are literally counting money from 40+ different revenue streams.

For anyone still thinking Disney is a movie company, want to know exactly how tiny the movie business really is? Disney's "theatrical distribution licensing" generated just $2.27 billion in 2024 - that's a pathetic 2.5% of their total $91.4 billion revenue. To put this in perspective: theme parks generate 15 times more revenue than movies! Even when you look at profits instead of just revenue, the entertainment segment (which includes ALL of Disney's movies, streaming, and TV) generated $3.92 billion in operating income. The theme parks and experiences division? $9.27 billion in operating income. That's more than double the profit from a single business segment compared to their entire entertainment empire.

Think you know Disney? Think again. This isn't just a entertainment company - it's the world's most sophisticated money-printing machine disguised as a mouse. And once you understand how this flywheel really works, you'll never look at "entertainment" stocks the same way again.

The great Disney deception: movies are just expensive commercials

Picture this: It's 1929, and Walt Disney is facing financial struggles when he signs a contract with a small New York stationery firm for a mere $300, granting them rights to sell schoolchildren's writing pads featuring Mickey Mouse. That seemingly tiny deal opened his eyes to the vast potential of licensing, leading to agreements like Mickey Mouse watches that initially sold a million units per year and contributed 10% of the company's income for a decade. Little did he know, that $300 licensing deal would become the blueprint for the most profitable character portfolio in human history. Fast-forward to today, and Disney isn't in the movie business-they're in the "turn movies into money machines" business.

Understanding how Disney makes money reveals one of the most sophisticated business models in the entertainment industry. While most people think they know Disney's revenue breakdown, the reality is far more complex and profitable than meets the eye.

The mind-blowing reality is that Disney is the #1 global licensor, generating $61.7 billion in retail sales from licensed merchandise in 2022 alone. That's roughly five times larger than Disney's entire box office revenue. Let that sink in for a second.

But wait, it gets better (or worse, depending on how you look at it). Remember when everyone was obsessing over whether Frozen was any good? While critics debated character development, Disney was laughing all the way to the bank with what might be the most profitable franchise in entertainment history.

Frozen earned $1.2 billion at the global box office - impressive, right? Wrong. That's actually the smallest slice of the Frozen money pie. The total Frozen franchise value is estimated between $13.9 and $14.1 billion. We're talking about a nearly $14 billion empire built around a singing ice queen.

Frozen merchandise sales alone generated $10.5+ billion. That means parents worldwide spent nine times more on Elsa dolls, Olaf backpacks, and "Let It Go" karaoke machines than they did on movie tickets. $10.5 billion in toys and t-shirts versus $1.2 billion in box office. The movie wasn't the product - it was the world's most expensive commercial for the real money-makers.

The Cars franchise tells an even more bonkers story. Despite critics calling it Pixar's "weakest" series, it generated over $10 billion in merchandise sales in its first five years. The box office performance? Almost irrelevant at $1.4 billion. Disney literally kept making Cars sequels not because they were cinematic masterpieces, but because kids couldn't stop buying the toys!

The Lion King provides another perfect example: the film generated nearly $1 billion in profit, with a massive portion attributed to merchandising sales that continued long after the movie left theaters. It's the gift that keeps on giving - quite literally.

The Encanto lesson: when magic doesn't translate to merchandise

Not every Disney hit follows the Frozen formula, and Encanto is the perfect case study in how cultural success doesn't always equal commercial domination. The film was a streaming sensation, generating 27.4 billion minutes viewed on Disney+ and producing a multi-platinum soundtrack that had parents everywhere humming "We Don't Talk About Bruno."

But here's where it gets interesting: Encanto earned $261.3 million at the global box office on a $150 million budget - respectable, but not exactly Frozen numbers. More telling? Its merchandise sales, while substantial, never reached the stratospheric levels of the ice queen phenomenon.

The reason reveals a crucial insight into Disney's business model: what entertainment analysts call the "toyetic" factor. Frozen gave us Elsa - an iconic, visually striking character that's instantly recognizable and perfect for toys. Encanto, brilliant as it was, centered on complex family dynamics and an ensemble cast. Try explaining Mirabel's emotional journey to a 4-year-old shopping for toys, versus just pointing at the sparkly ice princess.

Disney reportedly underestimated Encanto's breakout potential, leading to an initial "lack of merch" that fans complained about. It's a rare strategic miscalculation from the merchandising masters, proving that even Disney can't always predict which stories will capture the cultural zeitgeist. The lesson? Creating emotional connections is Disney's superpower, but translating those connections into billion-dollar toy sales requires very specific types of characters and stories.

