Kakeibo, the art of saving

The 家計簿 (kakeibo) - literally household finance ledger - is the essential tool used by any money-savvy Japanese to manage the household finances. She would diligently keep up her kakeibo every day, noting down items in each budget category.

Kakeibo promises an automatic saving of 35% on the household finances and learn how to use it is pretty simple: record every expense and follow the instructions. Simple, right?

Although it might take some time to get used to record every expense, the idea is that after some time you will be more aware of your financial habits and learn insights on how you spend money: maybe you’re spending too much on restaurants or maybe you should spend more on culture. The book’s subtitle slogan is ‘memory can be fuzzy, but the books are accurate’.

How to use a Kakeibo

- A the beginning of the month write down your fixed expenses and incomes (e.g. mortgage, rent, broadband bill, etc.). The difference will show you how much money you have available for the rest of the month.

- Estimate the savings that you want to achieve for the month and set it aside. You should just forget it and make everything possible to don’t touch it during your weekly expenses.

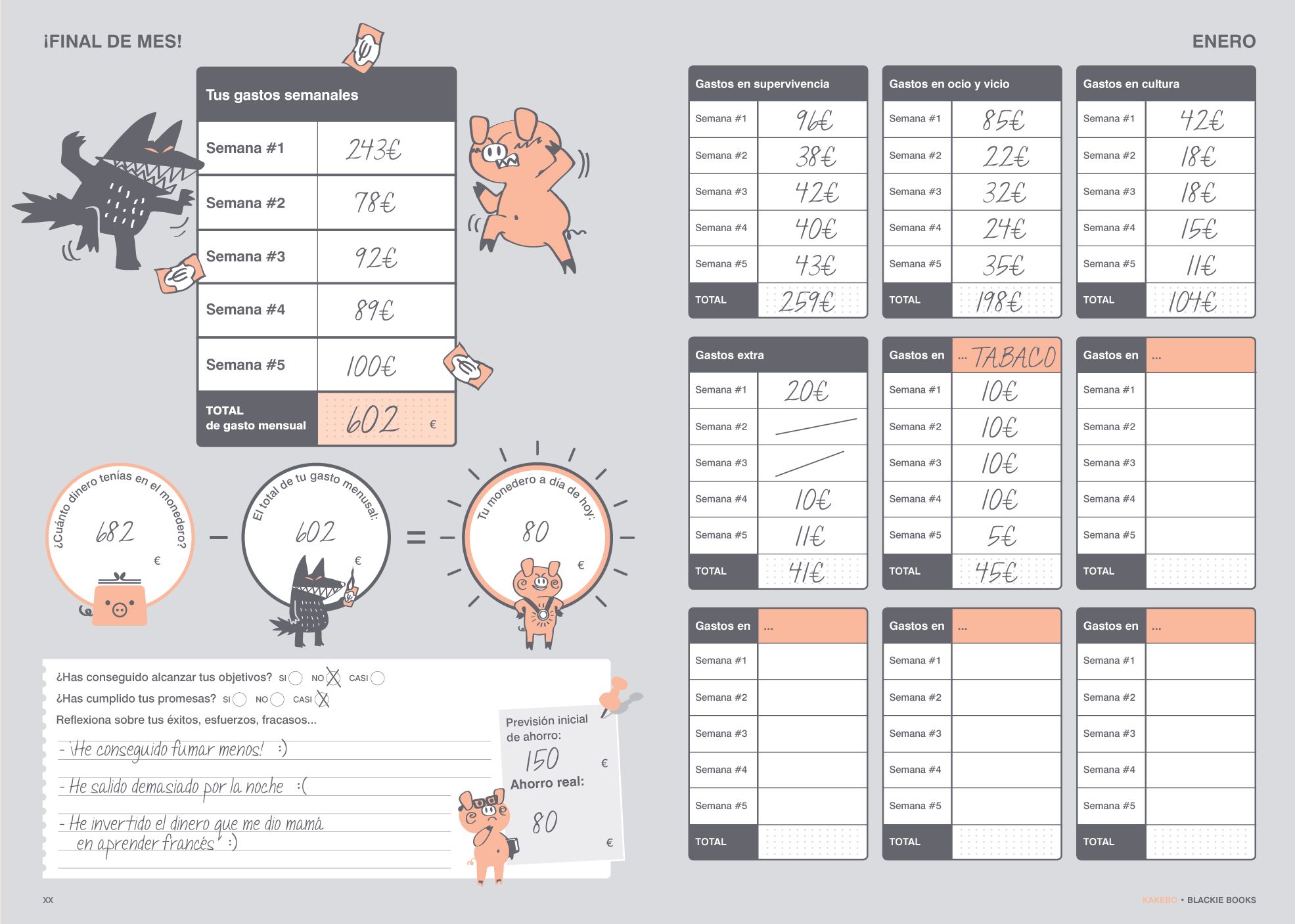

- During the month register the expenses in the different categories:

- Survival: food, pharmacy, transports, kids. Optional

- Optional: bars, restaurants, takeaway, shopping, cigarettes

- Culture: books, music, shows, movies, magazines

- Extra: irregular events such as gifts, repairs, furniture

- Establish the goals of the month (e.g. start to save for your summer vacation)

- Establish the promises of the month (e.g. stop smoking, buy gas from the cheapest station)

At the end of the month (and the year) the battle between the “savings pig” and the “expenses wolf” starts: the difference between the initial budget and the total monthly expenses will give you the monthly savings.

Food on focus

One thing that all kakeibos focus on is food costs, since food spending is both one of the biggest budget categories, and one of the easiest areas to cut down on costs. Generally a kakeibo categorizes food purchases by the nutritional type: carbohydrates, meat and fish, dairy and eggs, vegetable and fruit, etc. which also gives you a way to see if you are eating a healthy diet. More recently, easier kakeibos may divide it into larger categories like regular food, fun food (snacks and drinks), eating out, and so on. There are kakeibos that combine budgeting functions with meal planning and recipe tracking too.

Origins of the Kakeibo

The kakeibo has gained particular interest in Japan due to a variety of cultural and economic factors. A lot is owed to Hani Motoko, the first female journalist in Japan. She believed that financial stability was important for happiness, and decided to publish a kakeibo (accounting book designed for households) in a women’s magazine in 1904. After more than 100 years this book is still sold.

