Barbarians at the gate: how to buy a $25 Billion company with almost none of your own money

In October 2022, Elon Musk bought Twitter for $44 billion. You probably remember the headlines.

What you might not remember is the fine print: Musk borrowed $13 billion of that money. But he didn't get stuck with the loan. Twitter did. Not Elon. The company itself had to make the interest payments - roughly $1.2 billion per year - on the debt used to purchase it. That's about half of X's entire annual revenue going straight to lenders.

Think about that for a second. You walk into a car dealership, buy a car, and somehow convince the car to pay its own monthly installments.

That's a leveraged buyout (LBO). And Twitter is far from the first company to get the treatment. (If terms like "debt," "equity," and "balance sheet" already make your eyes glaze, our Accounting 101 guide breaks all of that down.)

Buying a company with someone else's money

An LBO is deceptively simple. A buyer - usually a private equity firm or wealthy investor - purchases a company using a relatively small amount of their own cash and a massive pile of borrowed money. Then they transfer that debt onto the company they just bought.

The best analogy? Buying a house with a mortgage.

You put down 20-30% and borrow the rest. The property's value and your future income secure the loan. If you picked a good house in a good location, it appreciates over time, you pay down the mortgage, and eventually sell for a profit.

Now replace "house" with "entire company" and "your income" with "the company's cash flow." That's the LBO playbook.

Except there's one crucial twist. When you buy a house, YOU make the mortgage payments. In an LBO, the house makes its own payments.

The math behind this is what makes LBOs so seductive. Say you buy a company worth $100 million. You put in $30 million of your own money and borrow $70 million. Five years later, the company is worth $150 million. You sell it, pay back the $70 million loan, and pocket $80 million - a 167% return on your original $30 million. If you'd paid all cash? That same $50 million gain would be a 50% return.

Leverage amplifies everything. That's the magic. It's also the danger.

