Why Spotify pays 70% revenue to record labels: the streaming music economics trap explained

Discover why Spotify surrenders approximately 69% of revenue to record labels, how streaming music economics work, and what it means for subscription prices and your investment portfolio.

Picture this: You're running the world's most popular music streaming service with 696 million users. You're generating over €16 billion in revenue. Sounds like a goldmine, right?

Plot twist: You have to hand over roughly seven out of every ten dollars you make to a handful of record labels who basically own all the music people actually want to hear.

And if you have no idea who Spotify is, Netflix made a series on them.

Welcome to Spotify's reality - a modern business nightmare that took 16 years to escape. After finally achieving consistent annual profitability in 2024, Spotify continues to face the industry's toughest economics. As of Q2 2025, cost of revenue still represents approximately 68.5% of total revenue, with the vast majority paid to record labels and publishers. That's like opening a restaurant where you have to give 68 cents of every dollar to your food suppliers. Good luck staying in business.

This streaming music business model doesn't just affect Spotify - it's reshaping how every content business operates, from Netflix to gaming companies. And yes, it's directly connected to why your streaming subscriptions keep getting more expensive.

Let's break down how the music industry created the most sophisticated wealth extraction machine in modern business, and what it means for your investment portfolio and monthly budget.

How Record labels control Spotify

Remember when you thought Spotify was just a tech company with a music app? Think again.

Spotify is basically running a protection racket, except they're the ones getting shaken down. The muscle belongs to three record label giants who control virtually everything you actually want to listen to.

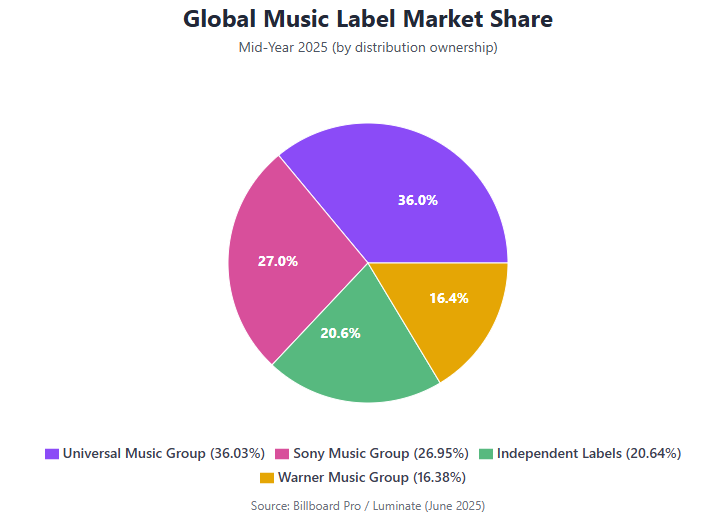

The Big three music labels: Universal, Sony, and Warner's market dominance

Three companies control 70% of all commercially relevant music.

- Universal Music Group: 36% of global market share

- Sony Music: 27% market share (secured 5.8% equity in Spotify during negotiations)

- Warner Music Group: 16% market share

Fun fact: When the major labels cashed out their Spotify equity after the company's IPO, they collectively made over $1 billion from those early ownership stakes - money that didn't have to be shared with artists under most record contracts. Sony alone sold part of its stake for $750 million in 2018.

