2024: what lies ahead

Last month I talked about key news and events of 2023, and I thought it would be interesting to see what major financial institutions expect for 2024. So I spent hours going through almost FIVE HUNDRED pages of reports from big financial players and I distilled for you the key themes in this blog post.

One important consideration though. It’s always very hard to predict what’s going to happen one year ahead. And if this is normally true, it is even more true for 2024. We come from a period of great uncertainty, where even the "big boys" (e.g. Central banks or investment firms) did miss on accuracy. As example, expectations of having high inflation for a short period of time, or guaranteed recession for most countries didn’t materialize. And don’t get me started on market projections.

This article will not guarantee bullet-proof answers to questions like “Where should I invest in 2024?” or “How to get rich in 2024?”, however it will give you a good idea of what the "big boys" of investments and economy THINK will happen, hence it is a good starting point.

For reference, you can find all the links to the reports I went through at the bottom of the article.

Welcome to a new paradigm

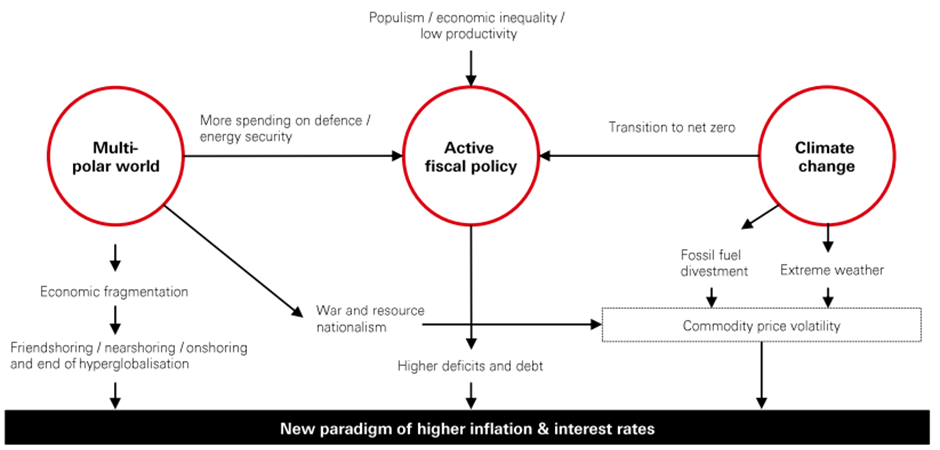

I liked a lot how HSBC framed what they think is a shift to a new paradigm for the macro economical landscape, which I report below.

The macroeconomic outlook for 2024 is defined by three key trends. Firstly, a shift towards a multi-polar and fragmented global order signifies the end of hyper-globalization. Secondly, there's a pivot to more active fiscal policies driven by political, environmental, and social concerns, moving away from the previous decade's austerity and monetary focus. Lastly, addressing climate change and transitioning to net-zero emissions is a central policy driver. These shifts imply increased supply-side volatility, with higher inflation and interest rates, and potentially more frequent economic downturns. These factors are critical in shaping long-term economic forecasts and capital market projections for the upcoming year.

Now let's dive deeper into what lies ahead.

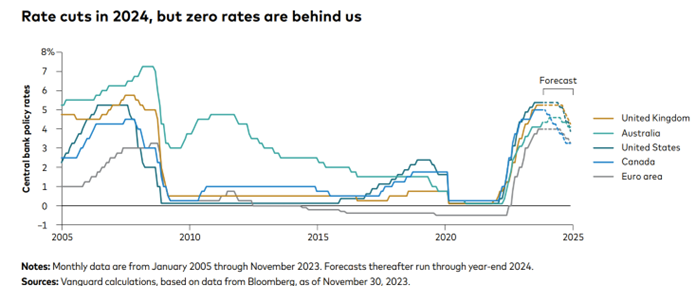

Inflation and monetary policy in 2024

Inflation is expected to continue its disinflation trend and fall within the 2% to 2.5% range by the end of 2024 hence approach central bank targets (that is around 2%). Structural changes will make it difficult to drive inflation back to its pre-pandemic average, which was below 2%.

