An introduction to bonds: what you need to know before investing

Are you looking to expand your investment portfolio? Have you ever considered investing in bonds? Bonds are one of the most common investments and can provide a steady stream of income over time. If you're new to bonds or just want to brush up on some of the basics, then this blog post is perfect for you! We'll explain how bonds work and why they are so popular among investors, as well as provide guidance on what kinds of questions to ask before investing in them. Read on for an introduction to bonds that will help get your feet wet in the world of investing.

What are bonds and how do they work

Bonds, or fixed-interest securities, are essentially loans given to institutions or governments by investors. When you buy a bond, you're lending money in exchange for interest payments (called coupons) over time. The amount of interest that you'll receive is determined when the bond is initially issued and will remain fixed until the bond matures (the date at which the institution or government must return your investment). Most bonds also come with a set date when the principal loan must be repaid, ensuring that your money is secure.

Bonds offer a higher income than a deposit account, with the possibility of some capital growth. They offer lower risk than shares, but they generally offer a lower return.

Why do companies borrow in the corporate bond market? Two reasons. First, since taxes are calculated on the profit AFTER interests (of a debt) are paid, the company ends up with lower tax bill. Second, companies can borrow money for longer term from the bond market than from banks, which are not typically keen on such arrangements.

Types of Bonds

As you look into investing in bonds, it's important to understand the different types of bonds available. The simplest distinction can be made on the issuer of the bond:

- Government bonds: issued by national governments or local entities. If we exclude some particular cases, the chance of a country to default is much lower than a business, hence this is the safest form of bond. As you probably guess by now, the price for safety is lower return. When discussing the economic outlook of a country, one of the key indicator is the yield of the Government bonds with a 10-year maturity, which are often referred as risk-free bonds as they (tend to) repay interest and principal with absolute certainty.

- Corporate bonds: issued by businesses when they need to raise money. Corporate bonds tend to offer higher returns than government bonds, but they also involve more risk as businesses are more likely to default on their loan payments.

Another way to classify bonds is their structure:

- Bullet: these are bonds where the investor will only receive one payment at maturity.

- Zero-coupon: these bonds do not make regular coupon payments but instead provide a lump sum upon maturity. The gain is the difference between the purchase price and the lump sum received (upon maturity).

- Floating rate: these bonds have variable interest rates that change with market conditions. E.g. inflation.

- Municipal: these bonds are issued by local governments and offer tax-free income.

- Perpetual: these bonds have no set maturity date and continue to pay interest indefinitely.

- Redeemable: these bonds have a set maturity and interest rate, with the option to be redeemed before their maturity date.

- Callable: these bonds can be redeemed by the issuer before their set maturity date.

- Putable: these bonds can be sold back to the issuer prior to their maturity date.

- Sinkable: these bonds are backed by a fund set aside by the issuer. The issuer over time buys and retiring a portion of the bonds periodically on the open market, drawing upon the fund to pay for the transactions.

- Convertible: these bonds can be converted into shares at a predetermined ratio.

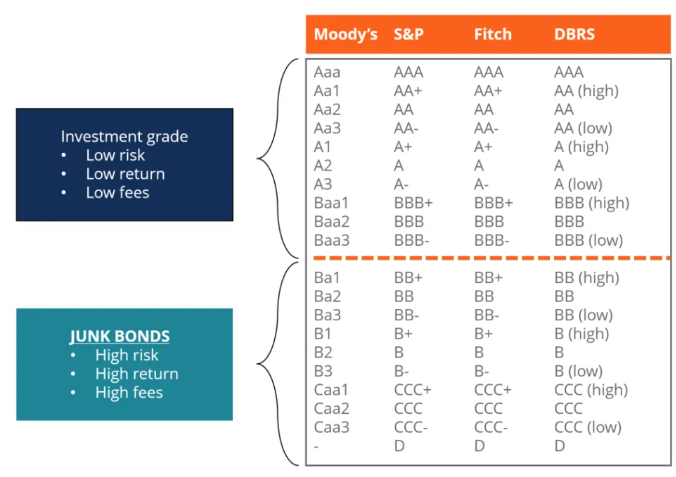

Bond ratings and what they mean

Every bond is assigned a rating by an independent agency such as Standard & Poor’s or Moody’s that reflects its creditworthiness and potential for defaulting on loan payments. Ratings range from AAA (the highest quality), pronounced "triple-A" to D (the lowest quality) which indicates the firm is in default. Ratings of BBB– (S&P and Fitch) or Baa3 (Moody’s) or above are regarded as ‘investment-grade debt’ – this is important because many institutional investors are permitted to invest in investment-grade bonds only. Bonds rated below this are called high-yield (or junk) bonds. Note that the specific loan is rated, rather than the borrower. If the loan does not have a rating it could be that the borrower has not paid for one, rather than implying anything sinister.

Advantages and Disadvantages of Investing in Bonds

Investing in bonds can be a great way to diversify your portfolio and create a steady stream of income, but it's important to understand the advantages and disadvantages before committing any funds. On the plus side, bonds tend to be less volatile than stocks and provide more consistent returns. Additionally, they offer tax benefits depending on what type of bond you're investing in. Bond holders are entitled to annual interest before shareholders receive dividends, making them far less vulnerable if the company underperforms - plus they have legal rights that ensure their investment won't go up in smoke!

It's not all roses though. Bonds do not offer potential for high returns, their prices and returns are normally impacted negatively by inflation, and there is no voting power over the management of the company (that normally comes with shares).

How to buy bonds

Once you have a good understanding of the basics of bonds and you’ve decided that they are right for your portfolio, it’s time to start investing. The first step is to identify an investment broker or bank who can help you purchase the bonds you want. You can also use online platforms such as ETFs (Exchange Traded Funds) or mutual funds that allow you to buy a basket of bonds without having to purchase them individually. Whichever approach you choose, make sure to do your research and understand the fees associated with each option before investing.

Tax Implications of Investing in Bonds

Depending on what type of bond you're investing in, you may be subject to different taxes such as capital gains, regular income, and alternative minimum taxes. Additionally, some bonds offer tax advantages for certain investors, so make sure to research the details before installing any funds.

Conclusion

Investing in bonds is a great way to diversify your portfolio, earn a steady income, and gain access to tax benefits. However, it’s important to understand the advantages and disadvantages of investing in bonds before committing any funds. Additionally, you should be aware of the various types of bonds available as well as their associated risks so that you can make an informed decision about what type of bond best suits your investment goals. Understanding how taxes apply to different types of investments will also help ensure that you get the most out of your investment while minimizing potential liabilities.

Happy investing!