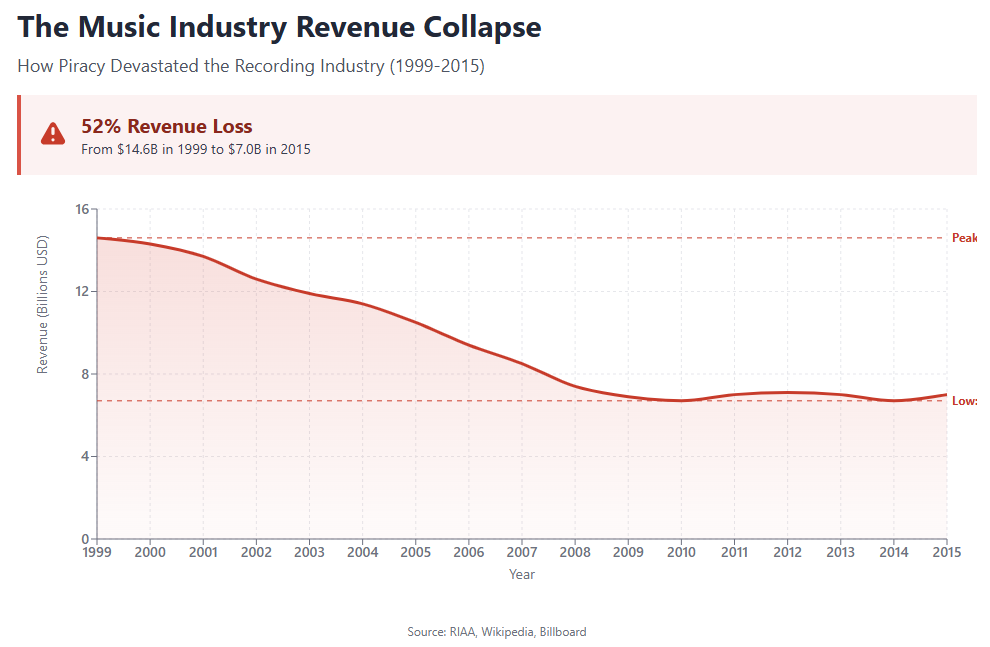

The Napster hangover: why Labels were paranoid

Between 1999 and 2015, the music industry's revenues collapsed by over half due to piracy. This wasn't just a business setback - it was an existential crisis that made labels deeply suspicious of any digital model that offered music without immediate payment.

When Spotify showed up with "free" music funded by ads, labels saw Napster 2.0. Warner Music's CEO Edgar Bronfman Jr. was so opposed to the freemium model that he threatened to pull Warner's entire catalog if Spotify didn't severely limit free access.

The ultimate power move: own your customer

When Spotify was a scrappy startup desperately needing music catalogs, the major labels didn't just demand money - they demanded ownership:

- Universal: Grabbed equity stakes plus "schmuck insurance" - a secret clause requiring Spotify's founders to pay Universal tens of millions if they sold the company or went public too quickly

- Sony: Negotiated 5.8% of the company

- Warner: Also secured equity stakes worth hundreds of millions

Imagine if your suppliers not only charged you most of your revenue but also owned part of your company and had a clause preventing you from selling without paying them extra. That's not a business relationship - that's a hostage situation with profit sharing.

Think the revenue split is bad enough? Plot twist: Spotify pays $1.6 million per day in minimum guarantees to just the Big Three labels. That's $144 million quarterly in non-refundable upfront payments, whether people stream their music or not.

Spotify only achieved its first quarterly operating profit in late 2018 - a full decade after launching in 2008. It then took until 2024 to achieve consistent annual profitability. That's 16 years of losses before finally escaping the red, longer than it took Amazon to become profitable. As of Q2 2025, the company posted an operating income of €406 million with a 9.7% operating margin and generated a record €700 million in quarterly free cash flow.