Vanguard believes that the equilibrium real interest rate, often referred to as the neutral rate or r-star, has gone up. This rate is essentially the sweet spot for interest rates, where monetary policy is neither revving up nor putting the brakes on the economy. Think of it as the point where the amount people save perfectly matches the amount invested in the economy. According to research from Vanguard, this r-star has risen roughly by 1% (or 100 basis points) since 2008, reaching about 1.5% now. This means the current nominal interest rate is around 3.5% (that is 1.5% + 2% "ideal" inflation level). What pushed this level up is mainly an aging population (with less people working, and more retired people spending) and potential productivity gains from new technologies.

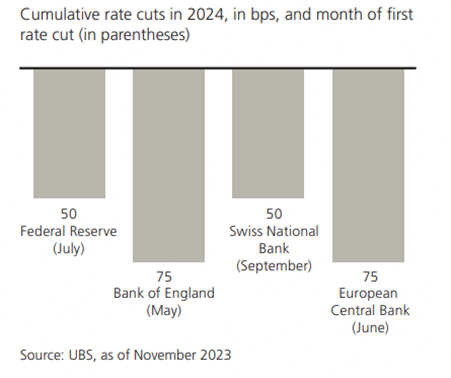

Central banks plan to cautiously transition to easing monetary policies, still keeping an eye on inflation though, to prevent a backfire.

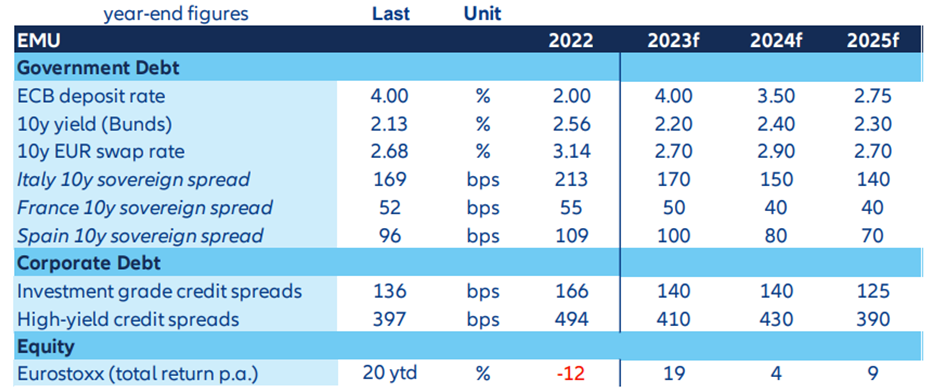

The Federal Reserve is expected to perform rate cuts only in the latter part of 2024. The baseline assumption is that real 10-year U.S. Treasury yields will reach approximately 2.3% by the end of 2024. The European Central Bank might act sooner given the sluggish economic growth in the Eurozone.

This shift in interest rates carries profound implications. For households, saving becomes more attractive due to higher interest rates, encouraging prudent consumption. Businesses will face higher borrowing costs, impacting smaller, more leveraged companies. Governments will need to reassess fiscal policies to tackle rising debt levels and ensure fiscal sustainability.

Economic growth and GDP

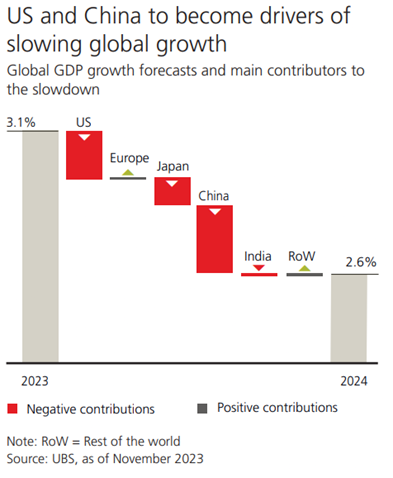

In 2024, the global economy, should remain resilient despite restrictive monetary policies. This has led to a brief period of below-trend growth, expected to improve in the second half of the year. With inflation normalizing, major economies should see real wage growth resuming. The labor market, especially in Europe, remains strong, with low unemployment despite the slow growth. Labor shortages are likely to persist, influenced by demographic changes and steady demand in various sectors. The overall economic outlook suggests a moderate downturn, followed by a recovery by late 2024 or early 2025.

