Wings of wealth: reader interviews on financial freedom #1

Wings of Wealth is a series of interviews with the Wealthy Parrot readers, focusing on their experiences and insights regarding financial freedom. If you want to tell your story, feel free to write me to info@wealthyparrot.com.

Hi Ludwig and welcome to the Wealthy Parrot! As you know, we are all about financial independence here, but before we dive into the technical details of your story, would you mind sharing a bit about yourself and your background?

Sure, no worries. My name is Ludwig, I’m born and raised in Sweden, I am 33 years old, married and have two children. We currently live in Germany, about an hour south of Berlin. I don’t want to be too open with details, since I’m still working and will probably continue for some time. What I can say though is that I work with performance improvement and business transformation in the German automotive industry as a project and PMO manager. I’ve been in this job for three years and enjoy my work.

Later in the fall, me and my wife will celebrate 10 years of being on the journey to financial independence, a journey we started back in 2013 when we bought our first ABB stocks listed on the Stockholm stock exchange. Now in spring she will leave the corporate world forever. I, myself, will continue working for a while, I don’t know exactly for how long, but I still want to develop my skills set a little bit more and take our portfolio one step further.

Seeing that you started your journey so early in your life, what would you say got you on the path to financial independence?

Looking back and reflecting upon my story and what brought me here, I’ve come to realize that me getting onto this path is a pretty reasonable response to the experiences I made early in life. You see, I grew up in a family of five, i.e. my parents and my two siblings. Sometime around the time I turned ten, my father’s mental health started deteriorating. He worked in telecommunications as a contractor, and was having increasing difficulties holding down assignments. This left the entire family in a constant state of anxiety, because we never knew when dad would have a job and for how long before he would be between contracts for months, sometimes even years, at a time. It was at this time, in my early teenage years, that I promised myself to never be poor.

The second intervention came early in the career of my wife, we had just moved in together and I was still a student. She had started working for her parents in their family business right after having sold it to a Private Equity fund, with the mission to scale the business of course. But the profitability did not increase as expected and she was laid off on the spot. It was at this point that she realized the risks inherent in being dependent on a paycheck for your living, and got on the financial independence train together with me.

What does financial independence mean to you personally?

Being financially independent means for me to be able to provide a decent lifestyle for myself and my family at minimal effort and risk indefinitely.