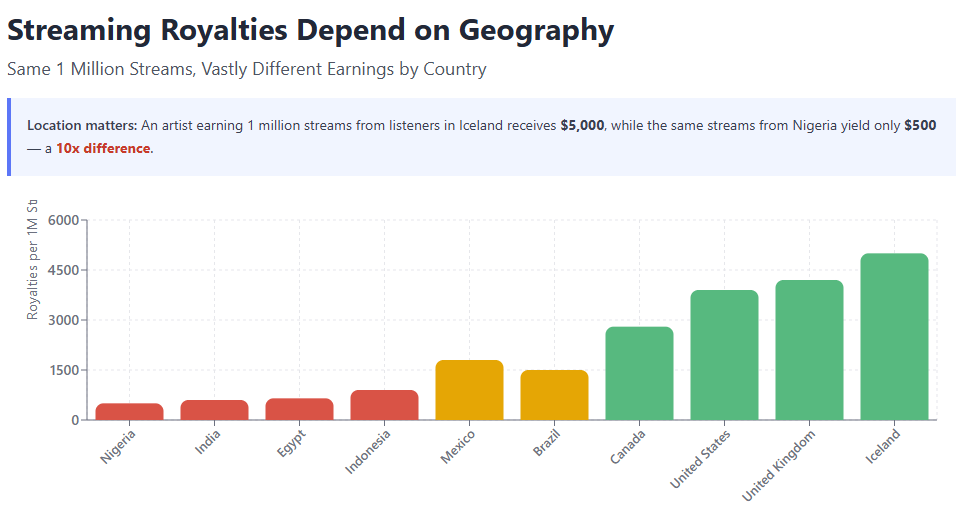

Geographic chaos: why location determines your paycheck

If you thought this was complicated already, wait until you hear about geographic licensing. Every country requires separate deals, with wildly different payout rates:

- Mexican artists: Earn 3x more from US streams than domestic ones

- Colombian artists: Make 6x more from American listeners

- The same song: Generates completely different revenues based on where the listener lives

This creates a bizarre global economy where streaming royalties' value depends entirely on geographic location. It's like if the same hamburger cost different amounts depending on where the customer lived, not where the restaurant was.

Spotify revenue breakdown: the math that breaks dreams

Quick business quiz: If you're running a tech company and you double your user base, what happens to your profits?

Normal answer: They should skyrocket because you're spreading fixed costs over more customers.

Spotify's answer: "Actually, our costs doubled too. Thanks for asking."

Understanding Spotify's cost of revenue structure

Here's the breakdown of where every dollar goes in Spotify's business model as of Q2 2025 (Source Spotify's Q2 2025 earnings):

- €4,193 million: Total Q2 2025 revenue

- €2,873 million: Paid to record labels and publishers (68.5%)

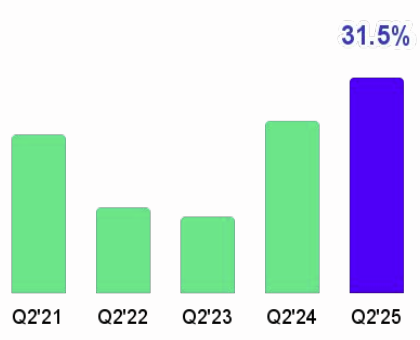

- €1,320 million: Gross profit (31.5% gross margin)

That gross profit has to cover:

- Research & development: €415 million in Q2 2025

- Sales & marketing: €364 million in Q2 2025

- General & administrative: €135 million in Q2 2025

- All other costs: Salaries, offices, servers, coffee for stressed executives

The improving trend: While Spotify historically paid out 74% of revenue to rights holders, the company has improved gross margins to 31.5% as of Q2 2025 (up from 29.2% a year earlier) through price increases, the audiobook bundling strategy, and improved podcast economics. Still, after paying the labels their cut, Spotify's margins remain razor-thin compared to traditional tech companies.

Why streaming scale economics don't work for Spotify

If we simplify a bit, for a traditional tech company that ties a lot of money in IT infrastructure costs:

- Add 1 million users = slightly higher server costs

- Revenue per user stays the same

- Profit margins expand

Spotify's reality:

- Add 1 million users = 1 million × more music streamed

- Music costs are percentage of revenue, not fixed

- Gross margins improving but still constrained (31.5% as of Q2 2025)

Spotify vs Apple Music vs Amazon Music: competition economics

What makes it all of this worse for Spotify, isn't competing against other music companies - it's fighting tech giants who use music as a loss leader:

Apple Music: Tim Cook literally said "We're not in it for the money" - they use it to sell more iPhones

Amazon Music: Bundled with Prime to drive retail sales and smart speaker adoption

YouTube Music: Backed by Google's advertising empire, where music is just another way to collect data

Spotify: Actually needs to make money from music streaming

YouTube won the streaming war by building a user-generated content model where creators upload billions of videos for free, making it the most-used music platform globally. Meanwhile, Spotify has to pay for every single song. It's like competing in a race where your opponent gets a free car while you have to rent yours at 69% of your revenue.