US

In 2023, the U.S. economy displayed remarkable resilience, largely due to strong job growth and consumers' spend, tapping into the over $2.25 trillion of excess savings accumated during the pandemic. However, 2024 is set to experience a moderate slowdown (or soft-landing) with a projected growth rate of 0.7%, down from the 2.2% forecast for 2023. This deceleration is attributed to various factors, including slowing manufacturing, higher fuel costs, the end of student loan payment breaks, and increasing budget deficits. Financial normalization, with rising interest rates and tighter credit conditions, will further contribute to this slowdown. Despite this, there's an expectation of a recovery towards the end of 2024, as inflation aligns closer to the Federal Reserve's 2% target. This could revive consumer spending and stimulate economic recovery.

The U.S. dollar is expected to face depreciation due to adjustments in global interest rates and inflation. U.S. debt has also reached concerning levels, exceeding $33 trillion in 2023, , up more than $3 trillion during the year and $10 trillion since 2019. Despite these challenges, U.S. government bonds remain a safe haven, and U.S. companies continue to dominate globally. The real GDP growth is anticipated to slow down, impacted by reduced consumer savings and increased costs of debt financing.

Europe

In 2024, Europe's economic outlook is cautious, with a modest GDP growth forecast of 0.3%, mirroring the slow growth of 2023. Growth should finally resume in H2 but the EU level of GDP is estimated as €500bn below its pre-pandemic trend by mid-2024. This is mainly due to the European Central Bank's (ECB) restrictive monetary policy. Interest rate transmission in the Eurozone is swifter than in the United States as over 70% of Eurozone corporate funding is from banks (often at floating rates) versus ~80% of US corporate funding from debt markets (largely at fixed rates).

The Eurozone's economy has slowed since mid-2022, contrasting with the more resilient U.S. economy. The good news is that in the eurozone, inflation has surprised to the downside in recent months. The ECB usually lags the Fed in terms of policy turning points, but relatively poor economic performance could mean the pivot comes earlier.

UK

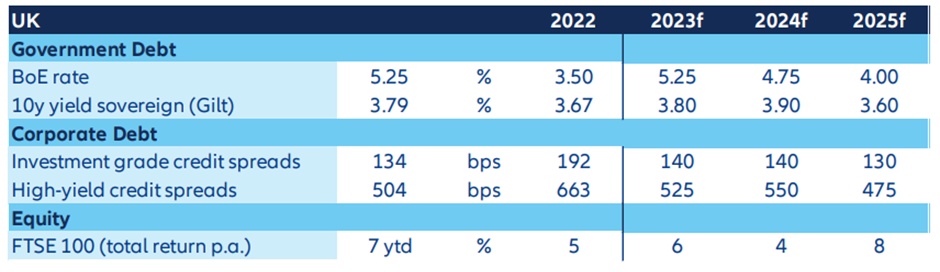

The United Kingdom is currently grappling with a multitude of challenges that have raised concerns both domestically and internationally. Despite avoiding a recession, similar to its Eurozone neighbors, the UK's economic situation remains precarious with a small margin for error. As consumers, businesses, and investors try to navigate this uncertainty, they are also faced with the prospects of a general election scheduled for the fourth quarter of 2024, unless snap elections are called earlier.

The Labour party, currently in opposition, is leading in opinion polls and seems poised for a potential victory. This prospect of a change in administration brings with it both hope and uncertainty. Election periods are often characterized by ambitious promises made by political parties, but these do not always translate into actual policy changes. The uncertainty fueled by these elections comes at a challenging economic time for the country.

One of the critical issues the incoming government will have to address is the nation's public borrowing, which is rapidly approaching 100% of GDP. This figure has doubled in the last 15 years, highlighting the severity of the fiscal situation. Given this backdrop, any additional public spending will likely not be financed through an increase in the deficit. This scenario suggests that higher taxes may be considered as a way to manage the economic challenges.

