Why smart investors are finally going global (and you should too)

For over a decade, one man shaped how millions of people invest. JL Collins - author of The Simple Path to Wealth, patron saint of the FIRE movement, the guy who made "just buy VTSAX" feel like a religious commandment - told his followers that all you needed was one fund. One American fund. Total U.S. stock market. Done.

Then, on February 8, 2026, he published a blog post titled "JL Goes International, and to ETFs... Oh my!" and quietly moved his IRA into VT - a fund that holds the entire world.

The FIRE community lost its mind.

If you've been happily parking your money in a U.S. index fund and calling it a day, this article is about to make you uncomfortable. And that's the point.

The man who changed his mind

Let's be clear about what happened. Collins didn't panic-sell everything and bought gold bars. What he did was shift his tax-advantaged accounts from VTSAX (which tracks only U.S. stocks) to VT (which tracks the entire global stock market). His taxable accounts stayed put - he didn't want to trigger capital gains.

But the why matters more than the what.

In his blog post, Collins cited several concerns that had been building. The U.S. share of global GDP has dropped from roughly 40% in 1960 to about 25% today. The dollar fell approximately 9.4% in 2025 - its worst year since 2017. U.S. national debt is approaching $40 trillion. And erratic tariff policies were damaging America's reputation as a reliable trading partner.

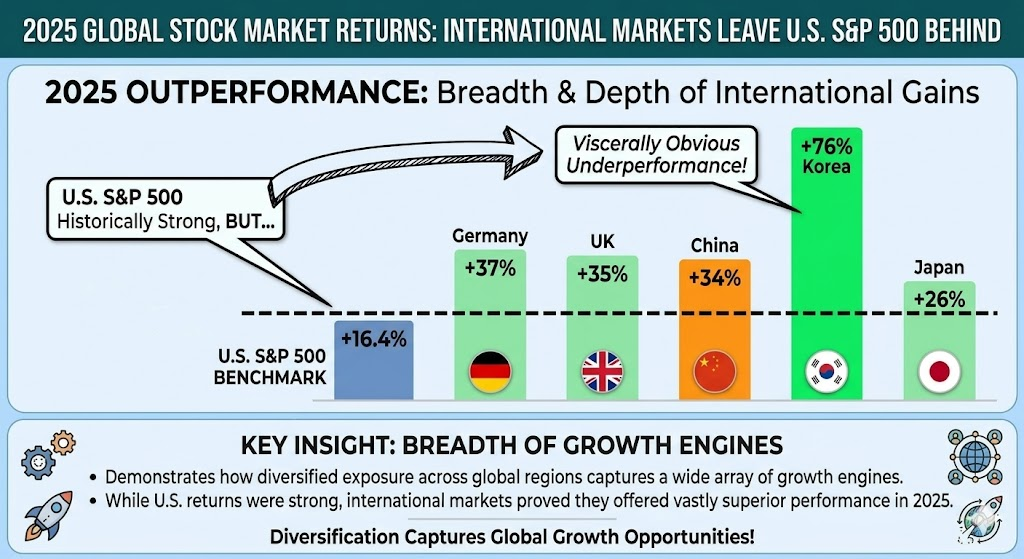

But here's the number that probably tipped the scales: in 2025, the S&P 500 returned 16.4%. Solid, right? Except international stocks returned roughly 31%, according to JP Morgan's analysis of the MSCI All Country World ex-USA index. That's the biggest gap since 1993.

The outperformance wasn't confined to one region. Germany surged 37%. The UK climbed 35%. China rallied 34%. According to JP Morgan, roughly 15 percentage points of the extra international gain came from P/E multiple expansion, and another 7 from the weakening dollar. It was broad-based, multi-continental, and hard to ignore.

Collins stressed he remains "very confident in America." His core philosophy hasn't changed: buy low-cost index funds, stay the course, hold forever. As one New Zealand blogger summarized the shift, "VTSAX and chill hasn't died - it's just gone global." What changed was Collins' answer to which index.

