Understanding Islamic Finance: a beginner's guide to ethical investing

The other day for first time I heard the term “Islamic Finance” and I got curious about it. I dug a bit about the topic, also thanks to the book “Understanding Islamic Finance” by Muhammad Ayub (which I used for some of the content in this post). and now I put together some key highlights for you. Now, I know that any topic involving religion can become controversial very quickly, hence the article is based entirely on what Scholars say. The post is entirely investment focused.

Islamic finance is gaining modern traction as one of the fastest-growing sectors in the global financial industry. Its assets are projected to reach a staggering $6.7 trillion by 2027 (Lseg). This growth isn't confined to Muslim-majority countries though; financial hubs like London, New York, and Hong Kong are integrating Islamic finance products into their offerings. But what exactly is Islamic finance, and how does it differ from conventional finance?

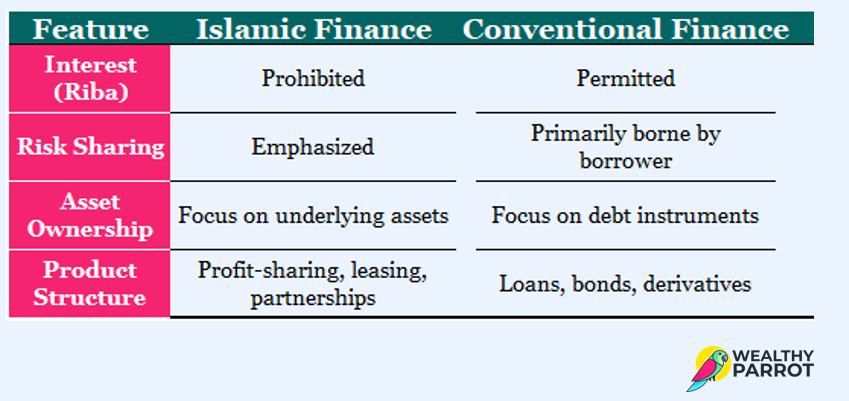

In a nutshell Islamic finance operates under Shariah, or Islamic law, which governs all aspects of a Muslim's life, including economic activities. The core idea is to conduct business in a manner that is ethical, just, and beneficial to society.

But let’s dive in!

Principles and practices

Islamic finance is founded on Sharia law, which provides guidance on various aspects of Muslim life, including financial transactions. A cornerstone of Islamic finance is the prohibition of Riba, which translates to "interest." To understand this, think of conventional finance where you borrow money from a bank and pay interest on the loan. This recurring interest payment, irrespective of the bank’s profit or loss, is considered Riba in Islamic finance (Abdullah Saeed, "Islamic Banking and Finance").

Instead of relying on interest, Islamic finance emphasizes risk-sharing and asset-based financing, structuring financial products around partnerships and shared ownership of assets. Let's dive into two key concepts:

- Shirkah (partnership): imagine two friends starting a bakery together. They invest capital, share profits based on a pre-determined agreement, and also bear any losses incurred. This partnership approach reflects the principle of Shirkah, ensuring that all parties are equally invested in the venture's success or failure.

- Asset-based financing: in Islamic finance, the focus is on actual ownership of an underlying asset. For example, a bank might purchase a piece of machinery and lease it out to a business, with ownership eventually transferring to the lessee upon full payment. This method ensures that financial transactions are backed by tangible assets.

Other important principles in Islamic finance include:

- Prohibition of riba (interest): as already mentioned charging or paying interest is forbidden. The rationale is that earning money from money, without any underlying productive activity, is exploitative and unjust. Instead, profit is earned through trade and investment in tangible assets.

- Risk sharing: Islamic finance contrasts with conventional finance by emphasizing risk sharing instead of risk transfer. This principle fosters a more equitable distribution of risk and reward between the parties involved in a financial transaction.

Fun fact: during the 2008 financial crisis, Islamic banks were relatively insulated from the subprime mortgage meltdown because of their asset-backed lending practices.

