How to teach financial wellbeing to your children

There is an old saying that goes like: "Money can't buy happiness". My answer to it is "Then try to live without money". Jokes aside, there are a couple factors to consider:

- The context you live in: being poor, wealthy or even rich depends on culture and country. Someone that is considered wealthy in Europe might be considered uber rich in Africa. If your friends are all making $1M a year and you make "only" $500k, you might consider yourself poor.

- Money has a deep psychological effect on our mind: we become happy when we get it and sad when we don't have it.

- Even what we buy can change our perception and make us happy short term or long term.

All in all, there is no universal magic number that everybody can use as target, but it's very personal and it will vary with age. So what's a better way to understand if you are on the right track? Financial wellbeing.

What is financial wellbeing?

The Consumer Financial Protection Bureau (CFPB), to try and answer what is financial wellbeing, did nearly 60 hours of open-ended interviews to get the consumer perspective. Their research suggests that financial well-being can be defined as a state of being wherein you:

- Have control over day-to-day, month-to-month finances: it means check every day or weekly or monthly your own finances with a notepad/spreadsheet/app, etc, to eventually build a simple income statement. This is to make sure you have control of your finances.

- Have the capacity to absorb a financial shock: this is a lot to do with the what if mindset. anything from having a life insurance to have enough cash to cover unexpected expenses (e.g. the fridge breaks, the bills increase, special medical treatments, etc.).

- Are on track to meet your financial goals: goals differ and depend on a mix of factors, from personal wishes to the context when you're raised.

- Have the financial freedom to make the choices that allow you to enjoy life: lifestyles vary a lot, someone likes to live in the city centers and go out for dinner in a posh restaurant every Friday, others prefer the calm of the countryside and go jogging every evening.

Financial behavior

Four types of behaviors will support you to achieve financial well-being:

- Make money management part of your routine and standardize the process, to leave no space for decision-making shortcuts. A very practical example is to save every month and stick to your investment strategy no matter what "noise" such as friends or news might tell you.

- Do your own financial research and keep learning: the world is full of advisors, but often the best non-bias advice will come from your own research. Staying up-to-date will also allow you to take calculated risks and navigate through the noise in social media or news.

- Plan and set financial goals: give yourself sensible targets that you can work against. $1M Net worth? Zero debt? Save €10k per year? Any flavor counts. This will give you purpose and structure to help you drive any single financial decision you'll take.

- Live in line, or better below, your financial means: if every time you get a salary increase or a new source of income you increase your lifestyle too, your savings will always stay stable or even decline. This will drag you away from your financial goals. Instead, try to optimize your expenses to increase your savings rate.

Personal traits

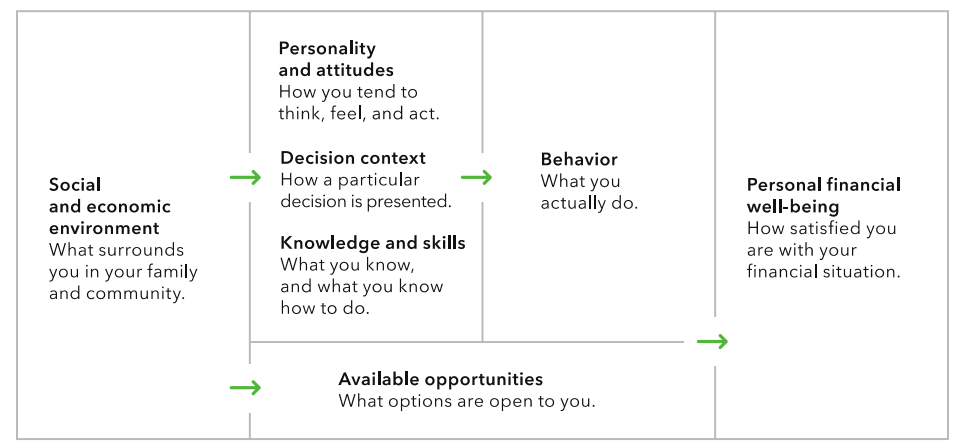

Personal attitudes and beliefs, non-cognitive skills, and personality traits all influence financial behavior and play a role in mediating the connection between knowledge and behavior. Based on CFPB's research, they hypothesize that the following four types of personal traits are likely to affect financial well-being through their influence on behavior and/or preferences and expectations:

- Comparing yourself to your own standards, not to others (internal frame of reference)

- Being highly motived to stay on track in the face of obstacles (perseverance)

- Having a tendency to plan for the future, control impulses, and think creatively to address unexpected challenges (executive functioning)

- Believing in your ability to influence your financial outcomes (financial self-efficacy).

Financial wellbeing in America

After defining what financial wellbeing is, CFPB also performed a survey to understand how is the situation in USA, and the key findings were quite interesting:

- The average financial well-being score for U.S. adults is 54 on a scale that falls between zero and 100. About a third of all adults in the United States have financial well-being scores of 50 or below, about a third have scores between 51 and 60, and about a third have scores of 61 or above.

- Financial well-being scores reflect real differences in underlying financial circumstances. Scores of 50 or below are associated with both a high probability of struggling to make ends meet and of experiencing material hardship.

- Savings and financial cushions provide the greatest differentiation between people with different levels of financial well-being. The average financial well-being for adults with the lowest level of savings (less than $250) is 41, compared to 68 for adults with the highest level of liquid saving ($75,000 or more).

How to teach financial wellbeing to your kids

- Have control over day-to-day, month-to-month finances: normally kids around 7-8 years have enough math knowledge to do this. If they get pocket money, they could calculate how much they make and how they spend it. If they don't, you can involve them in some family budget calculations or even come up with a puzzle for them to solve.

- Have the capacity to absorb a financial shock: For kids, we don't have to worry them with catastrophes, but you can teach them to set aside some money for unforeseen events, or for example, if they want to go on vacation with their friends, to cover part of the cost (e.g. train/flight).

- Are on track to meet your financial goals: For kids, one way is to use as goal the new toy they want, or the new bike. The important point is to set a deadline too: "the financial goal is to buy a used car with a budget of 7000 usd, within 1 year from getting the driving license". When the goal is hard enough, this will trigger the imagination (e.g. start selling used toys) but also will act as mental brake to avoid impulse buying. This could also act as deterrent and to understand if the "financial goal" they set was really important.

- Have the financial freedom to make the choices that allow you to enjoy life: this one can take many shapes, but when I was a child, it meant that I didn't have to ask my parents for money for small things such as buying some candies or picture cards.

If you want to know more on financial education for kids, check you my article on how to teach your children how to save.