Why artists earn pennies per stream: the artist payment problem

Ready for some depressing math? Let's follow the journey of your $11.99 Spotify subscription to see how much actually reaches the artists you love.

Spoiler alert: It's not pretty.

The "All-In" contract structure

When an artist signs a traditional record deal, they get an "all-in" royalty rate - usually 15-20% for new or mid-level artists. Sounds reasonable until you learn what "all-in" actually means:

The Producer's cut:

- Producers typically grab 3-4% from the artist's royalty

- An artist with an 18% "all-in" rate who hires a 3% producer ends up with a net rate of 15%

- This comes out of the artist's share, not the label's

The Recoupment trap:

- Both the artist's advance and all recording costs are treated as debts

- The artist must pay back 100% of these costs from their tiny royalty percentage

- Recording an album easily costs hundreds of thousands of dollars

- Many artists remain "unrecouped" for years, seeing $0 in royalty income

The label becomes profitable the moment streams cover their revenue share percentage, but the artist doesn't earn a dime until 100% of costs are recouped from their much smaller slice.

Spotify pay per stream: following the money trail

When you stream a song, here's the money trail:

- Step 1: Spotify keeps ~31.5% for operations (based on Q2 2025 gross margin)

- Step 2: ~68.5% goes into the "royalty pool"

- Step 3: Record labels grab the majority of Spotify's total payout

- Step 4: Publishers get their cut for songwriting rights

- Step 5: Producer takes their 3-4% cut from artist's share

- Step 6: Labels deduct expenses, advances, marketing costs

- Step 7: What's left goes to artists (if they're recouped)

The brutal reality: Artists earn $0.003-$0.005 per stream on Spotify. To make minimum wage, you need 330,000 streams per month.

Fun fact: Only 203,000 of Spotify's 11+ million artists earned over $1,000 annually from streaming in 2023. That's less than 2% making what most people earn in a week. The other 98% earned under $1,000 for the entire year - despite Spotify paying over $5 billion in total royalties.

Platform payout comparison: the hierarchy of sadness

Another way to look at it, is to see how much artists earn for 1,000 streams. It’s worth noting that streaming payouts aren’t fixed “per-stream” rates though. Platforms pool revenue and distribute it based on each artist’s share of total plays - adjusted by factors like region, subscription type, and ad revenue. Add label cuts, fluctuating rates, and payment thresholds, and those neat figures become rough averages rather than guarantees. Anyway, here are the estimates:

| Platform | Payout per 1,000 streams |

|---|---|

| Amazon Music | $4.00 |

| Apple Music | $6.20 |

| Spotify | $3.00-$5.00 |

| YouTube Music | $1.00-$2.00 |

Spotify's Podcast strategy: billion-dollar escape from music licensing

Imagine you're trapped in a business where roughly 69% of your revenue disappears into someone else's pocket. What's your escape plan?

Spotify's answer: Stop being just a music company.

How Spotify invested in podcasts to reduce label dependency

Starting in 2019, Spotify went on a shopping spree to kickstart their podcast portfolio:

- Gimlet Media & Anchor: $340 million combined in 2019 for podcast production and hosting tools

- The Ringer: Sports and pop culture network founded by Bill Simmons

- Joe Rogan: $250 million renewal deal (originally $100 million)

- Alex Cooper's "Call Her Daddy": $60+ million before jumping to SiriusXM for $125 million

Total investment since 2020: Over $1 billion across the entire podcasting value chain

The brilliant strategy: Unlike music, podcasts can be owned outright or licensed exclusively for fixed costs. No more percentage-based royalty prison.