- Ethical investments: investments must align with Islamic ethical standards, avoiding businesses involved in alcohol, gambling, pork products, and other activities considered harmful or unethical. This is similar to the concept of ESG (Environmental, Social, and Governance) principles.

- Prohibition of Gharar (excessive uncertainty): transactions involving excessive uncertainty or speculation are prohibited. Contracts must be clear and transparent, minimizing the risk of deceit or misunderstanding.

Why interests are not allowed

One of the most interesting part is the rejection of the concept of interests (riba). Islamic scholars sustain that the current economic system suffers from two main problems: inefficient management that ignores poverty and exploitation, and the way money, finance, and financial markets distribute resources and wealth. Interest, a key feature in borrowing money, is seen as a major hurdle in achieving economic fairness.

The interest-based system creates a situation where debt becomes unrepayable. This enriches a small group while leaving the majority struggling. Poor countries are particularly affected by this "debt trap," where they constantly borrow to pay off existing debt, hindering economic growth and poverty reduction efforts.

Easy access to credit through interest-based systems encourages wasteful spending by individuals and governments. This reduces savings, real investments, and job opportunities. When combined with inflation, it creates a recipe for economic chaos. The burden falls on the poor and middle class, hindering national savings and trapping economies in a cycle of poverty and injustice.

Excessive debt in poor countries is stifling economic growth and undermining efforts by organizations like the World Bank and IMF to reduce poverty. It distorts payment systems, disregards fair income distribution, and burdens future generations with repayment.

Islamic lending, on the other hand, is considered a virtuous act. The lender offers goods or money without expecting any compensation beyond the return of the principal. The lender even shares the burden if the loaned amount loses value due to inflation.

What happens if a debtor doesn’t pay then?

In Islamic finance, handling late repayment balances ethical compassion and practical measures. Debtors facing genuine hardship are given leniency, rescheduling, or even forgiveness of debt, while mechanisms like charity clauses act as deterrents against willful default. Legal recourse is available for deliberate default, ensuring fairness and justice in financial dealings.

When the debtors face genuine difficulties, creditors are encouraged to show leniency and compassion:

- Rescheduling the debt: if a debtor cannot repay on time due to genuine hardship, the creditor can extend the repayment period without additional charges.

- Forgive a portion or the entirety of the debt as an act of charity. This is seen as a noble act that brings great reward in the Hereafter.

Islamic finance generally prohibits the imposition of additional interest or penalties for late payment as it falls under the category of riba (interest), which is strictly forbidden. However, there are alternative mechanisms:

- Charity clause: Some Islamic financial contracts include a clause where the debtor agrees to pay a certain amount to charity if they default. This serves as a deterrent against willful default without constituting riba.

- Legal recourse: creditors have the right to seek legal recourse in the case of deliberate default or fraud. This might involve taking the matter to an Islamic court or arbitration body, which will assess the situation and determine a fair course of action based on Islamic law.

- Husnal Qadha (gracious payment of debt): Islam encourages debtors to repay their debts promptly and even go beyond what is due if they can. This concept, known as Husnal Qadha, reflects the debtor's gratitude and ethical commitment.