The home bias trap (and why your brain loves it)

Here's a question that should bother you: if the U.S. represents roughly 60% of global stock market capitalization according to MSCI data, why do American investors put 79% of their money in domestic stocks, according to a Vanguard-cited study?

The answer is a cognitive bias called home bias - and it's not just an American problem.

Japanese investors hold roughly 55% of their equity in Japan, despite the country being only about 7% of the world market. Canadians hold 59% domestically versus a 3% global weight. As the economist Gur Huberman documented in his landmark paper "Familiarity Breeds Investment," U.S., Japanese, and U.K. investors hold 93%, 98%, and 82% of their equity in their home countries.

Malmendier, Pouzo, and Vanasco analyzed IMF and World Bank data from 1980 to 2017 and found that U.S. home bias averaged 44% above the optimal level for 38 straight years. It never dropped below 30% - not when the internet arrived, not when global ETFs launched at rock-bottom fees, not when every financial textbook screamed "diversify." They call it experience-based learning: we form beliefs based on what we've personally lived through, and Americans who lived through the 2010s bull market became even more convinced that U.S. stocks were all they needed.

We buy what we know. We trust what we see in the news. We mistake familiarity for safety. And in doing so, we make a very expensive bet that our home country will outperform the rest of the planet - indefinitely.

That bet doesn't always pay off.

When America was a terrible investment

Between December 31, 1999 and December 31, 2009, the S&P 500 delivered an annualized total return of -0.9%. Negative. For an entire decade. The NASDAQ fared even worse, returning roughly -5% per year.

This period - sometimes called the "lost decade" - is the inconvenient truth that every "just buy U.S. stocks" advocate would rather you forget.

Meanwhile, international stocks had a field day. During that same 2000-2009 period, the MSCI World ex-USA returned roughly +2.0% annually - modest, but positive. Emerging markets more than doubled. Even boring European blue chips outpaced the S&P.

The companies and industries that define a market's identity today may be irrelevant tomorrow - which is why betting everything on the current champion is a gamble, not a strategy.

Fun fact: In 1900, railroads represented 63% of U.S. stock market value, according to Dimson, Marsh, and Staunton's 101-year analysis in Triumph of the Optimists. By 2000, railroads had shrunk to 0.2%. Sector dominance is temporary. So is country dominance.

Hartford Funds research shows that U.S. and international stock leadership moves in cycles. International stocks led from the late 1970s through the late 1980s (remember when Japan was supposed to take over the world?). The U.S. dominated from 2010 to 2024. And in 2025, the pendulum swung back.

Nobody knows when the next swing will happen. That's exactly the point.

2025: The year the world woke up

The numbers from 2025 aren't subtle. International stocks didn't just beat U.S. stocks - they demolished them.

South Korea's Kospi index soared almost 76%, its best year since 1999. Japan's Nikkei 225 gained 26%. Alibaba surged 75.8% as China embraced AI. Taiwan's TSMC hit record highs with a 46.5% gain.

And in Europe, where the story was supposed to be sleepy banks and sluggish growth? Markets received a massive boost from defense spending commitments and fiscal stimulus plans. Germany alone pledged to spend 5% of GDP on defense and infrastructure. European equities returned over 20% for the year.

What caused this sudden reversal? Several things converged at once.

First, the U.S. dollar weakened significantly. When the dollar drops, international investments become more valuable when converted back to dollars. A 9.4% currency tailwind is no joke.

Second, the AI boom went global. Chipmakers in South Korea, Taiwan, and Japan captured massive demand.

Third, U.S. trade policy took a sharp turn. According to the World Bank's January 2026 Global Economic Prospects report, U.S. tariff rates hit 17% - their highest level since the 1930s. The IMF's World Economic Outlook put the effective rate even higher at 18.5%, compared to a global average of just 3.5%. This uncertainty pushed capital toward markets with fewer self-inflicted wounds.

And fourth the U.S. market was also far more concentrated: the top 10 companies in the S&P 500 accounted for roughly 40% of its entire market cap, versus just 12% for the top 10 in a global ex-U.S. index. When you "buy the S&P," you're really making a leveraged bet on a handful of tech giants.

