The hardest part of FIRE isn't saving, it's spending

I know what you're thinking.. This article might be the opposite of what I've been preaching so far. But hear me out, you might be surprised.

A couple sits across from Ramit Sethi on his podcast. They have $2 million in the bank. And they want to know why they can't bring themselves to order the nicer bottle of wine at dinner.

Two million dollars. That's more than most people will earn in a lifetime. And yet this couple - educated, financially literate, objectively wealthy - feels guilty about spending $15 extra on a Barolo.

If you think this is an isolated case, think again. The FIRE community (that's Financial Independence, Retire Early, for the uninitiated) is having a collective reckoning. JL Collins, the godfather of "just buy VTSAX and chill," recently wrote that those pursuing financial independence follow "a path of deprivation and delayed gratification so ingrained they lack the ability to shift gears when it comes time to spend." The Mad Fientist, another FIRE icon, set a 2026 New Year's resolution not to save more - but to make sure his spending money is actually gone by December.

Read that again. A man who retired early with more than enough money has to force himself to spend it.

Something is broken. And it's not the math.

You trained yourself too well

The uncomfortable truth about the FIRE journey is that the exact skills that got you to financial independence might be the ones sabotaging your retirement.

Think about it. For 10, 15, maybe 20 years, you optimized every line item. You tracked spending like a hawk. You celebrated months where you saved 60% of your income and felt a pang of shame when it dropped to 45%. You turned frugality into an identity - perhaps even adopted a structured method like Kakeibo to make every purchase intentional.

And then one day, the spreadsheet says you're free. The portfolio is big enough. The safe withdrawal rate checks out. You've crossed the finish line.

Except your brain didn't get the memo.

If you've read my pieces on the psychology of saving and spending triggers, you know how deeply money habits root themselves in our psychology. The accumulation phase doesn't just build wealth - it builds neural pathways. Saving becomes automatic. Spending becomes the thing that requires effort.

And here lies the paradox that nobody warns you about: the transition from saver to spender is harder than the transition from spender to saver.

The numbers say you're under-spending

Let's get out of our heads for a moment and look at the data. According to research from the Employee Benefit Research Institute, nearly half of retirees agree - at least somewhat - that they spend less than they could because they're worried about running out of money. Not "some" retirees. Not the ones with small portfolios. Nearly half across the board, including those with more than enough.

Meanwhile, only 11% of retirees describe themselves as having a "spending mindset." A full 38% identify with a "savings mindset" even after leaving work behind. The habit persists long after the paycheck stops.

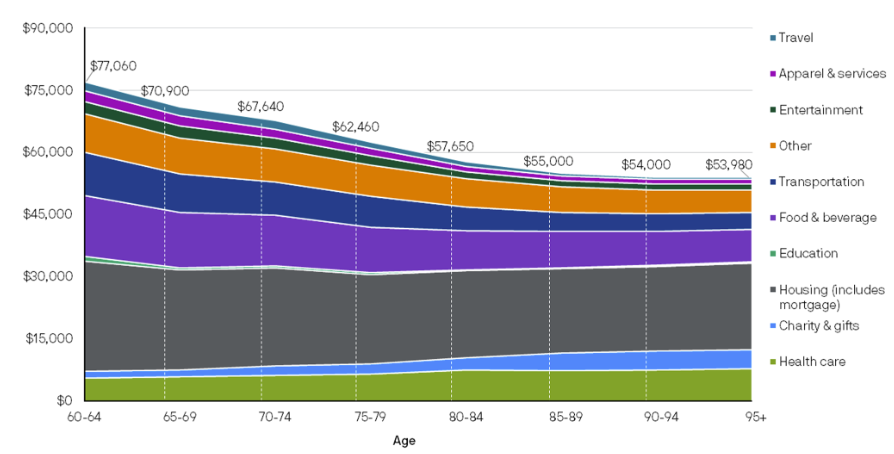

And the spending itself? It drops. A lot. Research from J.P. Morgan shows that average retiree spending declines by more than 30% between ages 60 and 85.

Some of that is natural - fewer commuting costs, a paid-off mortgage, less need for work clothes. But much of it isn't about need. It's about fear.