China

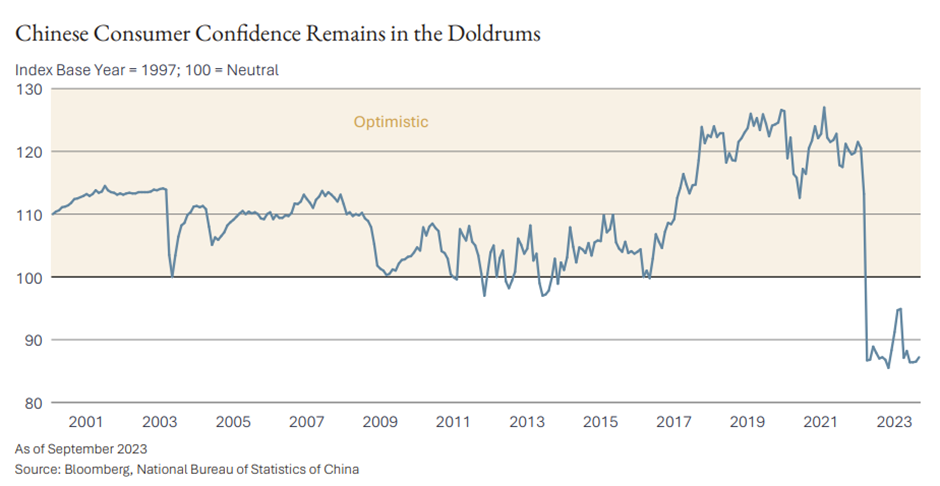

The macroeconomic outlook for China in 2024 presents a complex picture, shaped by a mix of challenges and strategic shifts. While the post-COVID reopening initially spurred optimism, this was tempered by subdued consumer confidence and significant problems in the real estate sector, which accounts for nearly a quarter of its GDP and 65% of household assets.

This has prompted various levels of government to introduce stimulative measures aimed at bolstering the economy. The era of over 6% annual growth appears to be in the past for China, with the economic growth for 2024 projected to be around 4.5% (down from 5.2% in 2023), with policy support playing a crucial role in sustaining this recovery. However, more policy support may be necessary, considering the ongoing downturn in the property sector, record-low consumer confidence, and limited fiscal and monetary policy interventions.

Interestingly, Beijing's shift in 2020 in its structural reforms under the 'dual circulation' strategy, favoring 'hard tech'(the production of hardware and components for strategic and high-tech industries ) over 'soft tech' (e-commerce development catering for non-strategic consumer demand) and leveraging the private sector for innovation, is expected to boost industrial migration inland and enhance productivity in the long term. China has also made notable strides in becoming a dominant player in critical strategic sectors like electric vehicles,transitioning from a net importer in 2019 to the largest net exporter in these fields in 2023. Similarly, China has embedded itself within the renewable energy supply chain.

However, China faces significant headwinds, including challenges in its export-driven economy due to slow global growth and trade tensions, a struggling domestic real estate sector, and a consumer focus on debt reduction rather than spending. The recently announced CNY 1 trillion bond issuance program could provide a modest boost to GDP growth(0.4-0.8%), but the focus is likely to shift towards consumer spending, leadership in carbon transition, and industrial supply chain upgrades for long-term, sustainable growth.