The "diversified" lie: what your world fund isn't telling you

Here's where most articles about international diversification stop. They tell you to buy a "total world" ETF and call it a day. Problem solved.

Not so fast.

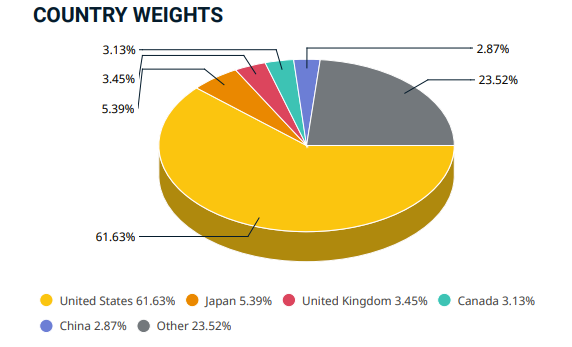

Let's look at what's actually inside VT - the fund JL Collins just switched to. As of March 2026, the MSCI ACWI (the index VT broadly tracks) allocates 61.63% to the United States. Japan gets 5.39%. The UK gets 3.45%. And Germany? Europe's largest economy, the fourth-largest GDP on Earth?

About 2%.

Let that sink in. You buy a "world" fund thinking you're getting global diversification, and six out of every ten dollars still go to one country.

Then there's China. The world's second-largest economy produces roughly 19% of global GDP according to IMF data. Its factories make your phone, your furniture, and half the goods on Amazon. Its consumer market has over a billion people. If you were building a portfolio based on where economic activity actually happens, China would be your second-largest holding.

Its weight in the MSCI ACWI? Just 3.1%.

That means a "world" fund gives China - 19% of the global economy - roughly the same allocation as Switzerland. As Dimensional Fund Advisors pointed out in their April 2025 analysis, if you weighted the MSCI ACWI by GDP instead of market cap, your China allocation would jump from 3.1% to 18.7%. That's a 6x gap between what the index gives you and what the economy says you should own.

Why does this happen? These indices use market-capitalization weighting - the bigger a country's stock market, the bigger its slice of the index. China's stock market is restricted by foreign ownership limits and state-owned enterprises that reduce its freely tradable "float." But from a diversification standpoint, that's an explanation of the mechanics - not a justification for ignoring the second-largest economy on Earth in your portfolio.

And there's another wrinkle most people miss entirely.

When an index says "61.63% United States," it doesn't mean 61.63% of your money is exposed to the American economy. It means 61.63% is allocated to companies listed on U.S. exchanges. That's a crucial difference. A company's country in an index is determined by where it's listed - not where it's headquartered, where it manufactures, or where it earns most of its revenue.

Think about it. Apple is classified as a U.S. stock, but it generates roughly 60% of its revenue outside America. ASML is listed in Amsterdam and counts as "Netherlands" in the index, but it's the sole supplier of cutting-edge chipmaking machines to fabs in Taiwan, South Korea, and the U.S. Unilever sells soap and ice cream in 190 countries but gets categorized based on its London listing.

Fun fact: According to S&P Global, companies in the S&P 500 generate about 40% of their revenue from outside the United States. So that "62% U.S. allocation" in your world fund is already more globally diversified than the label suggests - but the reverse is also true. Your 2% German allocation doesn't capture all the global revenue flowing through German-listed companies like Siemens or SAP.

Now, before you rush to build a GDP-weighted portfolio, here's a crucial nuance. Dimson, Marsh, and Staunton found in their 101-year, 16-country analysis (Triumph of the Optimists) that the correlation between a country's GDP growth and its stock market returns was actually negative (-0.53). Countries that grew their economies fastest - like Japan, Italy, and Spain in the 20th century - didn't translate that growth into shareholder wealth efficiently. Antti Ilmanen confirmed this in Investing Amid Low Expected Returns, finding a correlation of essentially zero between real GDP growth and real equity returns across 43 countries from 1997 to 2017. China is the poster child: its economy grew fivefold between 1993 and 2009, but a dollar-based equity investor earned a negative total return over that period, thanks to massive share dilution.