How the sausage is made

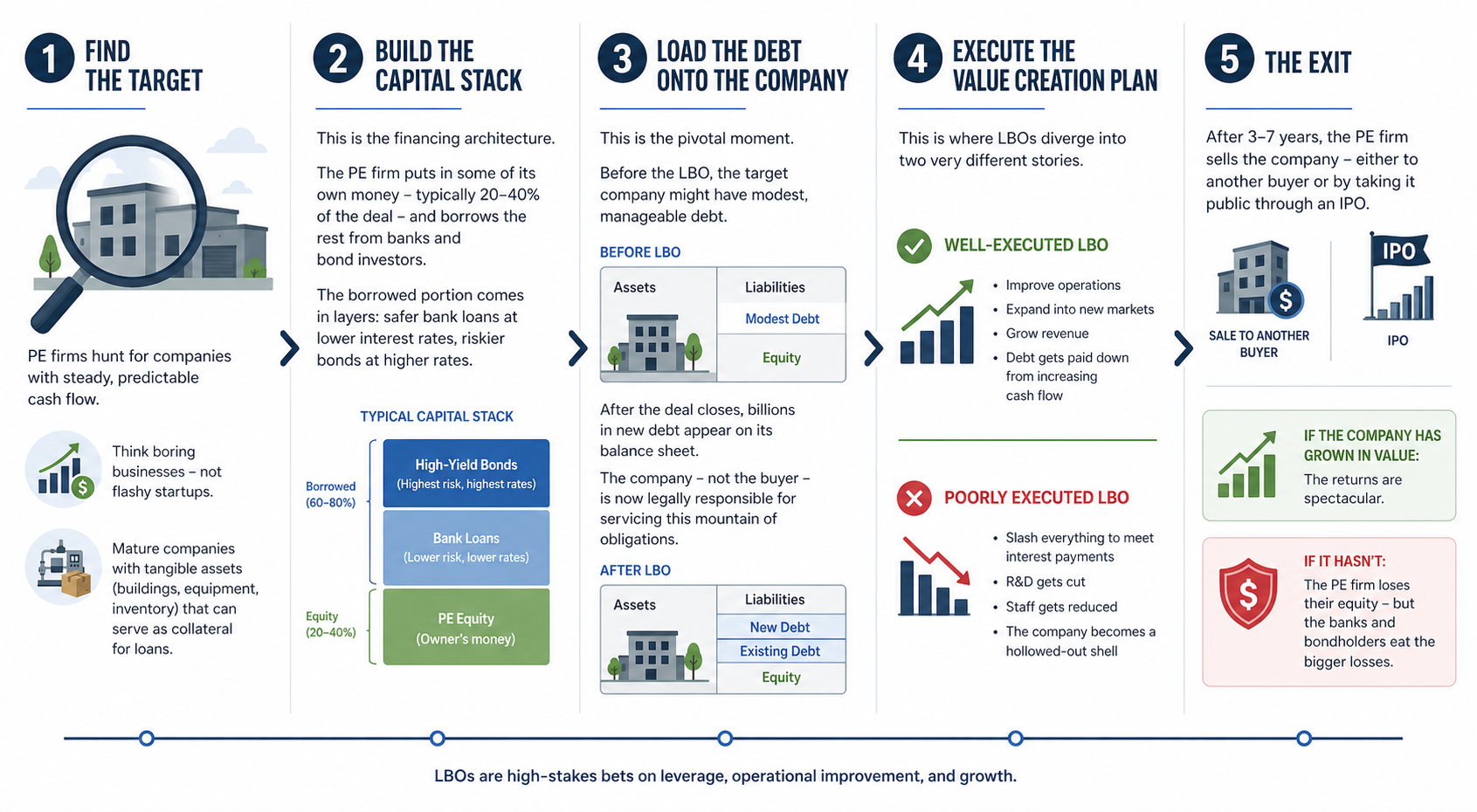

So what actually happens when a private equity firm executes an LBO? Five steps.

Step 1: Find the target. PE firms hunt for companies with steady, predictable cash flow. Think boring businesses - not flashy startups. Mature companies with tangible assets (buildings, equipment, inventory) that can serve as collateral for loans.

Step 2: Build the capital stack. This is the financing architecture. The PE firm puts in some of its own money - typically 20-40% of the deal - and borrows the rest from banks and bond investors. The borrowed portion comes in layers: safer bank loans at lower interest rates, riskier bonds at higher rates.

Step 3: Load the debt onto the company. This is the pivotal moment. Before the LBO, the target company might have modest, manageable debt. After the deal closes, billions in new debt appear on its balance sheet. The company - not the buyer - is now legally responsible for servicing this mountain of obligations.

Step 4: Execute the value creation plan. This is where LBOs diverge into two very different stories. In a well-executed LBO, the new owners improve operations, expand into new markets, and grow revenue. Debt gets paid down from increasing cash flow. In a poorly executed one, the new owners slash everything to meet interest payments. R&D gets cut. Staff gets reduced. The company becomes a hollowed-out shell.

Step 5: The exit. After 3-7 years, the PE firm sells the company - either to another buyer or by taking it public through an IPO. If the company has grown in value, the returns are spectacular. If it hasn't, the PE firm loses their equity - but the banks and bondholders eat the bigger losses.

One more thing about the fees: no matter what happens to the company, the investment banks that arranged the financing collect their cut upfront. Win or lose, Wall Street gets paid.

Now let's see how this plays out in practice.

