The IPO trap: why 'Getting in on the ground floor' usually means getting trampled

On May 18, 2012, Facebook went public in the most anticipated IPO in a decade. Retail investors - regular people with brokerage accounts - snapped up 26% of the shares offered.

What those regular people didn't know was that Facebook had quietly told its largest institutional investors that second-quarter revenue would be lower than expected. Morgan Stanley's lead analyst cut the company's 2012 revenue forecast from $5.04 billion to $4.85 billion - but that revision was shared verbally with institutional clients, never printed in the prospectus. The big players adjusted their bets. Some pulled out entirely. Others shorted the stock on day one.

The small investors? Nobody told them anything.

By September - four months later - the stock had fallen 50% from its IPO price. Facebook shareholders had lost tens of billions in market value, according to The Washington Post. The stock wouldn't recover to its IPO price for over a year. Nasdaq paid a $10 million penalty for technical failures on the first trading day. Federal and state regulators launched investigations into whether large investors got key information not available to everyone else.

Welcome to the Initial Public Offering - the financial event that sounds like an invitation but works more like a velvet rope.

If that sounds like ancient history, look at June 12, 2026. SpaceX went public in the largest IPO ever: shares priced at $135, roughly $75 billion raised, a valuation near $1.8 trillion. Retail investors placed more than $100 billion in orders. The stock popped 19% on its first day. But almost none of those retail buyers paid $135 - they bought in the open market at $160 and up. The velvet rope Facebook strung up in 2012 had just found a much bigger stage.

What an IPO actually is

When a private company wants to become a public company - meaning anyone can buy and sell its shares on a stock exchange - it goes through an IPO. The company sells shares to investors for the first time, raises a pile of cash, and in return gives up a slice of ownership to the public.

Sounds democratic. In practice, it's anything but.

Here's how it actually works, step by step.