So GDP weighting isn't a silver bullet either. The point isn't that you should blindly weight by GDP - it's that market-cap weighting has its own distortions, and the "world" fund label gives you a false sense of geographic balance.

Germany's stock market capitalization is only about 44% of its GDP, compared to a world average of 69%, per World Bank data. German companies are real, profitable, globally significant businesses. They're just not all publicly listed or valued at 30x earnings.

So think about this, if you're buying a "world" fund to protect yourself against U.S. decline, but 62% of that fund is allocated to U.S.-listed companies (many of which earn heavily abroad anyway)... how well do you actually understand your diversification?

The honest answer: probably less than you think. VT is better than VTSAX. But it's not true global diversification - and the country labels on the tin can be misleading.

What actual diversification looks like

True diversification means your portfolio's country allocation reflects a deliberate choice - not just the momentum of whichever stock market had the highest recent valuations.

There are a few approaches.

- The GDP-weighted approach. MSCI actually publishes a GDP-weighted version of its world index, and the results are revealing. Since 1988, the GDP-weighted MSCI ACWI has outperformed its market-cap-weighted peer by 2.7% annually, according to MSCI Research. In emerging markets specifically, the GDP-weighted index outperformed by almost 5% per year. This happens because GDP weighting forces you to buy more of the cheap, undervalued markets and less of the expensive, overvalued ones. It's a systematic form of contrarian investing. But remember the GDP-return disconnect we discussed - this outperformance comes from the rebalancing effect (buying cheap, selling dear), not because GDP growth itself predicts stock returns. The catch? GDP-weighted portfolios have higher turnover - about 8.3% annually versus 2.6% for market-cap weighted, per Dimensional Fund Advisors' analysis. GDP data is also lagged and sometimes restated. These aren't dealbreakers, but they're real costs.

- The single-country ETF approach. This is the purist's method. Instead of buying one "world" fund and hoping the weightings make sense, you buy individual country or regional ETFs and set your own allocation. Want 8% in Germany instead of 2%? Buy a DAX ETF. Think China deserves more than 3%? Add a dedicated China ETF. Believe emerging markets are undervalued? Overweight them explicitly. This gives you complete control over geographic exposure. The downside is complexity. You're now managing 5-10 positions instead of one, and you need to rebalance periodically. But you're also making conscious decisions about geographic exposure instead of blindly following market-cap momentum.

- The hybrid approach. Most practical for beginners: use a total world fund (VT or VWCE for European investors) as your core holding - maybe 60-70% of equities - and then add single-country or regional ETFs to correct the weightings you disagree with. Think of the world fund as your baseline, and the satellite positions as your adjustments for reality.

The free lunch (that actually exists)

Harry Markowitz, who won the Nobel Prize in Economics for his work on portfolio theory, proved mathematically that combining assets that don't move in perfect lockstep reduces your total risk without necessarily reducing your returns. He called diversification "the nearest an investor or business manager can ever come to a free lunch."

And we're not talking about small effects. Dimson, Marsh, and Staunton examined 101 years of data across 16 countries (covering roughly 88% of the world's stock market capitalization) and found that moving from a single-country portfolio to an equally weighted 16-country portfolio reduced annual volatility from 29.1% to 17.3%. That's a 40% reduction in risk - not over a few years, but over an entire century.

Fun fact: Antti Ilmanen demonstrated the power of diversification with an extreme example. A 50/50 portfolio of heating oil futures and stocks, rebalanced regularly, earned an 11.0% geometric return - higher than either asset alone (8.2% and 6.8%). He called the 3.5% bonus a "diversification return" and wrote that diversification was like "turning water into wine." The same principle applies to country diversification - the portfolio is genuinely more than the sum of its parts.