Japan

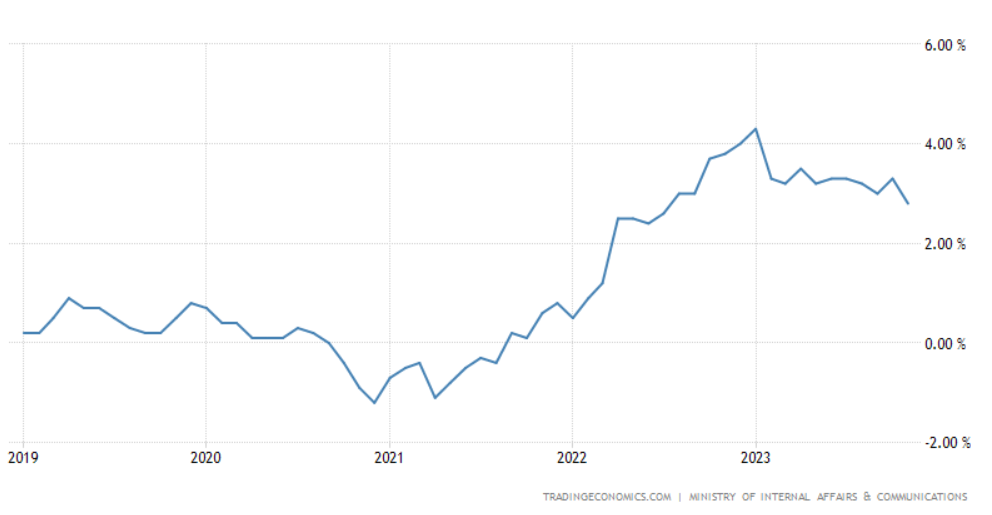

As the Japanese economy transitions out of deflation, a key development is the Bank of Japan's anticipated move away from its long-standing yield curve control policy. This shift is expected to occur around mid-2024, aligning with the country's departure from negative interest rates.

This economic transformation in Japan is underscored by a noteworthy change: the nation is experiencing higher and more sustained inflation for the first time in many decades. Several factors contribute to this inflationary trend. A notable one is the tight labor market, which has been consistently exerting pressure on wages. This labor market condition is not just a short-term phenomenon but appears to be increasingly entrenched. This dynamic is expected to be particularly evident in the spring of 2024 during the Shunto wage negotiations, a critical period for labor agreements in Japan. These negotiations are likely to result in further considerable wage increases, reinforcing the inflationary trend.

Emerging markets

In 2024, emerging markets (EMs) are poised for economic recovery, or a "re-emergence" in the global economic landscape. This will be marked by widespread interest rate cuts and improved current account balances. Central banks in regions like Latin America and Eastern Europe are initiating these cuts, while Asian EMs, excluding China, are expected to follow suit in the latter half of the year. This development is set to lower the yields of EM sovereign bonds, with a forecasted decrease from the current 6.6% to 5.6% by the end of 2025.

Despite this optimistic outlook, a degree of fragmentation within EMs is anticipated, with varying growth rates across regions. Resilient growth in EMs has been maintained, despite the challenges of inflation and currency protection. The central banks in these markets had preemptively raised rates, and now with easing inflation, are leading the cycle of rate reductions.

Interest rates, post these adjustments, are likely to stabilize at higher levels than pre-hiking cycles for an extended period.

GDP growth in EMs for 2024 is expected to outpace developed markets, with an overall growth of around 4%, led by emerging Asia at about 5%, and emerging Europe and Latin America at 2%-2.5%.

India is projected to be a standout performer with a growth rate slightly dipping from 6.6% in 2023 to 6.0% in 2024. The upcoming elections are crucial, as predictions indicate that the Indian economy could double in size by the decade's end, significantly outpacing the projected 20% growth for the European economy in the same timeframe.

Geopolitical

In 2024, the global geopolitical and economic landscape is undergoing significant transformation, influenced by a variety of factors:

Political landscape and elections:

The upcoming US presidential election is drawing significant attention, with speculation about a Biden-Trump rematch and polls suggesting a close race. The results will have implications for Ukraine aid, foreign policy predictability, and the rule of law.