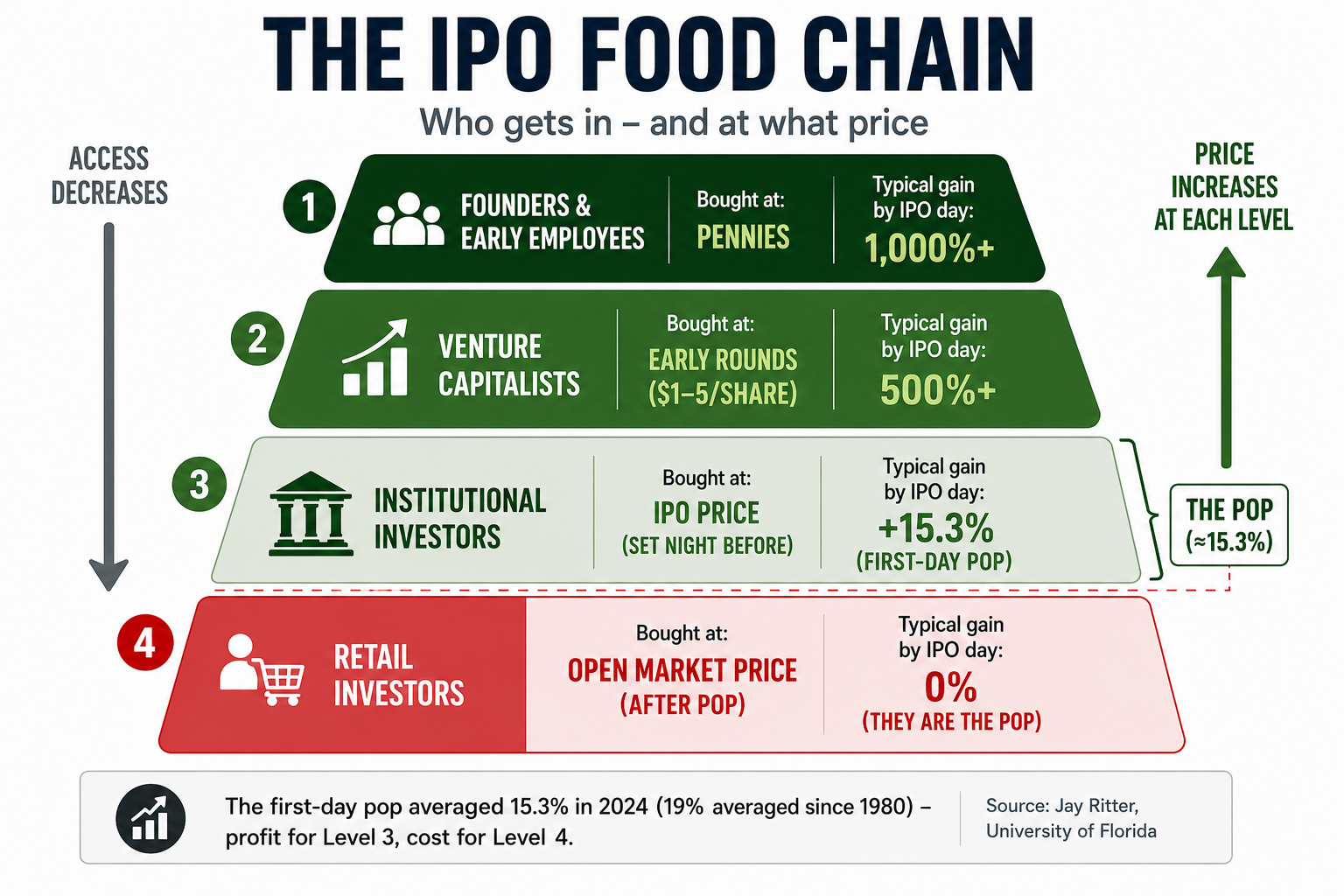

The company hires investment banks. Before a single share trades, the company picks one or more investment banks to manage the process. These banks are called underwriters, and landing this role is incredibly lucrative. The selection process is informally called a "bake-off" - each bank pitches its valuation estimate, marketing strategy, and connections to big investors.

The banks go on a roadshow. The underwriters and company executives spend weeks traveling to meet institutional investors - pension funds, hedge funds, mutual funds, sovereign wealth funds. They present the company's financials, growth story, and why this stock is worth buying. Notice who's in the room: institutions with billions to deploy. Not you.

The banks build the "book." During the roadshow, institutional investors place orders at various prices. This process is called book building, and it tells the underwriters exactly how much demand exists and at what price. Think of it as a private auction where the richest bidders set the terms.

The price is set the night before. Based on the book, the company and lead bank agree on the final offering price and - critically - who gets how many shares. The lead bank controls this allocation, and there's no rule saying it has to be fair.

Trading opens. You can finally buy. The next morning, the stock starts trading on the exchange. This is the first moment a regular investor can purchase shares. But by now, the price has usually jumped well above the offering price. The institutions who got in at the IPO price are already sitting on profits.

Fun fact: The typical fee for underwriting an IPO is 5-7% of the total money raised. On a $1 billion IPO, that's $50-70 million - split among the banking syndicate, with the lead bookrunner taking the most prestigious (and largest) cut.

The first-day pop: a feature, not a bug

You've probably seen the headlines. "Company X surges 40% on first day of trading!" It sounds like everyone is getting rich. But the people getting rich are the ones who bought at the offering price - which was set the night before, in a room you weren't invited to.

This surge has a name: the first-day pop. And it's not an accident.

According to data from Jay Ritter, a leading IPO researcher at the University of Florida, the average first-day return was 15.3% in 2024 and 11.9% in 2023. Across the full record - every US IPO since 1980 - the average day-one pop is 19%. During the dot-com bubble of 1999-2000, it ballooned to a staggering 65%.

That 15.3% sounds like free money. And it is - if you got the IPO allocation. For institutional investors who received shares at the offering price, the first-day pop is essentially a gift from the underwriters. They buy at $20, the stock opens at $23, and they can sell immediately for a quick profit. Or they hold, knowing they got in at a discount.

If you're buying on the open market that morning, you're buying at $23 - after the pop has already happened. You're the demand that makes the pop possible.

SpaceX is the textbook case. On June 12, 2026, institutions bought at the $135 offering price. The stock opened at $150, touched $176 in intraday trading, and closed at $160.95 - a 19% first-day gain that pushed the company's market value past $2 trillion. The institutions holding $135 shares were up 19% before lunch. The $100 billion in retail orders? Most got filled in the open market at $160 and above. They didn't catch the pop. They were the pop.

Fun fact: In 1999, VA Linux went public at $30 per share and closed its first day at $239.25 - a 698% pop, still one of the largest in history. The institutions that got allocated shares at $30 made nearly 8x their money in hours. The stock was below $9 within a year.

Why do underwriters deliberately set the price low enough to create a pop? Three reasons.