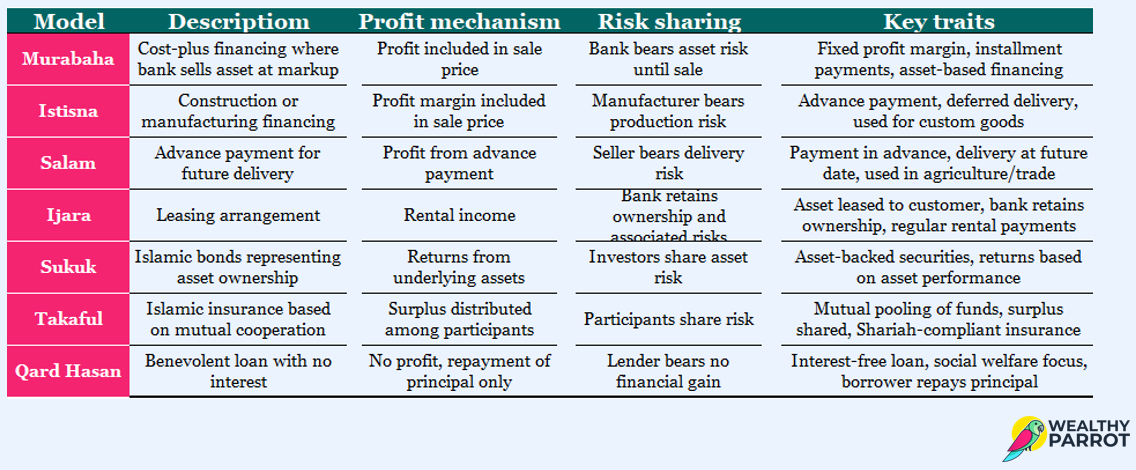

Key financial products in Islamic finance

Given the principles that Sharia-compliant products must follow, it’s no surprise that the financial products are different. In most cases it’s a readaptation of standard products, with the caveat that the investor does not get cash inflow in the form of interest, but as surplus.

Let’s take a look at the main products.

Sukuk (Islamic Bonds)

Sukuk are Islamic financial certificates, similar to bonds in conventional finance, that comply with Sharia law. They function quite differently from conventional bonds though.

Fun fact: The first-ever Sukuk issuance wasn't for a building or infrastructure project! It was used to finance the refurbishment of the Dome of the Rock in Jerusalem in the 7th century.

Imagine Company A, which builds shopping malls, needs funds for a new project. They issue Sukuk. Investors who purchase these Sukuk essentially become part-owners of the mall. The mall generates rental income, which is then shared with Sukuk holders as profit. This differs from a conventional bond, where investors receive a fixed interest payment regardless of the mall's performance. This profit-sharing approach aligns with the Riba prohibition

Fun fact: Islamic finance isn't just for Muslims. Non-Muslim countries like the UK have issued a £200 million sovereign sukuk in 2014 to build rental properties.

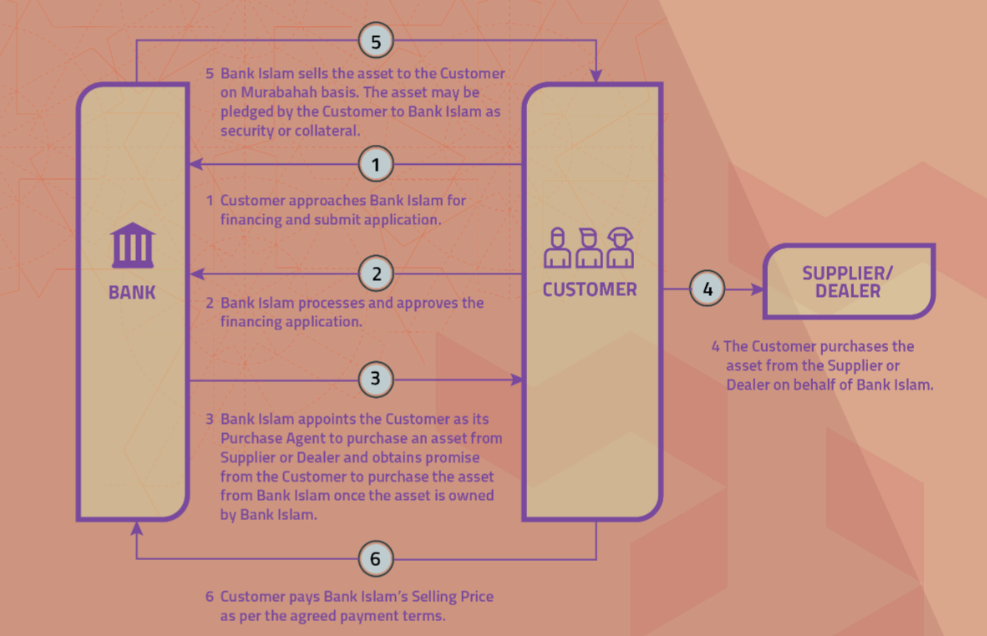

Murabaha (Cost-Plus Financing)

With Murabaha the financier buys an asset and sells it to the customer at a profit margin (that replaces the interest component) agreed upon in advance. The financier’s profit is built into the sale price, which the customer pays in installments, making it similar to a conventional loan but without interest.