The original barbarians

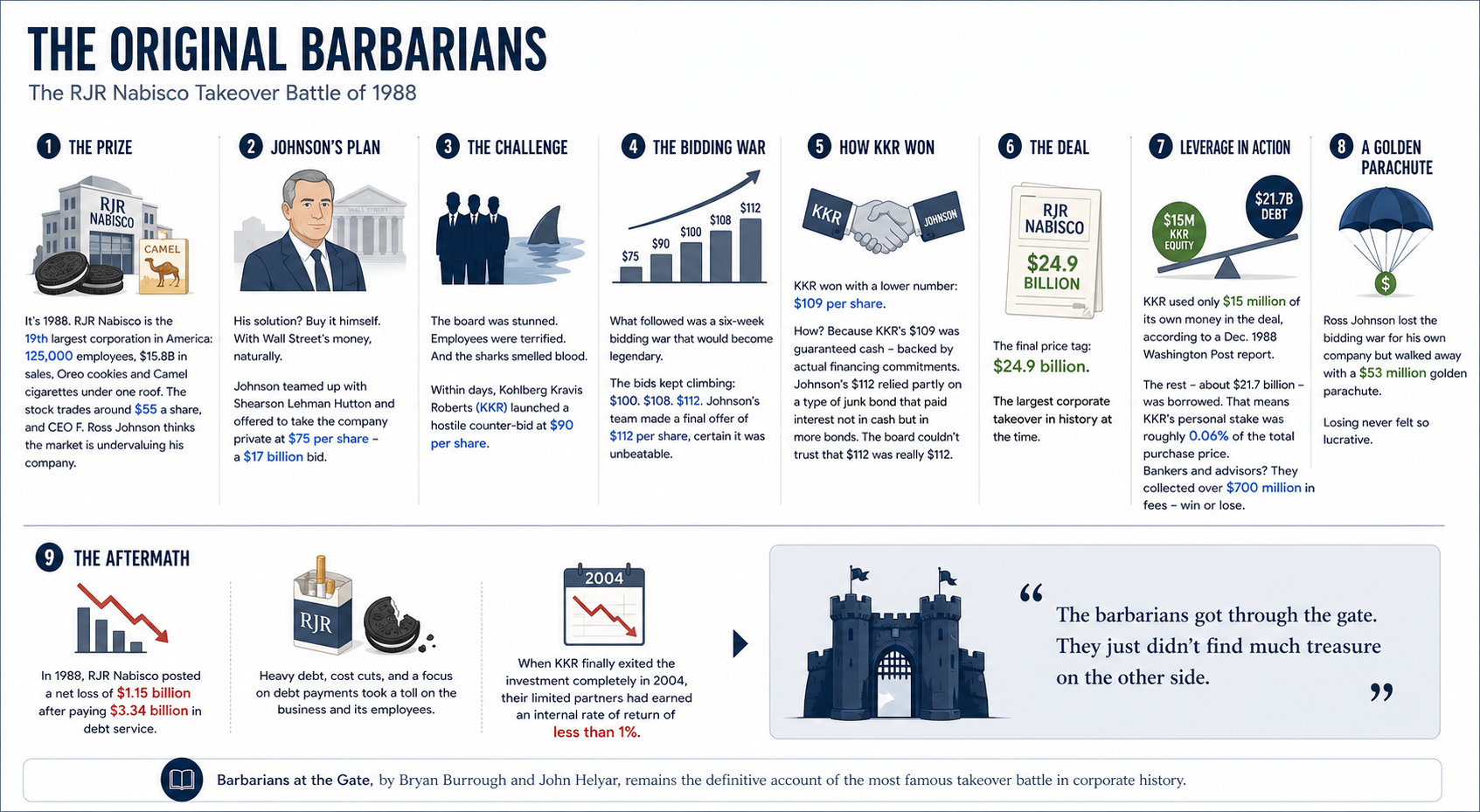

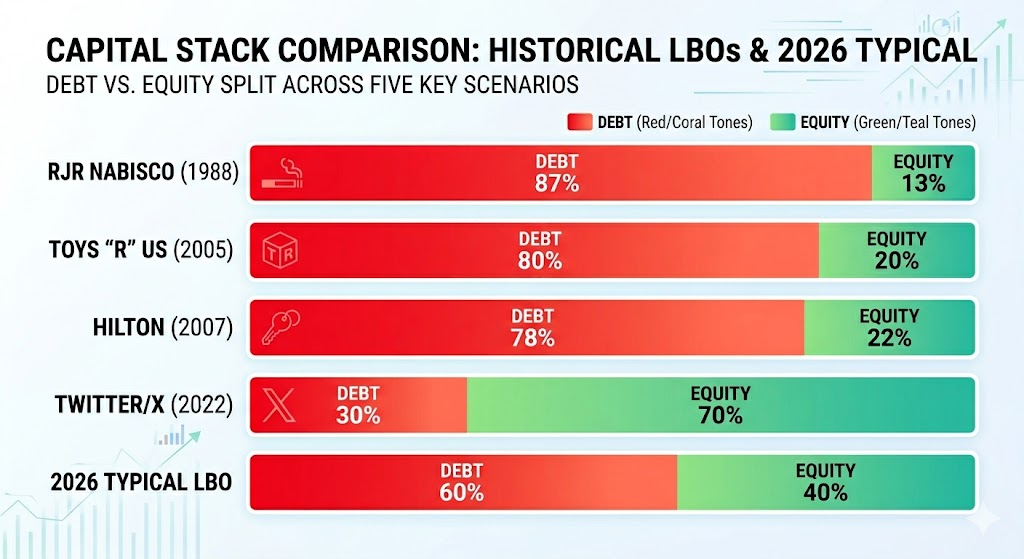

It's 1988. RJR Nabisco is the 19th largest corporation in America: 125,000 employees, $15.8 billion in sales, Oreo cookies and Camel cigarettes under one roof. The stock is trading around $55 a share, and CEO F. Ross Johnson thinks the market is undervaluing his company.

His solution? Buy it himself. With Wall Street's money, naturally.