Peter Bernstein demonstrated this with real numbers in Against the Gods. From 1970 to 1993, the S&P 500 returned 11.7% per year with a standard deviation of 15.6%. The EAFE international index returned 14.3% with a standard deviation of 17.5%. But a portfolio split 75% U.S. and 25% international lowered the standard deviation to 14.3% while increasing returns. You got more return and less risk. That's not a sales pitch - it's math.

A more recent analysis from Vanguard confirms the pattern holds. A 60% U.S. / 40% international equity portfolio delivered roughly 10% annualized over the past decade - between the 13% of a pure U.S. portfolio and the 5% of a pure international one - but, crucially, with considerably less variability in outcomes. Vanguard calls this an "insurance policy" against severe underperformance in any single region.

As Ilmanen wrote in Investing Amid Low Expected Returns: "Diversification remains the one almost-free lunch in investing, though its costs include unconventionality and lesser intuition." In other words, proper diversification feels weird. Your friends at dinner parties will have stronger opinions about single stocks or U.S. tech. Your portfolio will look boring. But boring wins.

How to actually do this

Let's get practical. Here's what you need to know about implementation.

If you want the simple approach, VT (Vanguard Total World Stock ETF) gives you roughly 10,000 stocks across developed and emerging markets for an expense ratio of just 0.06%. For European investors, VWCE (Vanguard FTSE All-World UCITS ETF) offers the same concept in a European-domiciled wrapper.

These aren't perfect. As we discussed, they're still 60%+ U.S. But they're a massive improvement over 100% domestic, and they automatically rebalance as global dynamics shift. If the U.S. share of global markets shrinks over time, VT adjusts without you lifting a finger.

If you want true geographic diversification, consider building a small portfolio of regional ETFs. A reasonable starting framework:

- U.S. total market (40-50%)

- Europe ex-UK (15-20%)

- Asia-Pacific developed (10-15%)

- Emerging markets (10-15%)

- UK (3-5%)

These percentages roughly correspond to GDP weights rather than pure market-cap weights, giving you more exposure to underrepresented economies.

A note on currency: when you invest internationally, you're automatically taking on currency exposure. If the euro strengthens against the dollar, your U.S. holdings lose value in euro terms (and vice versa). Whether to hedge this risk is a complex question that depends on your home currency, time horizon, and cost tolerance. For most long-term investors, the general consensus is that currency fluctuations wash out over decades - but it's worth understanding the exposure you're taking.

Tax considerations vary enormously by country. Dividend withholding taxes, capital gains treatment, and tax treaty benefits differ depending on where you live and where the fund is domiciled. This is one area where "check your local regulations" isn't lazy advice - it's genuinely the only responsible thing to say.

Practical takeaways

- Start by knowing your exposure. Check your current portfolio. If more than 60% sits in one country's stocks, you're making a concentrated bet whether you realize it or not. Understanding your portfolio's risk profile is key - tools like a portfolio beta calculator can help you see how exposed you really are.

- A world fund is a good start, not the finish line. VT or VWCE gets you from 100% domestic to 60% domestic instantly. That's progress. But recognize it's still U.S.-heavy.

- Consider GDP weights, not just market-cap weights. If China is 19% of global GDP but 3% of your "world" fund, that's a decision someone else made for you. Decide if you agree with it - but also remember that GDP growth and stock returns don't correlate the way you'd expect.

- Add satellite positions for genuine diversification. Single-country or regional ETFs let you correct for market-cap distortions. Even 2-3 positions can meaningfully change your geographic exposure. The principle of rebalancing applies here too - periodically adjusting back to target weights forces you to buy low and sell high.

- Don't swap everything overnight. Collins only changed his tax-advantaged accounts. If switching would trigger capital gains, consider redirecting new contributions instead.

- Accept that true diversification feels uncomfortable. Some of your holdings will underperform. That's the design, not a flaw. The portfolio as a whole is what matters.

As Ilmanen put it: "I prefer humble forecasts and bold diversification."

JL Collins spent a career saying one fund was enough. When the world gave him reasons to reconsider, he reconsidered. That's not weakness. That's what thinking clearly about money actually looks like.

Happy investing!