The Federal Reserve's Survey of Consumer Finances shows something even more revealing: median net worth actually increases with age. It's $124,200 for ages 45-54, climbs to $187,300 for 55-64, rises again to $224,100 for 65-74, and peaks at $264,800 for those 75 and older. People aren't spending down their wealth in retirement. They're still building it - on autopilot, out of pure habit.

William Bengen, the financial planner who literally invented the 4% rule, found that the average portfolio using his conservative 4.7% withdrawal rate ended a 30-year retirement with over $530,000 still in the account. That's not a rounding error. That's a life's worth of unkept promises to yourself.

More than half a million dollars that could have been trips taken, experiences shared, generosity extended, or simply a little less anxiety about the price of wine at dinner.

The five biases keeping your wallet shut

So why is this happening? Why do intelligent people with sufficient money struggle to spend it?

Behavioral finance gives us a roadmap. And if you're a diligent saver, you're going to recognize yourself in at least three of these.

Loss aversion is the big one. Daniel Kahneman's research showed that the pain of losing $100 is roughly twice as intense as the pleasure of gaining $100. Now apply that to a portfolio. Every dollar you spend feels like a loss. Every restaurant bill is a tiny wound. The portfolio going from $1,200,000 to $1,199,850 after a nice dinner registers in your brain as damage - even though it's 0.01% of your net worth.

Then there's status quo bias - the preference to keep things exactly as they are. You've been saving for 15 years. That's the status quo. Spending disrupts it. And disruption, even positive disruption, triggers discomfort.

Anchoring plays a nasty trick too. You hit your FI number - say, $1.2 million - and that number becomes sacred. Dipping below it feels like failure, even though it was always meant to be spent. The target you worked so hard to reach becomes a floor you refuse to break through.

Regret aversion keeps you paralyzed. What if you spend now and the market crashes next year? What if you take that trip and then need the money for a medical emergency? The fear of making the "wrong" spending decision leads to making no decision at all - which, ironically, is its own kind of wrong decision.

And finally, identity attachment. For years, you were the person who saved. The person who packed lunch while colleagues ate out. The person who drove the old car. Frugality isn't just what you did - it's who you became. Spending feels like betraying yourself. (If you've ever felt a twinge of pride watching your emergency fund grow past what you'd ever need, you know this feeling.)

Michael Pompian, in his work on behavioral finance and wealth management, draws a useful distinction here: cognitive biases (like anchoring) can be corrected with information. Emotional biases (like loss aversion and identity attachment) require structural changes - not just knowing better, but building systems that make spending easier. That distinction matters for what comes next.

Your money has a shelf life

Bill Perkins makes a provocative case in Die with Zero that money has what he calls peak utility - a period when each dollar spent generates the maximum amount of life satisfaction. And that peak, according to his analysis, arrives much earlier than most people think. Not at 70. Not at 65. Somewhere between your late 20s and mid-40s, when you have the health, energy, and social connections to extract maximum value from experiences.

Now, Perkins' framework is deliberately provocative (he's essentially arguing you should spend more in your 30s and 40s, not less). You don't have to agree with his timeline to acknowledge the core insight: money spent at 45 is not the same as money spent at 75.

Consider this: when a woman named Virginia Colin finally inherited $130,000 from her mother at age 49, she called it "a nice bonus." But 15 years earlier, when she was raising four children alone near the poverty line, that same money would have been life-changing. Her father had hoarded it out of fear of future medical costs. The money arrived decades after it could have made the biggest difference.

The retirement research backs this up with what planners call the "spending smile." Retirees typically move through three phases:

- The Go-Go years (roughly 60-70) - active, traveling, spending on experiences. This is when you actually want to do things. Spending is highest.

- The Slow-Go years (70-80) - activity declines, spending follows. Fewer big trips. More time at home. Costs drop naturally.

- The No-Go years (80+) - spending falls significantly, outside of healthcare. The desire and ability to spend diminishes even if the money is there.

Bureau of Labor Statistics data confirms this pattern. Average annual spending drops from roughly $85,000 at ages 55-64 to about $55,000 at 75 and beyond - a 34% decline. The money you're "saving" for later years? You probably won't spend it then either.