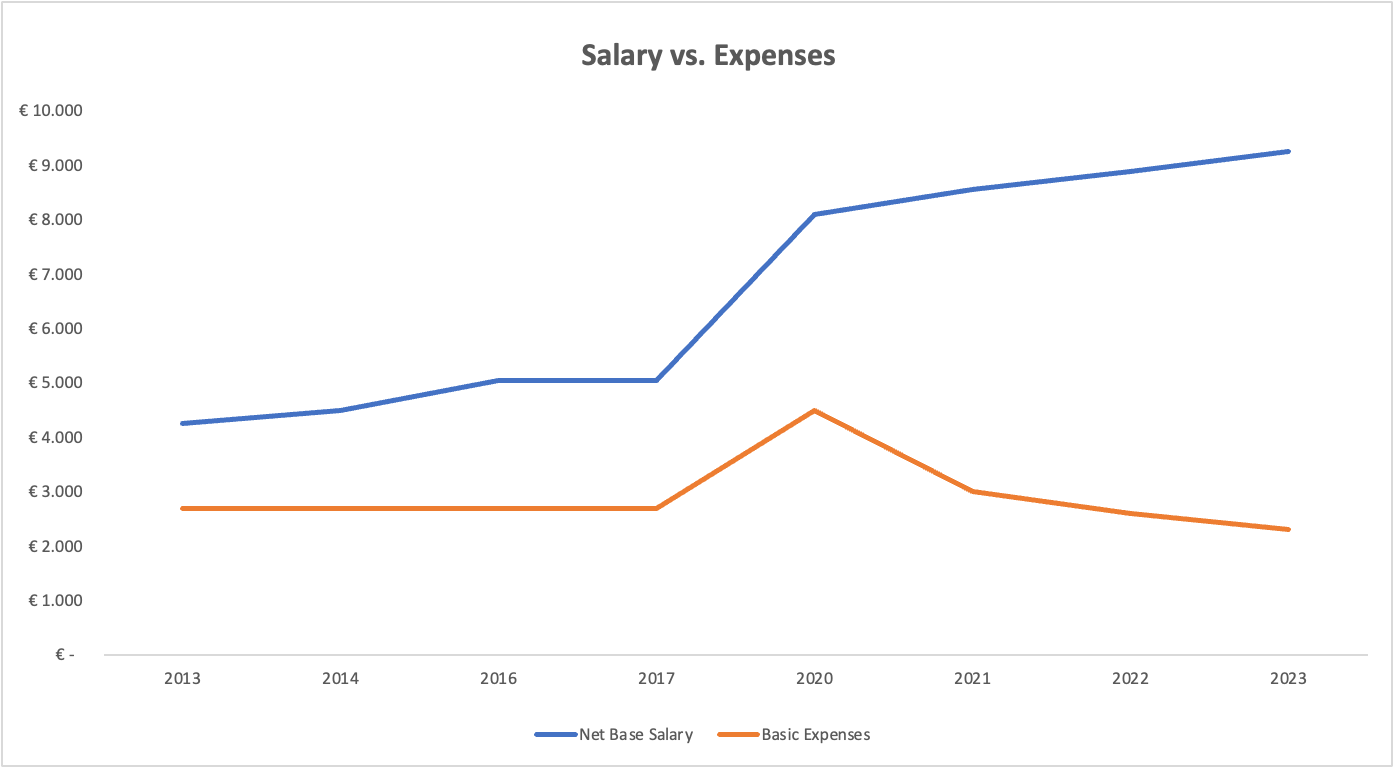

For us as a family, we have found that we need roughly a cash flow of 4k euro a month to finance the lifestyle we want here in Germany. Our needs are split according to the following:

- Fixed Costs (interest payments, electricity, kindergarten) of 1k euro

- Amortization (long term and low interest debt only of course) at 1k euro

- Living Expenses (food, clothing, entertainment, transport) of 2k euro

Since we are still working, we do not yet utilize the possible ways to finance ourselves yet, but if we would it would be through the following:

- Apartment Rental: 1k euro

- Side Hustle: 1k euro

- Equity Portfolio: 2k euro

This places us roughly at the median income of a household of our size, and we live in a comparatively affordable part of the country.

What steps have you taken towards achieving financial independence?

We have literally done everything you can imagine to secure our financial independence! The basics of course are to get insight and transparency into your household expenses. I started tracking all expenses in a spreadsheet as a student back in 2007. Thereafter, I took targeted steps to increase my income without also increasing my costs of living. For me this meant doing my MBA and moving abroad to Germany, where jobs generally are more well paid, taxes are lower (for families) and costs are much, much lower than back home in Stockholm. We started out with a savings rate of around 25% living in Stockholm ten years ago and will probably finish 2023 with having saved around 70% of our net income this year.

In addition to this, I’ve of course also experimented with basically every asset class available to us retail investors, from gold to art to small venture capital investments through index funds, exchange-traded funds, property and cryptocurrencies. Soon, or probably in 2024 due to the current market downturn, I will qualify as a semi-professional investor in Germany and will gain access to even more exotic investment options such as Private Equity and Venture Capital funds!

How do you approach budgeting and managing your expenses?

There are two parts to this, one is the rational part of budgeting and managing expenses. For this we use my good old excel spreadsheet which tracks daily expenses, fixed expenses, projections for the next 3 years and a cash flow calculation for the year. Having done it for over 15 years now gives me and my wife excellent command of what we spend.