First, it makes the banks look good. A stock that pops 20% on day one generates positive headlines and grateful institutional clients. A stock that drops on day one generates lawsuits and angry phone calls.

Second, it rewards the banks' best clients. During the dot-com era, the practice of "spinning" made this explicit: investment banks gave executives of prospective client companies guaranteed IPO allocations as a sweetener to win future underwriting business. Credit Suisse First Boston maintained so-called "Friends of Frank" accounts - named after tech banker Frank Quattrone - that funneled hot IPO shares to Silicon Valley executives. The SEC eventually cracked down, but the underlying dynamic persists in subtler forms. The institutions that get generous allocations are the same ones that generate the most trading commissions for the bank throughout the year.

Third, it creates buzz. A successful IPO generates media coverage that helps the stock's narrative. The company doesn't mind leaving some money on the table if it means a strong debut and a rising stock price in the weeks that follow.

As a 2025 analysis from 3040 Wealth noted, all market participants - companies, venture capitalists, and investment banks - are aligned around getting deals done, even at the cost of leaving money on the table. The question is: whose table?

The money you leave on the table (and the money that disappears)

The first-day pop is just the beginning of the story. What happens after day one is where retail investors really get hurt.

Recent research shows how lopsided the outcome is. A 2025 study of US IPOs from 2012 to 2021 found that the IPOs which let ordinary investors buy in at the offer price underperformed other IPOs from the same period by roughly 20 percentage points in their first year. The deals retail could actually get into did worse than the ones they couldn't.

Jay Ritter's original research puts this even more bluntly: for every dollar invested in IPOs at the end of the first trading day, investors had just $0.83 after three years. A dollar invested in a matched portfolio of similar-sized companies over the same period grew to $1.62. Same dollar, same time period, dramatically different outcomes.

Burton Malkiel puts the long-term number more starkly still: IPOs underperform the total stock market by 4 percentage points per year over five years, according to the academic studies he cites in A Random Walk Down Wall Street.

Fun fact: During 1999-2000, nearly $67 billion was "left on the table" by IPO issuers. Many of the IPOs with the biggest first-day pops - 300% or more - had lost over 90% of their value by December 2002. The bigger the pop, the harder the fall.

Four percent per year might not sound catastrophic. But compounded over five years, it means a $10,000 investment in an average IPO would be worth roughly $2,000 less than if you'd just bought a simple index fund.

A 2026 analysis from The Motley Fool put hard numbers on the first year specifically: among the 15 largest US IPOs since 2006, the average stock fell about 50% at some point during its first 12 months, and finished that year roughly 33% below its IPO price. Nasdaq's own research team reached the same conclusion from the other direction - more than 70% of tech companies underperform the market after going public. The headline debut is the high point, not the starting line.

Why do IPOs underperform so consistently? Several forces are at work.

Companies go public at peak hype. The whole point of the roadshow is to maximize excitement. Companies time their IPOs for when their growth story sounds most compelling - which is often right before growth slows down.

Insiders are selling, not buying. An IPO is fundamentally a transaction where people who know the company best are selling their shares to people who know it least. Founders, early employees, and venture capitalists have been waiting years for this exit. They're not selling because they think the stock is cheap.

The lock-up expiration creates a second crash. Insiders typically can't sell their shares for 90 to 180 days after the IPO - a restriction called the lock-up period. When that window opens, a flood of insider selling often pushes the price down further. It's a predictable supply shock that hurts anyone who bought during the hype phase.

Retail attention drives overpricing. A 2025 study published on SSRN by Gempesaw, Henry, Pisciotta, and Xiao found that retail IPOs had lower earnings-to-offer price ratios - meaning they were more aggressively priced. The study found that higher pre-IPO Google search activity and greater post-IPO fractional trade volume (a proxy for retail interest) both predicted worse long-term performance. The more retail investors wanted a stock, the worse it performed.

Fun fact: During the dot-com bubble, the total "money left on the table" - the gap between what companies raised and what they could have raised if priced at the first-day closing price - was nearly $67 billion in 1999-2000 alone, according to Jay Ritter's IPO data. During that same era, many of the IPOs with the largest first-day gains - including those that popped 300% or more - had lost more than 90% of their value by December 2002, according to analysis of Ritter's IPO data.