In countries like Malaysia and the UAE, Islamic mortgages have become quite popular: the bank buys a property and sells it to the customer at a profit, paid in installments.

Fun fact: there are several Islamic equity indices too e.g. S&P500 Shariah Index or FTSE Shariah China Index.

Mudarabah (Profit-Sharing Agreement)

Mudarabah is similar to a venture capital or private equity in conventional finance. With a Mudarabah, one party provides capital while the other provides expertise and management. Profits are shared periodically between the parties as per pre-agreed ratios, while losses are borne solely by the capital provider (unless they are due to the negligence or misconduct of the manager). The manager loses the effort and time invested but not the capital.

At the end of the investment term, the initial capital is returned to the investors, possibly along with a final profit distribution.

Musharakah (Joint Venture)

Imagine a group of investors coming together to fund a new startup. Profits are distributed based on pre-agreed ratios, and losses are also shared proportionally. Similar to dividends, profits are distributed periodically to the investors and upon completion of the investment term, the initial capital is returned, along with any remaining profits.

Ijara (Leasing)

This is similar to a car lease in conventional finance, but with a key difference. In Ijara, the bank purchases the car and leases it to you for a pre-determined period with fixed monthly payments. Ownership remains with the institute until the end of the lease term, at which point the customer may have the option to buy the asset.

Takaful (Islamic Insurance)

Derived from the Arabic word "kafala," meaning "guaranteeing each other," Takaful is a cooperative system where participants contribute to a common fund to protect each other against specific risks. – basically an Islamic alternative to conventional insurance. Conventional insurance operates on a risk transfer model, where the insurer takes on the risk in exchange for premiums. Takaful, however, is a cooperative model, sharing both risk and reward among participants.

You can find a summary of the major financial products below.

Benefits of Islamic finance

Islamic finance promotes financial inclusion by providing financial services to those who avoid conventional finance due to religious reasons. This is particularly significant in Muslim-majority countries where a large portion of the population may be underserved by conventional banks.

Fun fact: estimates suggest there are around 1.9 billion Muslims around the world. This constitutes roughly 24.9% of the global population, making Islam the second-largest religion after Christianity (Wikipedia).

The risk-sharing principles of Islamic finance can contribute to greater financial stability. By avoiding excessive leverage and speculative activities, Islamic finance institutions are less likely to be exposed to the kind of systemic risks that led to the global financial crisis of 2008.

The ethical nature of Islamic finance appeals not only to Muslims but also to a growing number of socially conscious investors. By focusing on ethical and socially responsible investments, Islamic finance can attract a wider audience.

Challenges in Islamic finance

It’s not all roses though. Creating standardized regulations for Islamic finance is complex, given the diversity of interpretations of Shariah law across different regions. This can lead to inconsistencies and complications in cross-border transactions.

While Islamic finance is growing, it still faces challenges in penetrating non-Muslim majority markets. There is often a lack of awareness and understanding of its principles and benefits among potential customers.

Innovating financial products that comply with Shariah law can be challenging. Financial institutions must ensure that new products do not violate Islamic principles, which can limit the scope of innovation.

Conclusion

Islamic finance offers a unique and ethical alternative to conventional finance, rooted in principles of fairness, transparency, and social responsibility. By promoting financial inclusion, stability, and ethical investing, Islamic finance has the potential to contribute significantly to the global economy - especially given the sheer size of the Muslim population. Whether you are an investor looking for ethical investment opportunities or a business seeking Shariah-compliant financing options, Islamic finance might be an option for you.