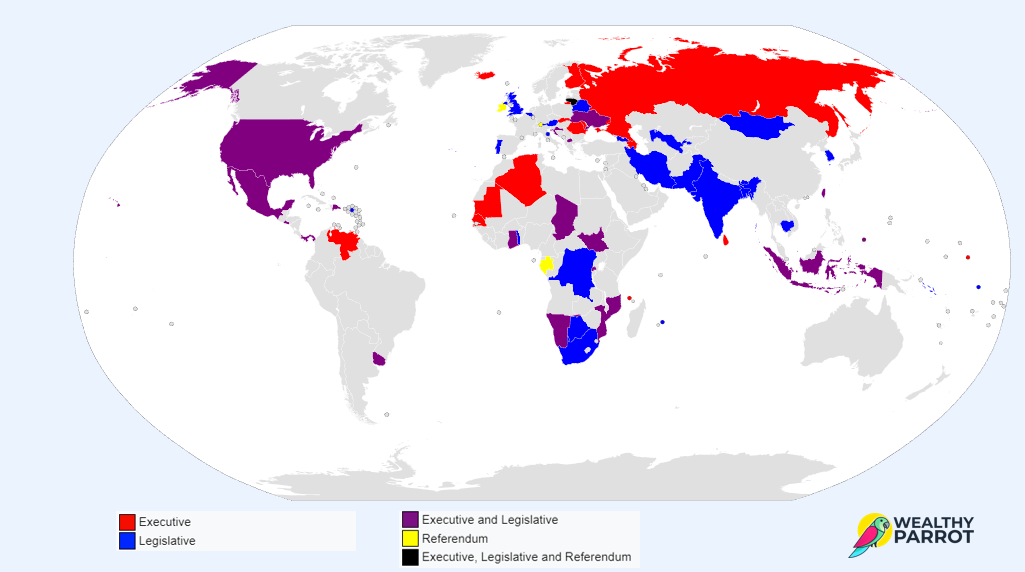

US is not the only nation going to the polls though, as 64 countries (plus the European Union) that make up almost 60% of global GDP will undergo decisive elections, causing uncertainty. This uncertainty, akin to a negative supply shock, compounds the challenges posed by recent events like the pandemic and energy crises.

Populism is at a historic peak, with over a quarter of nations governed by populist leaders. Populist governance often correlates with lower GDP per capita over time, reduced judicial independence, and challenges to election quality and press freedom.

In Europe, rising inflation and immigration issues have fueled right-wing populism, raising concerns about the next European Parliament's stance on environmental and immigration issues.

Friend-shoring trend:

There's a notable shift in production and trade patterns, moving away from China towards countries closer to the United States, both geographically and geopolitically. This change is driven not just by rising labor costs in China, but also by ideological differences and geopolitical considerations. Mexico has overtaken China as the largest trading partner of the US, indicating a reorientation of global trade dynamics. Emerging economies, especially those in close proximity to the US, are benefiting from this trend. These economies also offer comparative advantages and strong trade complementarity with the US and EU, particularly in global value-chain trade.

Geopolitical concerns and conflicts:

Ongoing conflicts such as the Israel-Hamas War, the Russia-Ukraine War, and US-China trade tensions present substantial risks to financial markets.

The global pandemic has sustained high levels of risk and uncertainty. The Russian invasion of Ukraine, Middle East tensions, and Taiwan straits issues add to this uncertainty, affecting global markets, supply chains, and consumer behavior.

Where to invest in 2024

A couple considerations before we start. What I said in the beginning about making predictions, is VERY RELEVANT when it comes to forecasting which asset class will grow, a.k.a. where to invest. So please take all the below with a pinch of salt, and use it more as indication of what all the reviewed investment firms THINK will happen, rather then putting all your money right away there. Many reports I read did offer specific views on certain assets - which I have not included (but feel free to read the reports). Also, I did find divergent views on some asset classes, therefore I decided to keep the predictions at a fairly high level. Alright, let's begin!