The CEO's vision: Daniel Ek stated the goal was for "audio - not just music" to be Spotify's future, with over 20% of all listening being non-music content. Why? Because owned content = better margins.

The bundle hack: legal loophole worth $200 million

In 2024, Spotify pulled off one of the smartest financial maneuvers in streaming history. They added 15 hours of audiobooks to Premium subscriptions, creating a "bundle." While part of the reason might have been to grab the audiobook consumers, there is another one you probably are not aware of: pay less royalties.

The regulations have a different formula for bundled services - services that offer music PLUS other non-music content (like video, audiobooks, games, etc.). For bundles, the mechanical royalty is calculated using this formula:

Total subscription revenue × (Percentage of service usage attributed to music) × statutory rate

If Spotify can prove that subscribers spend time on non-music content, they can allocate a portion of subscription revenue away from music royalties.

Now let's play some math.

- Total revenue at ~$18.5 billion USD

- Royalties at ~10.5% of revenue --> ~$1.94B USD

But! If bundling reduces this by allocating even just a very small part, ~15% of value to audiobooks:

- Savings: $1.94B × 0.15 = $194 million annually

The expansion: In Q2 2025, Spotify rolled out audiobooks in Premium to Germany, Austria, Switzerland, and Liechtenstein, giving users access to over 350,000 titles. Audiobook listening hours grew over 35% year-over-year in the U.S., U.K., and Australia. The company also launched Audiobooks+, a monthly add-on subscription enabling access to incremental listening hours.

Fun fact: The music publishers sued Spotify over this move, claiming it was an "unlawful loophole." A federal court ruled in Spotify's favor in early 2025.

Geographic nightmare: 184 different ways to lose money

Think negotiating with three major labels is hard? Try doing it in 184 different countries with completely different laws, currencies, and economic conditions.

The global pricing chaos

Remember how we said location affects royalties? Here's the subscription price insanity:

Monthly subscription costs:

- India: $0.84

- United States: $11.99

- Price difference: Over 1,000%

Spotify operates in 184 different markets, each requiring separate licensing negotiations, different royalty structures, and compliance with local laws. But here's the kicker - subscription pricing varies by over 1,000% globally while licensing costs don't drop proportionally. A stream from India generates roughly 1/3 the revenue of a US stream, yet Spotify still pays similar percentages to labels in both markets.

Market entry: a political minefield

Spotify can't just launch wherever it wants. It needs permission from local copyright societies and governments:

Launch failures and delays:

- Germany & Italy: Initial European launch delayed due to local copyright society negotiations

- Russia: Planned launch cancelled due to repressive internet legislation

- China: Completely barred from launching, forced to partner with Tencent Music instead

- US Market: Blocked for years by major labels (especially Warner's CEO Edgar Bronfman Jr.) until Spotify made massive concessions

Currency chaos and legal complexity

Beyond pricing, Spotify deals with:

- Currency fluctuations affecting royalty payments across dozens of currencies (Q2 2025 saw €104 million in unfavorable FX headwinds)

- Different copyright frameworks in each country requiring local legal expertise

- Regional collection societies each taking their percentage

- Local content requirements in some countries (Canada and France historically required radio to play minimum domestic content)

- Regulatory scrutiny like Apple's €1.84 billion EU fine for anticompetitive practices

Every country requires separate negotiations, different royalty structures, and compliance with local laws. Scale doesn't create efficiency - it multiplies complexity exponentially.

Streaming subscription price increases: why your music costs more

Remember when Netflix cost $7.99? Or when Spotify stayed at $9.99 for over a decade? Those days are dead, and Spotify's economics explain why.