The merchandising money machine that would make Bezos jealous

Disney figured out how to create emotional connections with fictional characters, then monetize those feelings across decades. Mickey Mouse - a drawing from 1928 - remains the #1 licensed character globally nearly a century later. Talk about return on investment!

The math is staggering. Disney typically receives 8-10% licensing fees from total retail sales, meaning they earn money without manufacturing, inventory, or distribution costs. Pure profit from intellectual property. Star Wars drives $2-3 billion in annual retail sales globally, and Disney captures a healthy slice of that action without making a single toy.

Fun fact: Mickey Mouse is 96 years old and still dominates global merchandise sales. The character drives over $3 billion annually in retail sales worldwide - that's more consumer spending than most Hollywood blockbusters generate at the box office!

But here's the genius part: Disney creates characters specifically designed to forge multi-generational connections. Grandparents who loved Mickey pass that love to parents, who pass it to kids. It's like emotional compound interest, except instead of money growing, it's brand loyalty - and that loyalty translates directly into cold, hard cash.

Theme Parks: where psychology meets highway robbery (legally)

If you think Disney's merchandising is impressive, wait until you see their theme park revenue optimization. These aren't just amusement parks - they're customer experience laboratories where Disney tests pricing strategies that would make airline executives weep with envy.

Ready for some jaw-dropping numbers? Magic Kingdom charges up to $199 for single-day admission, using seven-tier dynamic pricing that fluctuates like Uber surge pricing. But that's just your entry fee to Disney's revenue extraction laboratory. The real genius is in the add-ons:

- Individual Lightning Lane: $10-$25 per ride for popular attractions

- Genie+ line-skipping: $15-$39 daily (and here's the kicker: up to 50% of guests buy it)

- Disney Private VIP Tours: Several hundred dollars per hour for the ultimate skip-every-line experience

- Hotels? $150 to $950 per night, commanding 2-3x local market rates just because they slap Mickey Mouse on the towels

Want to know how profitable this strategy is? Genie+ alone generated $724 million in revenue in less than three years. That's nearly three-quarters of a billion dollars from convincing people to pay extra for something they used to get free. It's like charging for air, except people are happy to pay because Mickey Mouse is involved.

The pricing pressure is relentless. A typical four-day Walt Disney World vacation increased by over $1,000 between 2019 and 2024 - and that's before you buy a single souvenir or churro.

Fun fact: Walt Disney World is absolutely massive at 25,000 acres-that's larger than Manhattan (14,500 acres) and about the same size as Paris! You could fit roughly 200 Vatican Cities inside Disney World and still have room for parking lots. It's also the largest single-site employer in the United States, accommodating hundreds of thousands of guests on peak days.

The loyalty these experiences generate is mind-blowing: Walt Disney World has a 70% return customer rate. That means 7 out of 10 people who visit once come back for more punishment... er, magic. Disney's hotels achieve occupancy rates exceeding 90%-among the highest globally-while charging premium prices that would make Manhattan hoteliers jealous.

The beautiful (terrifying?) part is how Disney segments customers while squeezing maximum revenue from each group. Budget families pay $119 and wait in lines. Rich families drop $600+ per person daily for premium experiences. Disney captures the entire demand curve while using the same underlying infrastructure.

And the best part (for Disney?): per-capita spending keeps growing despite higher prices. That's pricing power most companies can only dream about. The result? $9.3 billion in theme park operating income annually - that's 60% of Disney's total operating income from just one business segment.

Fun fact: Disney extracts approximately $200 per visitor at their theme parks before they even buy a souvenir. That's more than most people spend on a nice dinner, and you haven't even gotten to the gift shop yet!

But here's the secret sauce behind those astronomical numbers: Disney's obsessive attention to detail. We're talking about trash cans strategically placed every 27 steps (Walt Disney personally counted), hotel room peepholes positioned at child-eye level, and "Cast Members" (employees) whose individualized, unscripted interactions are often the single biggest factor in guest satisfaction and intent to return. This isn't accidental magic - it's a "rational, muscular, no-nonsense business strategy" disguised as pixie dust.

The theme parks are meticulously designed to immerse guests in these stories, with attention to every detail from landscaping to pavement texture, creating a "living movie" in which guests participate. You're not just visiting an amusement park-you're literally stepping inside the stories you love. That's why people pay $200+ per day and keep coming back for more.

Content as marketing: the $200 Million commercial strategy

Every Disney movie isn't actually a movie - it's a two-hour commercial for everything else Disney wants to sell you. They don't make entertainment; they make marketing campaigns that happen to entertain.