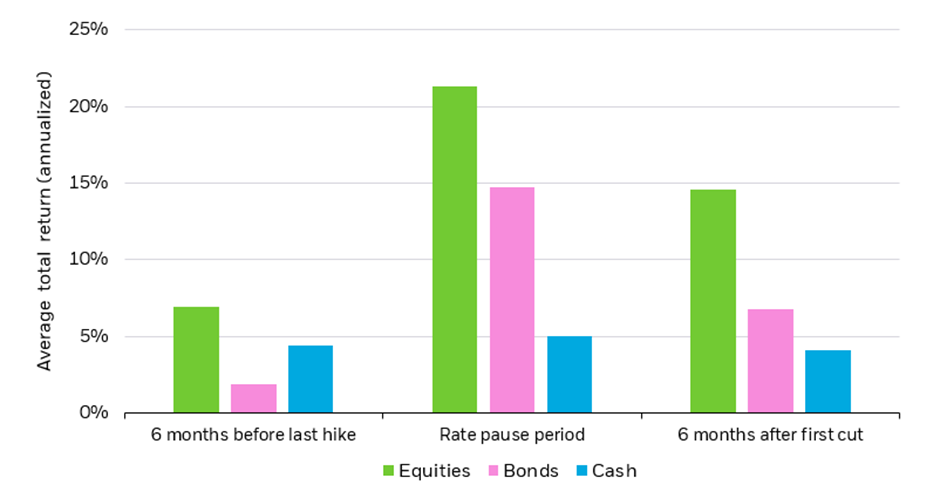

Let's begin by looking at the US. Since 1990, across the past five cycles of interest rate increases, the Federal Reserve typically waited an average of 10 months from its final hike to its initial rate cut. Historically, both stock and bond returns have been more favorable during this pause phase compared to the periods right after the first rate cut, as shown in Figure 2.

In all the reports I read, "quality" assets was a recurrent choice. For stocks this means companies with a strong free cash flow, robust balance sheets, high interest coverage, and healthy real revenue growth. A proxy for these stocks, the MSCI ACWI Quality Index. When it comes to bonds, quality means 5 years duration, both high grade (government) and investment grade.

Stocks

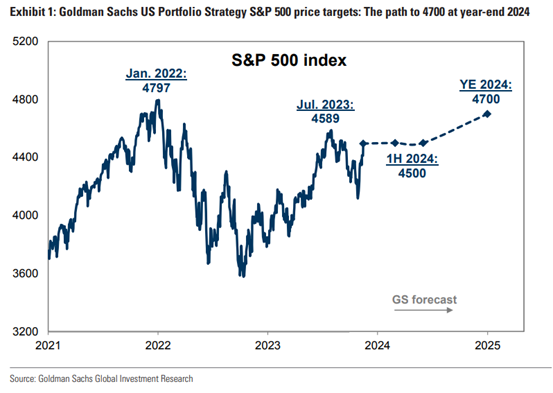

The market outlook for the S&P 500 in 2024 is cautiously optimistic, with an expected modest increase to 4700, indicating a 5% year-over-year growth and a 6% total return including dividends. This growth could be influenced by potential Federal Reserve interest rate cuts.

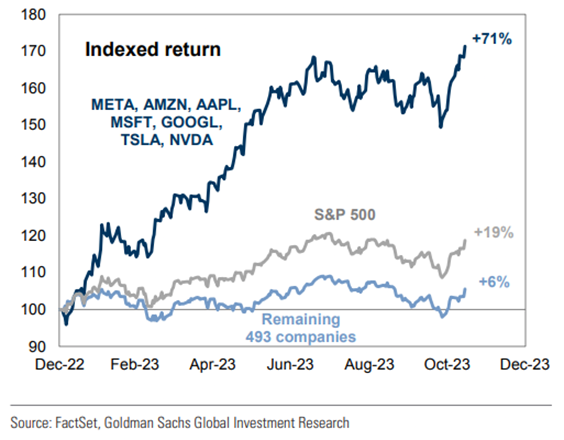

Central to this outlook is the continued dominance of the "Magnificent 7" mega-cap tech stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla), which significantly impacted the market trends in 2023 and are expected to outperform in 2024, despite a high-risk profile due to elevated expectations.

A notable shift is anticipated from the creators to the adopters of Artificial Intelligence (AI), suggesting a broader impact across industries. Investment focus is trending towards companies with strong financial health markers like robust cash flow and high interest coverage. The Magnificent 7 are predicted to lead in growth, maintaining their significant influence on the market.

Bonds

As interest rates continue their declining trend, bond yields, which were previously seen as the peak expectation of total returns, are now considered more as a baseline. This shift implies that investors could benefit from price appreciation in addition to interest income, especially as falling rates (--> expect bond yields to fall) typically lead to rising bond prices.