Secondly, there is the emotional part, and it is much trickier. It’s about really distilling down what is important for you and your family and building a life around that. If reducing expenses makes you unhappy and leaves emotional needs out, you and your family won’t be successful long term.

For us, in the end, it meant literally travelling the world to find the best place to raise a family, and through moving as much as we have, we’ve been able to figure out what we need. For us this means living somewhere calm, safe and quiet, without the need to have a car, with a high living standard. It should clearly be a couple of thousands of kilometres south of Sweden because the cold and darkness makes me depressed. Lastly, the city should have a few Michelin-starred restaurants and be within commuting distance of a large urban area with advanced jobs in case I would like to work. All of this we found in East Germany, south of Berlin.

What strategies or investments do you consider essential for building wealth and achieving financial independence?

The most essential element is to understand exactly how safe the stock market really is an investment. The ones in the FI / FIRE community, like us, speak repeatedly about the so-called Safe Withdrawal Rate (SWR). Essentially it is a statistically derived formula saying that, based on historical data, you can withdraw 4% of a diversified stock market portfolio, without it depleting in the next 30 years as good as guaranteed.

Now, these 4% are the lowest rate we’ve observed in the last hundred years in the American equities market, and this is if you retire off your portfolio right before the Great Depression in the 1930s or the runaway inflation following the oil shocks in the 1970s. Probably it would even have survived the tech bubble and subprime housing crises at the beginning of the millennia, but it is still too early to tell. Thus, the probability is high that you will be able to withdraw significantly more per year, in fact the average SWR is around 7 to 8% for a globally diversified portfolio. Given this low degree of risk and ease of access, building an equity portfolio should, in my mind, definitely be one of the cornerstones of reaching financial independence.

Secondly, my recommendation would be to build up separate income streams, or side hustles, based on your interest and passions. My wife works remotely in her own business as an accountant and she loves it, even if it’s just for a few hours a week it gives her more than it costs in terms of effort and energy, while reducing the risks in our household economy substantially. For myself, I am seriously considering starting a coaching and consulting activity to support others on the path to FI, which within a year should be able to provide a cash flow of another 1k euro to our household.

Lastly, do not underestimate geo arbitrage! There are probably a lot of places around the world that can afford an amazing quality of life at a much lower cost and required investment than where you currently are, and you get the adventure free of charge! When we travelled the world we took note of the quality of life and the costs of different locations, and oddly enough, I have found that the costs of living here in East Germany matches locations in South East Asia such as Thailand and the Philippines, which is amazing. Here we spend about half as much as we did in Stockholm, while having an apartment twice as large and providing for a household of four instead of just the two of us in Sweden.

Surely, during this journey, there must have been challenges and difficulties, how did you manage them to stay on track?

Since we started there has probably only been one time when I thought that the adventure would have been ruined for us, and that was a combination of factors that came together during Covid, and it was my burnout late 2020. We had just moved from Paris to Frankfurt with our son, who was six weeks old. I moved into a job that was significantly more challenging than what I had done previously, in a new industry and in a new country.

Covid struck, and, unrelatedly, my son started having kidney infections. He was colicky and did not sleep and we were locked in our new apartment with his screams. This caused me to have difficulties performing at work, and as a response my boss started performance manage me. The symptoms I started experiencing were textbook burnout, with pressure around my chest and difficulties breathing, inability to sleep, inability to focus, constant headaches, dizziness, and panic attacks on a regular basis.

My wife told me to speak to a doctor and see a therapist, the doctor told me to make a change in life and the therapist told me that if I continue like this for another week, my recovery time will not be six months but three years, if I ever will be able to get back to normal.

Luckily, the HR lady at my employer was able to take me out of the running business and gave me my first performance improvement project, and let me work as much as I could. So I started working one hour a day, then two hours a day, then after around half a year I could work for almost a full working day. But it probably took me the last three years to feel that I also can perform at a high level through this working day.