Take Encanto. Limited theatrical release, huge streaming success (27.4 billion minutes viewed on Disney+), which drove massive merchandise sales and justified new theme park attractions. The movie was basically a very expensive trailer for the real money-makers.

Disney's $60 billion, ten-year theme park investment plan specifically targets IP integration. Every new attraction based on recent films - Encanto at Animal Kingdom, Cars expansion at Magic Kingdom - transforms temporary movie success into permanent revenue-generating experiences. Each attraction creates multiple revenue streams: admission fees, merchandise, food, photos, and premium experiences.

It's genius when you think about it: Traditional movie studios make a film, release it, and hope for the best. Disney makes a film, then builds an entire ecosystem around it that generates money for decades.

Disney+: the $1 Billion loss that became a $300 Million win

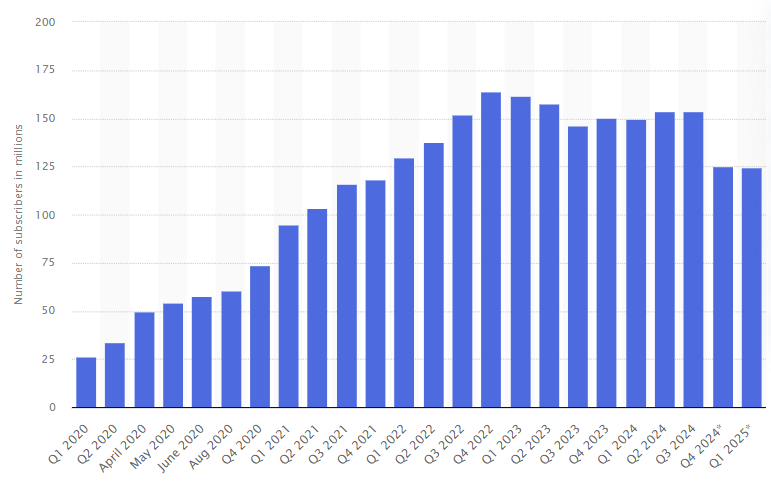

Ready for the most dramatic corporate turnaround story in streaming history? Disney+ went from hemorrhaging $984 million in a single quarter (Q1 2023) to generating $321 million in profit (Q2 2025). That's a $1.3 billion swing in less than two years.

But let's rewind to see just how wild this ride was. Disney+ hit 100 million subscribers in less than two years, absolutely crushing their original goal of 60-90 million by 2024. Success! Then came the reality check: subscriber counts fell from 164 million (end 2022) to 150 million (end 2023) before recovering to 153 million by mid-2024. The culprit? A combination of losing cricket streaming rights in India (goodbye, 1 million subscribers) and aggressive price increases that made budget-conscious viewers say "thanks, but no thanks."

Here's the plot twist: Disney+ average revenue per user hit $7.28 globally (excluding Disney+ Hotstar) in Q2 2024. Disney realized something profound: profitable customers beat vanity metrics every time.

How do you flip a billion-dollar loss into hundreds of millions in profit? You stop playing Netflix's game and start playing your own. Disney abandoned the "growth at all costs" mentality and focused on what actually matters: making money from each subscriber.

The turnaround strategy was surgical:

- Price hikes that actually worked: Instead of losing subscribers, Disney proved they had pricing power

- Ad-supported tiers became the secret weapon: 37% of domestic subscribers chose the cheaper ad-supported option, creating a whole new revenue stream

- Bundle everything: The Disney+, Hulu, ESPN+ trio bundle improved retention and reduced customer acquisition costs

The beautiful part? Unlike Netflix, which must constantly produce new content to keep subscribers, Disney+ is essentially a 24/7 commercial for everything else Disney wants to sell you. Every stream of The Mandalorian is a marketing touch-point for Baby Yoda merchandise. Every viewing of Encanto plants the seed for a future Disney World vacation. Disney even uses its traditional media networks for cross-promotion-ABC runs specials to promote Disney films, creating a seamless marketing ecosystem where every platform feeds every other platform.

Unlike Netflix, which must continually produce new content to retain subscribers, Disney leverages existing IP libraries while using streaming success to justify investments in parks, merchandise, and live experiences. It's the ultimate customer retention tool disguised as a streaming service.

The original land grab: how Disney pulled off history's sneakiest real estate deal

Before we talk about Disney buying Marvel and Star Wars, let's rewind to the OG business masterstroke that made everything else possible. In the 1960s, Walt Disney pulled off what might be the most brilliant real estate con in American history - and it was completely legal.

Picture this: It's 1963, and Walt Disney is flying over Central Florida in his company plane, looking at mile after mile of worthless swampland. Most people saw mosquito-infested marshes. Walt saw the future home of the world's most visited theme park. But here's the problem: if anyone knew Disney wanted this land, prices would skyrocket faster than a Space Mountain launch.