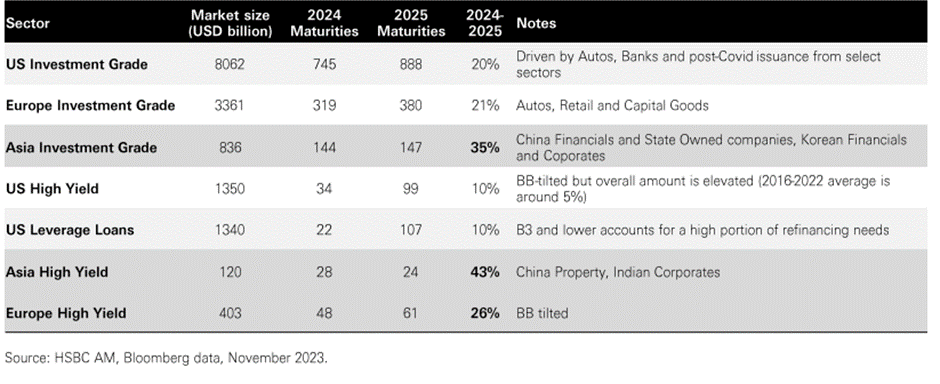

In the U.S., the Investment Grade maturity wall is anticipated to grow by 21% in 2024, reaching $136 billion. This increase is predominantly driven by the banking sector, largely due to heightened regulations and the Basel III framework. Additionally, the non-financial sector is seeing increased maturities, partly a result of the substantial Covid-related market issuance during 2020 and 2021.

In contrast, the maturity outlook in European investment grade and high yield markets seems more manageable. However, certain sectors within the high yield market, such as automotive, chemicals, retail, and real estate, may face increased stress. Post the record issuance phase of 2020 and 2021, fueled by the low-rate environment and the ECB Corporate Sector Purchase Programme, supply softened in 2022 but has shown signs of recovery in 2023, with expectations of continued recovery in 2024. Most companies, both in the investment grade and high yield categories, maintain strong liquidity and committed credit lines, though some deterioration in credit metrics is anticipated.

Commodities

The 2024 investment outlook for commodities is cautiously optimistic but emphasizes strategic caution. Gold remains a stable, risk-mitigating asset in portfolios, yet there's a trend towards investing risk elsewhere. The ongoing commodity bull super-cycle has pushed prices to decade highs, but gains are expected to slow in 2024 due to economic factors. Commodities like copper may outperform, especially with strong demand from China, while oil prices are predicted to remain stable, influenced by OPEC+ supply control and a disciplined approach from U.S. producers. Gold, facing challenges such as a stronger U.S. dollar and rising interest rates, has held its value well and could rally in 2024 as its headwinds reverse.

Investors are advised to prepare for market volatility due to geopolitical uncertainties, using diversification and capital preservation strategies. Oil and gold are seen as viable options for hedging portfolios against geopolitical risks, with opportunities in oil market investments or energy stocks, especially for those with higher risk tolerance. The overall approach for 2024 combines careful commodity selection with an emphasis on risk management in a complex economic and geopolitical environment.

A closing note on the green revolution

The investment outlook for 2024 is heavily focused on tackling climate change and biodiversity loss, with a shift from traditional returns to sustainable, long-term impacts. Key areas include:

- Renewable energy: a significant increase in solar and wind power capacity is needed, offering mature and emerging investment opportunities.

- Energy grids: upgrading grids for zero-carbon sources will require substantial investment, rising from $260 billion in 2020 to $820 billion by 2030.

- Energy storage: diverse storage solutions are needed for grid resilience and vehicle power.

- Building renovation: efficient heating and cooling, notably through heat pumps, are crucial in modernizing buildings.

- Nature-based solutions: investing in protecting, managing, and restoring ecosystems is an emerging field for climate mitigation.

This evolving investment landscape presents opportunities to not only grow portfolios but also contribute positively to the global environmental future.

Phew! This was a wild ride! I wish you a prosperous 2024, happy investing!

References

The used reports to compile this post:

- Allianz Global Economic Outlook 2023-25

- BNP Paribas Investment outlook 2024

- Barclays Outlook 2024

- Charles Schwab 2024 Market outlook

- Deloitte Banking Industry outlook 2024

- Deutsche bank Outlook for 2024

- Fidelity Outlook 2024

- Goldman Sachs 2024 US Equity Outlook

- HSBC 2024 Investment outlook

- Invesco 2024 investment Outlook

- iShares 2024 Investment strategy

- Lazard Global outlook 2024

- Morgan Stanley 2024 investment outlook

- UBS Investment Strategy 2024

- Vanguard Market outlook 2024

- Wells Fargo 2024 outlook