Market fluctuations you survive as long as you do not sell in panic, you just need to sit still (or even better - invest more!), but if you get wiped out completely (by say health issues or a divorce or something like that) - you are out of the game and no skills in earning, saving or investing will save you.

How do you allocate your capital today?

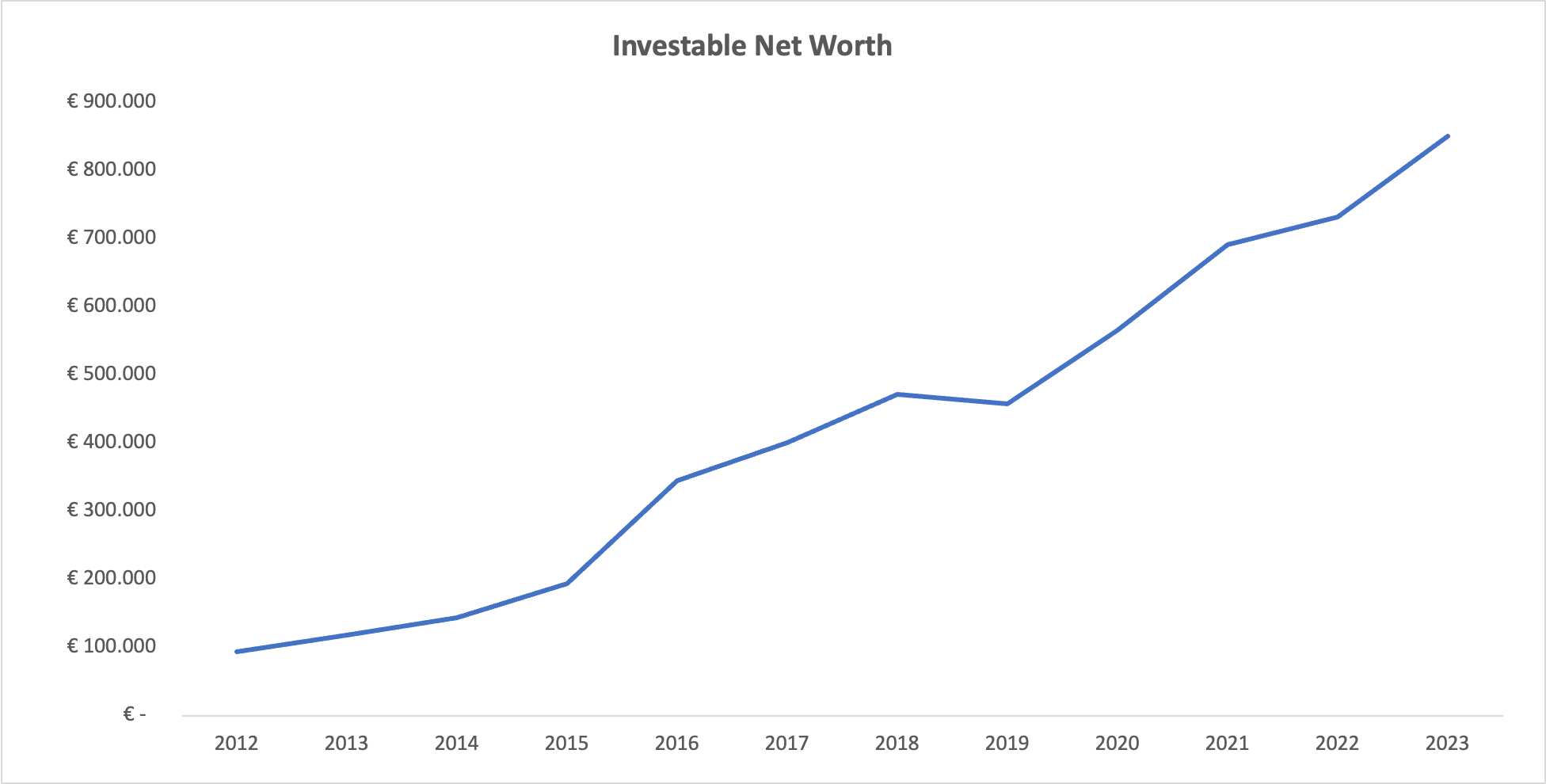

Our capital allocation is a consequence of both the history of how we have moved across Europe in the last six years since leaving Sweden, as well as the investment philosophy I have developed.