Johnson teamed up with Shearson Lehman Hutton and offered to take the company private at $75 per share - a $17 billion bid. The board was stunned. Employees were terrified. And the sharks smelled blood.

Within days, Kohlberg Kravis Roberts (KKR), the private equity firm that had essentially invented the modern LBO, launched a hostile counter-bid at $90 per share. What followed was a six-week bidding war that Bryan Burrough and John Helyar later immortalized in their book Barbarians at the Gate.

The bids kept climbing. $100. $108. $112. Johnson's team made a final offer of $112 per share, certain it was unbeatable.

KKR won with a lower number: $109 per share. How? Because KKR's $109 was guaranteed cash - backed by actual financing commitments. Johnson's $112 relied partly on a type of junk bond that paid interest not in cash but in more bonds. The board couldn't trust that $112 was really $112.

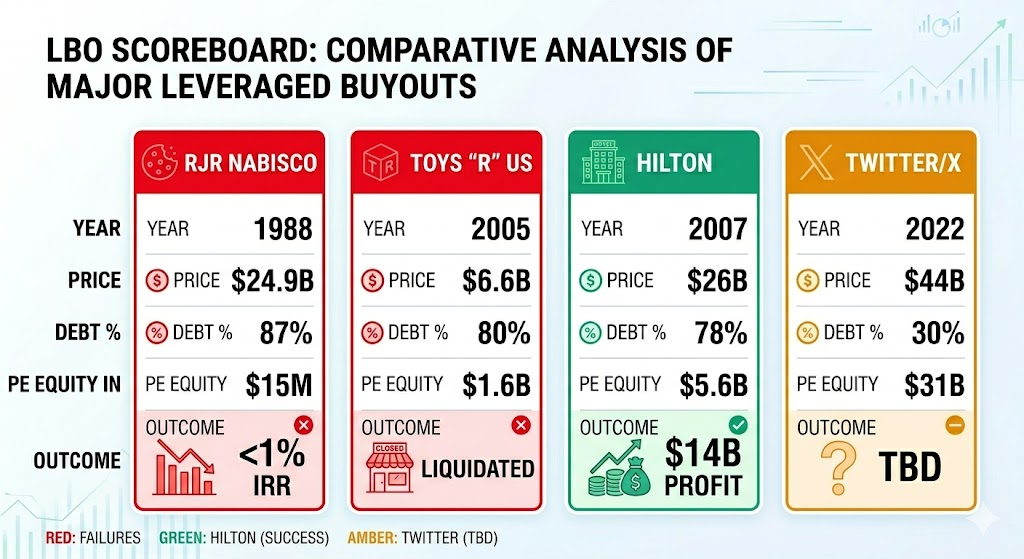

The final price tag: $24.9 billion. The largest corporate takeover in history at the time.

And KKR used only $15 million of its own money in the deal, according to a December 1988 Washington Post report. The rest - about $21.7 billion - was borrowed. That means KKR's personal stake was roughly 0.06% of the total purchase price. The bankers and advisors? They collected over $700 million in fees - win or lose.

Ross Johnson lost the bidding war for his own company but walked away with a $53 million golden parachute. Losing never felt so lucrative.

The aftermath for RJR Nabisco was less glamorous. In 1989, the company posted a net loss of $1.15 billion after paying $3.34 billion in debt service. When KKR finally exited the investment completely in 2004, their limited partners had earned an internal rate of return of less than 1%.

The barbarians got through the gate. They just didn't find much treasure on the other side.

The debt that kills

If RJR Nabisco was a cautionary tale about disappointing returns, Toys "R" Us was something worse: a story about debt killing a profitable company.

In 2005, KKR (yes, the same KKR), Bain Capital, and Vornado Realty Trust bought Toys "R" Us for $6.6 billion. They put in roughly $1.6 billion of their own money and borrowed $5.3 billion. Overnight, the company's capital structure flipped from 30% debt / 70% equity to 78% debt / 22% equity.

Now here's what makes this story maddening. Toys "R" Us was profitable. Operating income was growing. The stores were generating revenue. The toy market wasn't dying - kids still wanted toys.

But the company was bleeding $400 million per year in interest payments alone.

That's $400 million that couldn't go toward building an e-commerce platform. Couldn't go toward renovating stores. Couldn't go toward competing with Amazon, which was rapidly eating the toy retail market. Planned technology upgrades and digital partnerships were repeatedly shelved as cash was hoarded for interest payments.

In September 2017, Toys "R" Us filed for bankruptcy under a $5.2 billion debt pile. By 2018, the company was liquidated entirely. 800 stores closed. 33,000 people lost their jobs.