So what did Walt do? He basically became a master of disguise in the real estate world. Working with attorney Paul Helliwell, Disney created multiple shell companies with names that would make you chuckle: "M.T. Lott Real Estate Corporation" (get it? "Empty Lot"?), "Latin-American Development and Management Corporation," and "Reedy Creek Ranch Corporation." They used fake names, rerouted phone calls through New York to avoid suspicion, and bought land through mysterious "mystery clients."

The results were spectacular. Over 18 months of secret operations, Disney quietly acquired 27,400 acres of Central Florida swampland for around $100-120 per acre. That's land that nobody wanted, from sellers who often lived out-of-state and had never even seen their inherited "worthless" property. Many were practically begging to sell!

Compare that to what would have happened if Disney had announced their plans first. Land speculators would have swooped in, prices would have exploded, and Disney's dream might have died before it started. The secret was so well-kept that even Disney's own employees didn't know - the project was called "Project X" and only seven people in the entire company were in the loop.

The scheme finally unraveled when Orlando Sentinel reporter Emily Bavar connected the dots in October 1965, but by then it was too late. Disney had already locked up virtually all the land they needed at bargain-basement prices. Total savings? Potentially hundreds of millions of dollars that could be invested in actually building the park instead of enriching land speculators.

Fun fact: Disney used so many shell companies to secretly buy Florida land that they could have started their own stock exchange. The fake company names included "M.T. Lott Real Estate" (Empty Lot) and "Compass East Corporation"- Walt Disney was apparently as good at dad jokes as he was at business strategy!

This wasn't just smart real estate - it was a masterclass in strategic thinking that would define Disney's approach to business for decades. If you can control information and think three steps ahead, you can control outcomes. And trust me, this lesson applies to way more than just buying swampland in Florida.

The acquisition Hall of Fame: buying revenue multiplication machines

Disney's $60 billion acquisition spree wasn't just smart - it was the greatest intellectual property shopping spree in corporate history. The numbers are so staggering they sound made up:

Marvel Entertainment ($4 billion, 2009):

- Return on investment: 3.3x

- Value created: $13.2 billion

- Translation: Disney turned $4 billion into $13.2 billion in Marvel value

Lucasfilm ($4.05 billion, 2012):

- Return on investment: 2.3-2.9x

- Value created: ~$12 billion

Fun fact: Star Wars merchandise alone generates $1 billion annually, meaning the licensing revenue will pay back the entire acquisition every four years. Forever.

Pixar ($7.4 billion, 2006):

- The deal that started it all, transforming Disney's animation pipeline and creative culture

Combined impact: $25 billion in value creation on an $8 billion investment. That's not just successful corporate development - that's financial alchemy.

But here's what makes these acquisitions pure genius: Disney didn't just buy content libraries. They bought IP-generating machines. When Disney acquired Pixar, they weren't just getting Toy Story - they were getting the culture and talent that could create the next Toy Story and teach Disney's own animators how to do the same. When it bought Marvel, it wasn't just buying Iron Man; it was buying Kevin Feige's proven methodology for building interconnected narrative universes. And when it bought Lucasfilm, it acquired not only a galaxy far, far away but also the world-class technical wizards at Industrial Light & Magic (ILM) and Skywalker Sound.

These acquisitions demonstrate Disney's laser focus on purchasing IP portfolios with cross-platform monetization potential. They don't just buy content libraries; they buy characters that can generate revenue through movies, streaming, theme parks, merchandise, and licensing for decades.

The Disney Flywheel: where everything connects to everything

Every business unit doesn't just generate revenue - it drives revenue for every other business unit. It's like a financial perpetual motion machine.

Movies create emotional connections → Characters drive merchandise sales → Merchandise revenue funds theme park attractions → Theme park visits boost streaming subscriptions → Streaming keeps characters relevant → Relevant characters justify new movies.

The flywheel effect means Disney's competitive moat gets stronger over time rather than weaker. Traditional entertainment companies have to start from scratch with each project. Disney builds on 95+ years of accumulated brand equity with every new release.

What Wall Street actually values (hint: it's not box office numbers)

Financial analysts don't value Disney as a movie company - they treat it like a diversified consumer experiences and intellectual property conglomerate.

The investment thesis boils down to what analysts call Disney's "wide economic moat" - a fancy way of saying "good luck competing with this monster." As Morningstar puts it: "No peer can match the depth of Disney's iconic characters, franchises, or content library."

Translation for normal humans: Netflix can create Stranger Things, but where's their Stranger Things theme park? Apple can spend billions on content, but do they have a century-old mouse that still generates $3 billion in annual merchandise sales?