First of all, we want to own the properties we live in, but not use real estate as an investment in terms of individual items. The benefits of owning your home is that you are made immune from rent inflation, and up until recently, it also gave you a great opportunity to leverage the investment through dirt cheap mortgages. Today we own the apartment in Leipzig and the one where we used to live in in Frankfurt. We maxed out the available mortgage and locked the rate below 1% per year for a decade for both properties.

The drawbacks of owning real estate, especially as an investment, is the lump risk stemming from just one item in the portfolio. This combined with the efforts of managing the property, makes it unattractive as an investment in general in my view.

Secondly, we move as much money as possible into a combination of three exchange traded funds. These are the three iShares ETFs basically covering the MSCI All Countries World Index Investable Markets Index (ACWI IMI) which allocates capital according to market capitalization of all the world's exchange-listed equities. The only drawback of this approach is that it is susceptible to market bubbles, and longer term I would like to move the money to a professional manager which can allocate according to the free cash flow of the companies, this reduces bubble risk while delivering the same average return. Once one reaches 1M EUR in investable capital this option starts to be interesting for both you as an investor as well as the manager.

Thirdly, we allocated about 5% of our total net worth to speculative assets. This is where I have played around with things like gold coins, crypto and pieces of art. Since crypto became easier to invest in as a retail investor in the last couple of years with the rise of centralized exchanges, I decided to build up a crypto portfolio, which I follow every day out of excitement, and if Bitcoin goes to 100k USD in the next bull run maybe I will finally be able to convince my wife to get a 2019 BMW M2 Competition (or even the new BMW Z4 Touring Coupe if it goes into production!) for me to drive her around in - but it is not something I depend on.

Having reached financial independence at this, still relatively, young age, after all, what are your plans for the future?

In the immediate term, we are at the point where we are saving the cash buffer necessary to tie us over for at least one year without any cash flow at all, which we will have done by fall. Given our current income streams, this means that we could live without drawing down the portfolio for about two to three years. By the end of 2023 our portfolio will be the size I need it to be and we will pretty much have been able to prove that our income streams as well as living expenses deliver what we need them to do.

So, what’s next? This is a tricky question. About a year ago I was updating our projections and it dawned on me - that in 18 months we will, with high probability, have reached our target. So what do I do? And all the dreaming I have been doing for nearly a decade had to materialise into plans. And my answer is, still, that I don’t really know.

First of all, I still have a need to feel competent and that I bring value to people. Also, I’m quite loyal to my current boss (who was the HR lady that helped me back in 2020, she got promoted by the way), and would like to finish the performance improvement program I started back then. Thus, I see myself continuing doing more or less the same thing I’m doing today for another, say, 12 to 18 months.

What about longer term? Well, even if I decide to pull the plug and fulfil my wife’s dream of being at home more than 4 nights a week, after 6 to 12 months everything in the apartment will be fixed, every box of stuff will be organized and every dust grain will be vacuumed. And I will be, I fear, the fat guy sitting on the sofa.

Is that the kind of role model I want to be for my son? Is that the kind of man I want my daughter to look for? I’m not so sure. We need purpose in life, and it has to be genuine, which is generally not something you read or think your way to. Which means that I’m currently feeling my way through towards the next thing that attracts me, the next thing that obsessively grabs me - just like FI and the FIRE movement did 10 years ago. Let’s see what I find.