Understanding recent Spotify price increases

Spotify's recent price increases from $10.99 to $11.99 in 2024 represent just the beginning. Here's why:

The Math Problem:

- Fixed subscription price for years: $9.99

- Rising content costs: Everything increases except Spotify's revenue per user

- Inflation: Office rent, employee salaries, server costs all go up

- Royalty rates: Labels push for higher percentages

The current reality: As of Q2 2025, Premium ARPU (average revenue per user) is €4.57, declining 1% year-over-year in reported terms but up 3% excluding foreign exchange impacts. This reflects the ongoing pressure to raise prices to maintain profitability.

The streaming price prediction: With operating margins still under 10% despite reaching profitability, further price increases are inevitable as Spotify chases sustainable margins.

Investment alert: the content business danger zone

If you have to remember one rule, that would be: never invest in companies that rent their key inputs from oligopolies.

Spotify's core problem isn't unique - it's a case study in what happens when you build a business around assets you don't control. Here are the warning signs to watch for:

Red Flags:

- High percentage of revenue paid to suppliers (Spotify: ~69% as of Q2 2025)

- Concentrated supplier base (3-5 companies control most content)

- Suppliers who also compete or own competing platforms

- Variable costs that scale with revenue instead of fixed costs

Green Flags:

- Own their content or key inputs

- User-generated content models

- Diversified supplier base with no single dominant player

- Improving gross margins over time (Spotify has improved from 29.2% to 31.5% Y/Y)

Real-World Comparisons: The Good, Bad, and Ugly

The Bad (Improving): Spotify's music licensing model

- Suppliers: 3 major labels control 70% of content

- Cost structure: ~69% of revenue to suppliers (Q2 2025), down from historical 74%

- Profitability timeline: 16 years to reach consistent annual profitability

- Current status: €406 million operating income, 9.7% operating margin, €700 million quarterly free cash flow

The Ugly: Traditional cable TV companies

- Suppliers: Networks demand higher fees every year

- Cost structure: Sports rights alone can cost billions

- Result: Cord-cutting acceleration and industry decline

The Good: YouTube's user-generated content

- Suppliers: Millions of creators, no single dominant player

- Cost structure: Revenue sharing, but YouTube sets terms

- Result: Massive profitability and market dominance

The Smart: Netflix's original content strategy

- Evolution: From licensing to owning content

- Investment: Billions in original programming

- Result: Reduced supplier dependence and improved margins

The pattern: Content ownership beats content licensing every time.

What could break the music Mafia

The streaming music trap isn't permanent, but breaking it requires seismic industry shifts. Here's what could actually reshape the game - and why each potential revolution faces its own uphill battle.

AI Music could change everything (or nothing)

Spotify could generate unlimited background music, lo-fi beats, and ambient soundscapes without paying a single dollar in royalties. That's the promise of AI-generated music - and it's closer than you think.

AI music is expected to account for 20% of streaming revenues by 2028. That's over $3 billion annually that could potentially flow to platforms instead of labels. But there's a catch. Recent US court rulings determined that AI-generated works can't receive copyright protection. No copyright means anyone can copy it freely, which makes it worthless for building a defensible music catalog.

The major labels aren't panicking. They're doing what they do best - turning a potential threat into a new revenue stream. Universal, Sony, and Warner are already in licensing talks with AI music generators Suno and Udio - the very companies that were supposed to disrupt them.

The likely outcome? Instead of AI freeing platforms from label control, we'll probably see "AI-generated Taylor Swift sound-alikes" that require licensing from... you guessed it, the same three labels that own the training data. The revolution becomes just another revenue stream for the incumbents.

Direct-to-fan revolution

While the big players fight over AI, something more interesting is happening at the grassroots level. Thousands of artists are simply walking away from the streaming game entirely.

Bandcamp's revolutionary model: Artists keep 82% of every sale. One fan buying a $10 album puts $8.20 directly in the artist's pocket. To earn that same $8.20 on Spotify, you'd need roughly 2,000-2,700 streams. It's not even close.