Here's the plot twist most investors miss: Financial analysts don't value Disney as a movie company. They use sum-of-the-parts analysis that treats content as infrastructure supporting higher-margin businesses.

Disney's $195 billion market capitalization reflects:

- Recurring cash flows from parks operations ($34B+ annual revenue)

- Growing streaming subscriber base with improving unit economics

- Long-term ESPN sports rights and content library value

- Global brand licensing generating perpetual revenue streams

The company's stock price correlates more strongly with parks attendance and per-capita spending than box office performance. When Disney announces theme park expansions, shares often jump more than when they announce new movie slates.

Your investment playbook: spotting Disney-style money machines

Disney's success provides a framework for identifying companies with durable competitive advantages and multiple revenue streams. Here's what to look for:

Durable brands that transcend generations: companies that create strong brand loyalty and emotional connections with consumers across multiple generations possess rare competitive advantages. Disney's brand, rooted in values like quality, innovation, and family, evokes nostalgia and positive feelings that ensure customers keep returning. Look for brands that mean something beyond their products - brands that become part of people's identities and family traditions.

Pricing power that defies gravity: companies that can raise prices ahead of inflation while maintaining customer loyalty possess rare economic moats. Disney's theme park pricing increases consistently outpace inflation while attendance remains stable. Look for businesses where customers complain about prices but keep paying anyway - that's true pricing power.

Multiple monetization channels and "Related Diversification": the strongest businesses don't just have multiple revenue streams-they have related diversification where different business units exploit synergies and feed into each other. Disney leverages its IP through theme parks, resorts, cruises, merchandise, publishing, and various media networks. Look for companies that can generate income from various interconnected sources, reducing reliance on any single product while creating amplifying effects.

Ecosystem effects and cross-selling: the strongest businesses create flywheel effects where success in one area drives performance everywhere else. Disney's content success drives theme park attendance, which drives merchandise sales, which funds new content investment. Amazon's Prime membership works similarly-shipping drives video consumption, which drives cloud adoption.

Asset leverage and infinite scalability: Disney creates Mickey Mouse once but monetizes the character across decades and hundreds of product categories. Look for companies that can leverage core assets across multiple revenue streams without proportional cost increases. Software companies often exhibit this pattern.

Recurring revenue components: while Disney's movies generate one-time box office revenue, theme parks, streaming subscriptions, and licensing deals create recurring cash flows. Predictable earnings provide stability and compound growth opportunities.

The only thing that could stop this money machine

Of course, no empire lasts forever. Disney's biggest threat isn't competition - it's their own success. The same flywheel that makes them unstoppable also makes them vulnerable. A string of box office flops doesn't just hurt the movie division; it fails to create new characters for toys and theme parks. Economic downturns don't just hurt park attendance; they reduce the cash flow needed to create the next billion-dollar franchise. Disney's greatest strength - everything connects to everything - is also their greatest weakness.

The most substantial source of friction is the structural decline of Linear Television. For decades, the cable bundle was a high-margin cash cow that funded the company's expansion. Its erosion is a persistent headwind, putting immense pressure on the other segments to compensate for the lost profitability.

The bottom line: why this matters for your portfolio

Disney's true business model reveals how misleading surface-level company descriptions can be. The company's entertainment empire operates more like a real estate investment trust with theme park properties, combined with a licensing business generating royalties on global consumer products.

Understanding Disney's actual revenue drivers - experiences (37%), entertainment/streaming (45%), and sports (19%) - provides better insight into future prospects than tracking box office performance. Smart investors monitor parks attendance trends, Disney+ subscriber metrics, and licensing revenue growth rather than focusing on whether the latest Marvel movie gets good reviews.

This lesson extends far beyond Disney. Many companies generate revenue through channels that differ significantly from public perception. Amazon's profitability comes from AWS rather than e-commerce, while Apple's services revenue provides higher margins than hardware sales.

Disney's $91 billion revenue machine proves that the most successful entertainment companies don't just sell content - they create intellectual property generating revenue across multiple platforms for decades. That mouse Walt Disney drew in 1928 continues earning billions annually, demonstrating that great brands appreciate rather than depreciate over time.

For investors, Disney provides a masterclass in identifying companies with durable moats, pricing power, and business models designed for long-term wealth creation. The magic isn't in the movies - it's in building a money machine so sophisticated that customers happily pay premium prices while competitors struggle to copy even one piece of the puzzle.

The real Disney magic? Making $91 billion look effortless while everyone thinks you're just in the movie business.

Now that's what I call a happy ending!🦜