The most attentive of you might argue that income also declines with age. True! However, that "missing" income was partly diverted to retirement (savings, investments, 401k, etc.), and in most cases that money should have grown by time your retire. Plus even the wealthiest retirees still see expenditures slide after ate 75.

Perkins calls the emotional return from past experiences the "memory dividend" - the idea that a great experience at 35 pays psychological returns for decades, while the same experience at 75 pays returns for a much shorter window. A backpacking trip through Southeast Asia at 30 gives you 50 years of stories. The same trip at 80 - well, your knees might have other plans.

The point isn't to be reckless. It's to recognize that money sitting in a brokerage account at 82 has already failed at its job.

The European dimension

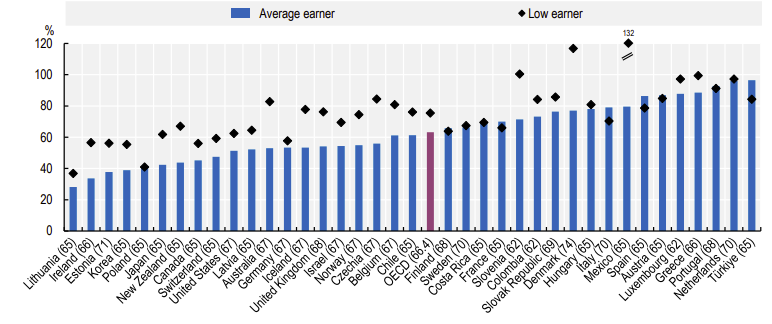

Now, if you're reading this from Europe, you might be thinking: "This sounds like an American problem. We have state pensions."

Fair point. And it's true - the safety net looks different on this side of the Atlantic. Most EU countries provide state pensions that replace 40-70% of pre-retirement income, depending on the country. In the Netherlands it's around 70%. In Germany, roughly 50%. Italy and France sit somewhere in between. That's a guaranteed income floor that most Americans simply don't have.

But here's the thing: the spending psychology problem isn't about the size of the safety net. It's about the psychology of the saver.

European FIRE pursuers face the same identity trap. You still spent years optimizing, cutting, investing. You still built neural pathways around delayed gratification. And when the state pension kicks in alongside your portfolio income, you still struggle to shift gears.

In fact, there's an argument that strong state pensions make the problem worse, not better. The EBRI found that retirees with pensions spent down only 4% of their non-pension assets over 18 years. Four percent. In nearly two decades. If you know you have a guaranteed €1,500-2,000 per month coming regardless, your portfolio becomes even more clearly "extra." And "extra" money is psychologically harder to spend than "necessary" money.

Whether your floor is Social Security, a state pension, or a combination of both, the behavioral challenge is the same. The spreadsheet says spend. Your brain says save. The pension just gives your brain one more excuse.