The Patreon phenomenon: Over 300,000 creators are now generating $8+ billion annually through direct fan subscriptions. Musicians with just 500 dedicated fans paying $5/month earn $30,000 annually - far more than all but the top 2% of Spotify artists.

The "1,000 True Fans" theory in action: Author Kevin Kelly predicted this decades ago - you don't need millions of casual listeners. You need a smaller group of dedicated fans who'll pay directly for your work. NFT and Web3 platforms are taking this further, letting artists earn royalties every time their music resells, creating perpetual income streams that traditional streaming can never match.

The emerging two-tier system: Smart artists now use streaming services like Spotify as discovery tools and loss leaders, not income sources. They give away music on streaming to build audiences, then monetize through concerts, merchandise, Patreon subscriptions, and direct digital sales. One $10 album sold directly equals the revenue from thousands of streams - so why not cut out the middleman entirely?

The limitation? This model works brilliantly for niche artists with dedicated fanbases. It doesn't scale to mainstream pop music that depends on casual listeners and algorithmic discovery. Taylor Swift can't run a Patreon. But for the 98% of artists earning under $1,000 annually on Spotify? Direct-to-fan platforms offer a genuine alternative path to sustainability.

Regulatory pressure: when Governments notice the math doesn't add up

Politicians are starting to do the same math we've been doing throughout this article - and they're not liking what they see. When 98% of artists on the world's largest music platform earn less than $1,000 annually while three corporations collect $12+ billion, that's the kind of wealth concentration that gets regulatory attention.

France fired the first shot: In 2022, France enacted legislation guaranteeing minimum streaming royalty rates, directly mandating higher payments to artists regardless of what labels and platforms negotiate. It's small, but it's precedent-setting.

The US is watching closely: The proposed "Living Wage for Musicians Act" would create new royalty funds paid through taxes on streaming platforms and subscriber fees - money that would bypass labels entirely and go directly to artists based on streams. If it passes, it fundamentally rewrites the value chain.

Why this might actually work: Unlike technological disruption (which labels can co-opt) or grassroots movements (which they can ignore), regulatory change forces compliance. When the EU fined Apple €1.84 billion for anticompetitive practices, it didn't ask politely - it took the money. Similar pressure applied to streaming royalty structures could mandate fairer splits regardless of what existing contracts say.

The real question: will any of this actually matter?

The major labels survived the transition from vinyl to CDs to digital downloads to streaming. They'll likely survive AI, direct-to-fan platforms, and regulatory pressure too.

AI might generate infinite music, but it can't (yet) create the next Beatles or Beyoncé. Direct-to-fan platforms work great for niche artists but can't replicate the mainstream cultural phenomenon of a globally coordinated album release. Regulation might mandate higher payments, but labels will find new ways to structure deals and extract value.

The most likely future? Not revolution, but evolution:

- Streaming prices keep rising to support higher royalty payments

- AI-generated content fills out "background music" categories while humans dominate premium content

- A robust independent artist economy thrives alongside the mainstream streaming system

- Labels maintain dominance but gradually see their margins compress from multiple directions

- Artists with dedicated fanbases increasingly opt out of traditional deals entirely

What this means for your money

Spotify's story is ultimately about power, concentration, and the challenge of building sustainable businesses in winner-take-all markets.

For your investment Portfolio

The Spotify lesson: Even brilliant execution and massive scale can't overcome structural disadvantages - but they can eventually create profitability. When evaluating content businesses:

- Look for content ownership, not just content access

- Avoid businesses dependent on oligopolistic suppliers

- Favor platforms with user-generated content models

- Watch for regulatory risks in concentrated industries

- Monitor margin trends - improving gross margins signal the business model is working

Share buyback signal: The July 2025 decision to upsize share repurchases to $2 billion indicates management's confidence that the worst is behind them and the business model is finally sustainable.

That's all folks! Happy investing! 🦜