While bookkeeping might not be as popular as it once was due to a whole slew of cultural and economic factors, it hasn't faded out completely. Also, the recent economic downturn, for example, has encouraged cash-strapped families to economize as much as possible, often with help of a kakeibo.

Delayed gratification

Most children in Japan get their first training in personal finance at a young age from their parents. They are taught that the more money they save, the higher the quality of personal items they can buy in the future. It is common for Japanese parents to urge their children to keep their ‘otoshidama‘ (traditional cash gifts received from relatives and friends) in the bank to avoid impulse buying. Most parents instill in their children’s mind that borrowing money from people is frowned upon in Japanese society. So when there’s a chance, high school students get a part-time job to fund a purchase outside of the family budget. Over time, their money management skills improve. Thus, by the time a man starts his career and raises a family, he is well prepared to manage his personal finances.

If we look at some statistics, in the UK, 8 in 10 adults have less than £500 in savings and the average household saves only 8% of their earnings. The average American saves between 6% and 8% of their earnings. If we take Japan instead, households averaged 11.82% from 1970 until 2017, reaching an all time high of 60% in December of 2021.

The wife is in charge of the household budget

In a traditional Japanese family, a working father is either too busy or adverse to the trivialities of home finance therefore it is the duty of the mother (who may or may not work outside the home) to manage everything from cleaning to child rearing, including the finances. Therefore, the husband generally leaves his earnings in the hands of his wife, from which she gives him a monthly or weekly kozukai (小遣い), or "allowance", for drinking, eating out, gambling and so on. The wife is expected to take care of his entertainment budget in addition to any other financial obligations. She decides on how the money is spent, how to plan for big ticket purchases, even in many cases how money is invested. Financial products are often marketed with 'cute' themes, to appeal to a female audience.

Many magazines aimed at housewives include a giveaway version as a supplement in their December issues, for use in the coming year.

Why not an app?

There are plenty of computer programs, excel templates, and mobile phone apps floating around out there for the technology savvy housewife. There is one advantage of writing down amounts by hand though: it will give you a more tangible sense of how you're managing your money.

You want to start but don't know where? I wrote a book about it! You can grab in on Amazon.