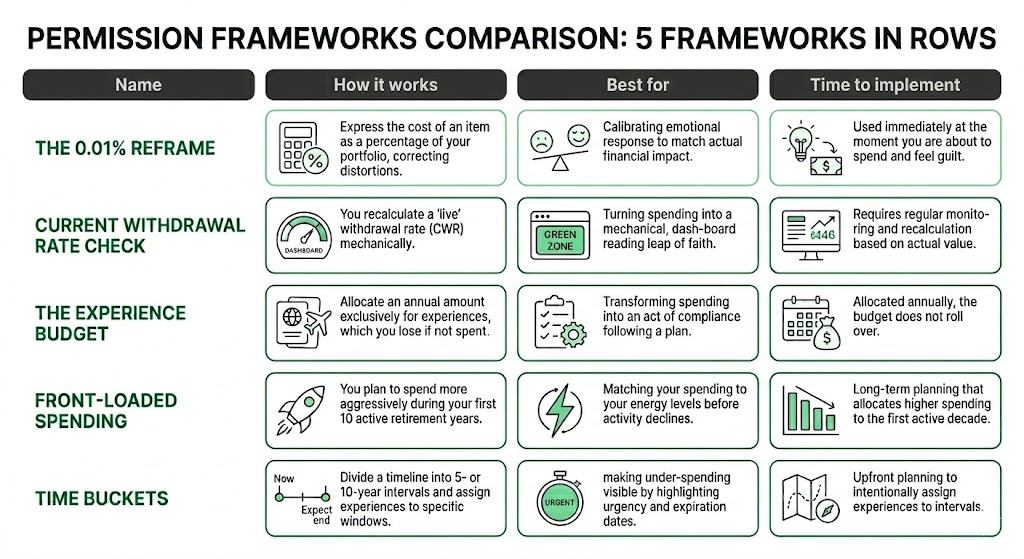

Permission frameworks that actually work

Knowing you have a spending problem is useful. But knowing isn't the same as doing. You need tools - practical, repeatable frameworks that give your brain permission to spend without triggering a panic response.

Here are five that work.

The 0.01% reframe

This one comes from the Mad Fientist, and it's beautifully simple. When you're about to spend money and feel the guilt rising, express the cost as a percentage of your portfolio.

That $150 dinner? If you have a $1.5 million portfolio, that's 0.01%. One hundredth of one percent. Your portfolio fluctuates more than that before you finish your appetizer. The $3,000 vacation? That's 0.2%. The market moves that much on a random Tuesday.

This doesn't mean spend recklessly. It means calibrate your emotional response to match the actual financial impact. Your brain is treating a 0.01% expense like a 10% loss. The reframe corrects the distortion.

The current withdrawal rate check

William Bengen, the 4% rule inventor himself, suggests monitoring your Current Withdrawal Rate (CWR) - not a fixed percentage set once at retirement, but a live number recalculated regularly based on your actual portfolio value.

If your CWR is at 3.2% and your historical safe rate is 4.7%, you have a 1.5 percentage point gap. That's not a cushion to feel smug about. That's money you're choosing not to spend. Every year that gap persists, you're voluntarily under-living.

The CWR turns spending from a leap of faith into a dashboard reading. Is the number in the green zone? Then spend. It's that mechanical.

The experience budget

Instead of budgeting against spending (the traditional model), create a budget for experiences. Allocate a specific annual amount - say, $10,000 or €8,000 - exclusively for experiences. Travel, courses, dinners, gifts, adventures.

The key: if you don't spend it, you lose it. It doesn't roll over. It doesn't get "saved." It's use-it-or-lose-it by design.

This works because it transforms spending from an act of consumption into an act of compliance. You're not indulging. You're following the plan. And if there's one thing a FIRE devotee respects, it's following the plan.

Front-loaded spending

Bengen's research supports a front-loaded withdrawal scheme - spending more aggressively in the first 10 active years of retirement, then tapering as activity naturally declines. This isn't reckless; it's matching your spending to your energy.

If you're 50 and newly FI, years 50-60 are your Go-Go years. That's when to take the big trips, renovate the house, try the expensive hobby. By 70, your spending will naturally fall. Plan for that reality instead of spreading your money evenly across decades - which, as we've seen, just means under-spending early and sitting on a pile at 85.

Time buckets

This framework from Die with Zero replaces the vague bucket list with something more intentional. Draw a timeline from your current age to your expected end, divided into 5- or 10-year intervals. Then assign specific experiences to the interval where they make the most sense.

Hiking Patagonia? That's a 50-60 bucket, not a 75+ bucket. Learning piano? Any bucket works. Taking your grandkids to Disney? Better do it while they're young enough to care (and while you can keep up).

The power of time buckets is that they make under-spending visible. When you see "sailing the Greek islands" sitting in your 55-65 bucket and you're already 58, the urgency becomes real. The experience has an expiration date - and so does the money you'd spend on it.

But I'm saving for a reason

Now, before this turns into a blanket "spend everything" manifesto, let's pump the brakes. Because there's a perfectly valid objection sitting in the room: not everyone wants to die with zero.

Some people are saving for their children's education. Others want to leave an inheritance - a head start they never had. Maybe you're building toward a property purchase, or funding a future business, or simply want the deep-down security of knowing your grandkids won't struggle.