The private equity firms that bought it? They collected hundreds of millions in management fees during their ownership. KKR and Bain Capital eventually contributed $20 million each to a hardship fund for displaced workers - roughly 0.3% of the original deal value.

The core lesson is brutal in its simplicity: if every dollar of profit goes to servicing debt, nothing is left to invest in the future. And a company that can't invest in its future eventually doesn't have one.

Not all barbarians: the Hilton exception

It would be unfair to paint every LBO as a corporate raid. Some genuinely create value.

In 2007, Blackstone bought Hilton Hotels for $26 billion - one of the largest hotel LBOs in history. The financing was aggressive: $20.5 billion in debt (78.4% of the deal), with Blackstone putting in $5.6 billion of equity.

The timing could not have been worse. The deal closed months before the 2008 global financial crisis. Hotel occupancy rates cratered. Revenue plummeted. The deal looked like a disaster.

But Blackstone played the long game. They restructured the debt at a discount, removing immediate interest pressure. Then they invested in the business. Under CEO Christopher Nassetta, they shifted toward a franchise-heavy "asset-light" model - fewer owned hotels, more licensing - and expanded the global room count from 480,000 to over 665,000.

In December 2013, Blackstone took Hilton public in what was then the largest hotel IPO ever. They continued selling shares over the following years, finally exiting completely in 2018. Total profit: approximately $14 billion on a $5.6 billion equity investment - a 3.6x return over 11 years. Bloomberg called it "the most profitable private equity deal in history."

The difference between Hilton and Toys "R" Us wasn't just luck. It was what the owners did after they signed the check. One set of owners invested in the business. The other extracted from it.

Why this matters to you

You might be thinking: "I'm not buying a $25 billion company anytime soon. Why should I care?"

Three reasons.

First, LBOs are everywhere. Private equity doesn't just buy Fortune 500 companies anymore. It buys veterinary clinics, dental practices, nursing homes, apartment buildings, and local newspapers. If you work for a company that gets acquired by a private equity firm, understanding LBO mechanics helps you read the tea leaves. Sudden cost-cutting? Deferred maintenance? Rising debt on the balance sheet while management collects bonuses? Those are warning signs.

Second, leverage is the same force that powers your mortgage, your student loans, and your margin investing account. Understanding how it amplifies returns - in both directions - is one of the most important financial lessons you can learn. Leverage doesn't create value. It magnifies whatever's already there: good decisions and bad ones alike.

Third, just look at Twitter. Musk's deal loaded $13 billion in debt onto a company that then slashed 80% of its workforce to stay afloat. By 2024, Fidelity had slashed X's estimated value to $9.4 billion - a nearly 80% decline from the $44 billion purchase price. The story of leverage is always the same story. It just keeps finding new characters.

Practical takeaways

- A leveraged buyout uses borrowed money to buy a company, then makes the company itself pay back the debt - like convincing the house to pay its own mortgage

- The math is seductive: small equity investments can produce massive returns when things go well (see Hilton's $14 billion profit)

- The math is deadly when things go poorly: Toys "R" Us was profitable but drowned in $400 million annual interest payments

- Watch for LBO red flags if your company gets acquired: sudden cost-cutting, deferred investment, rising debt ratios, all profits going to debt service instead of growth

- Not all LBOs are destructive - the difference is whether new owners invest in the business or extract from it

- Leverage amplifies everything. The same force that can turn $5.6 billion into $14 billion in profit can also turn a profitable toy store into 33,000 lost jobs

The $53 million goodbye

Let's circle back to where this all started.

Ross Johnson lost the bidding war for RJR Nabisco. He didn't get to buy his company. His plan failed, his reputation was shredded, and he became the poster child for corporate greed in the 1980s.

He also walked away with $53 million.

The real winners of the RJR Nabisco deal were the investment bankers and lawyers who collected over $700 million in fees regardless of the outcome. The real losers, as is often the case, were further down the food chain - the employees who faced layoffs as the company struggled under its debt burden.

At Toys "R" Us, 33,000 people learned that lesson the hard way. At Twitter, thousands more.

And somewhere right now, a private equity firm is running the numbers on its next target. The deals are more conservatively financed than they were in 1988 - equity cushions have grown from 13% to closer to 35-40% - but the fundamental mechanics haven't changed. Borrowed money. Transferred debt. Someone else's risk.

The barbarians never really left the gate. They just got better suits and fancier spreadsheets.