These are real goals. Legitimate goals. And this article isn't arguing you should abandon them.

Here's the distinction that matters: there's a difference between intentional saving and fear-based hoarding.

Intentional saving looks like this: "I want to leave €200,000 to each of my two kids, so I've ring-fenced €400,000 in my plan. The rest is mine to live on." That's a decision. That's a number. You can work with that.

Fear-based hoarding looks like this: "I want to leave something for the kids, so... I'll just keep saving. All of it. Just in case." There's no number. No target. No point at which it's enough. The "something for the kids" becomes an infinitely expandable excuse to never enjoy a cent.

The irony is that people who hoard out of vague legacy anxiety often leave random amounts, at random times, to people who may not even need it - what Bill Perkins calls the Three Rs of inefficient inheritance. Your 60-year-old children inheriting $800,000 when they've already built their own wealth isn't a gift. It's a transfer that arrived 30 years too late to make a real difference in their lives. Federal Reserve data backs this up: the peak age for receiving an inheritance is around 60, well past the point where money has its highest utility.

If legacy matters to you - and it should, if that's your value - then plan for it explicitly. Put a number on it. Fund it. Protect it. And then give yourself permission to live on the rest.

And here's a tool that can make that permission feel a lot more real: life insurance.

A term life policy doesn't just protect your family if something happens to you. It also protects your psychology while you're alive. If you know that a €500,000 policy covers the inheritance you want to leave, your portfolio stops being your children's future money. It becomes yours again.

Think of it as a psychological firewall. The policy handles the legacy. The portfolio handles the living. The two jobs are separated, and your brain no longer has to treat every restaurant bill as money stolen from your kids' inheritance.

This works both ways, too. If your biggest fear is "what if I spend too much and then get sick?" - a critical illness rider or a long-term care policy addresses that specific anxiety without requiring you to hoard an extra $300,000 "just in case." You're outsourcing the catastrophic risk to an insurer and freeing up capital for actual living. It's what insurance was designed for.

The specific products and costs vary widely depending on where you live - premiums, tax treatment, and coverage types differ across countries. But the principle is universal: insurance lets you separate the protection function of money from the enjoyment function. And that separation is often the permission slip your brain needs.

The same goes for any financial goal. A safety cushion? Great - define its size. A dream property? Calculate the deposit. Your kids' university? Estimate the cost in today's money and set it aside.

What you'll often find is that once you put actual numbers on your goals, the remaining portfolio is larger than you expected. The "saving for the kids" that felt like it required your entire net worth turns out to need 20-30% of it. The rest? That's yours. And it's waiting for you to use it.

Saving with purpose and spending with intention aren't opposites. They're partners. The person who has clearly defined what they're saving for is, paradoxically, the person most equipped to spend freely on everything else.

The real risk

Every financial planning article you've ever read warns about the risk of running out of money. It's the boogeyman of retirement planning. Outliving your portfolio. Eating cat food at 90. The horror.

And to be clear: that risk is real. I'm not dismissing it. If your portfolio is tight, your withdrawal rate is high, and your safety margin is thin, this article isn't for you - yet. Get the fundamentals right first.

But for the millions of diligent savers who have done the math, who have built the cushion, who have ring-fenced their legacy goals - there's an opposite risk nobody talks about: under-living with too much.

Bengen's research found the average retiree following the 4% rule ends up with more money than they started with. After 30 years of withdrawals, the typical outcome is more wealth, not less. The conservative scenario that everyone plans for - the one where markets crash at the worst possible time - is the exception, not the norm.

One in three retirees actually increases their assets over time. They enter retirement with a plan to spend down, and leave with more than they started. That's not prudence. That's a spending failure disguised as financial success.

That leftover money isn't a sign of good planning. It's a sign that you spent decades sacrificing for a future you then refused to enjoy. And if science is right that money can buy happiness - when spent on the right things - then under-spending isn't just a financial mistake. It's a life one.

If you've spent years building financial independence, you've already proven you can delay gratification. You've proven you can sacrifice. You've proven you're disciplined. And if you've put clear numbers on your legacy goals, you've proven you care about the people who come after you.

Now prove you can enjoy what's left.