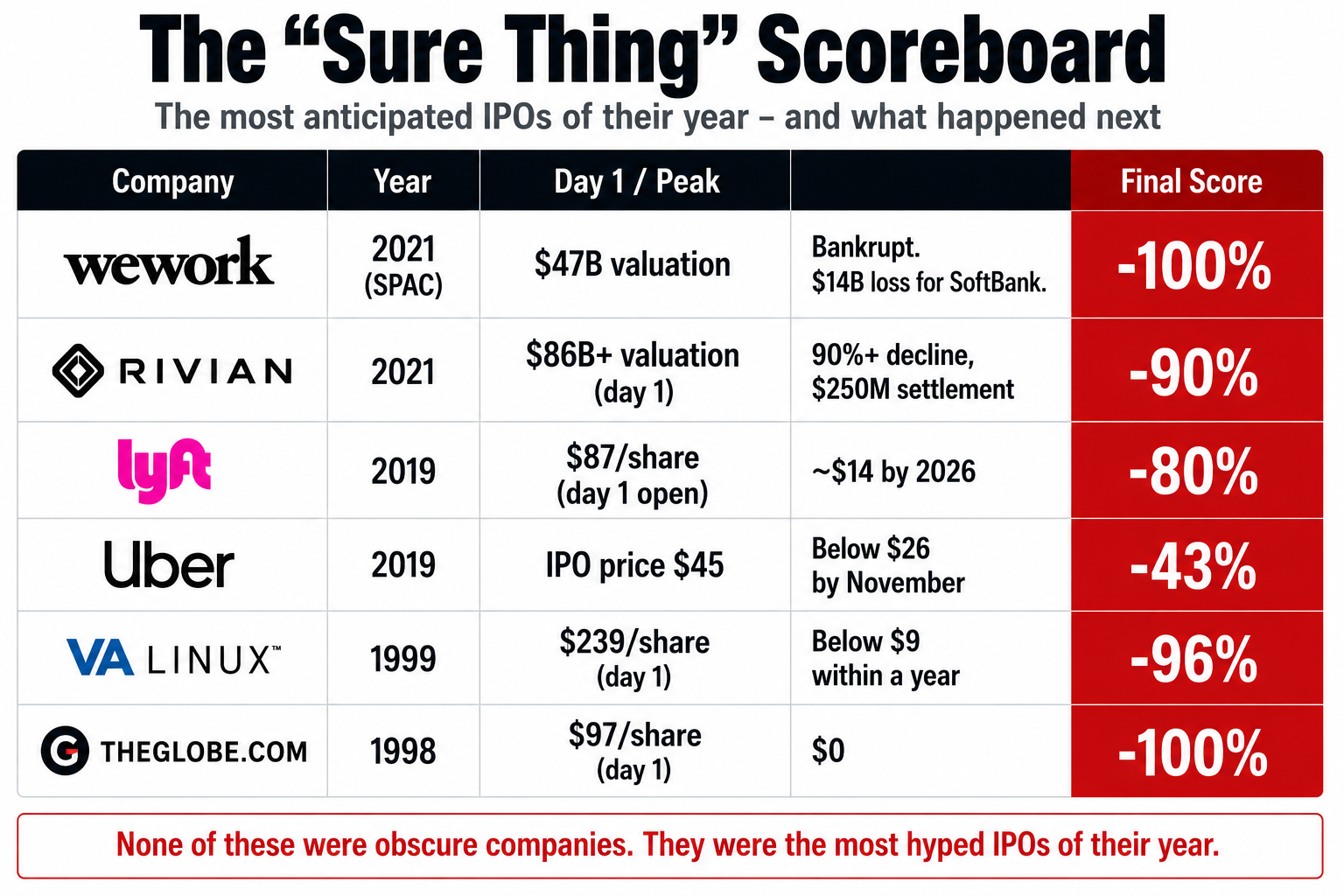

The graveyard of "sure things"

The data is damning enough in aggregate. The individual stories are worse.

WeWork (2019 - never made it). Adam Neumann built a coworking empire valued at $47 billion by SoftBank. The company filed for its IPO in August 2019, and the prospectus revealed staggering losses ($1.9 billion on $1.8 billion in revenue in 2018), questionable self-dealing (Neumann had leased buildings he personally owned back to WeWork and even charged WeWork $5.9 million for the trademark "We" - a fee he was later forced to return after public outrage), and a corporate structure that gave him near-absolute control. The IPO was pulled. WeWork eventually went public via SPAC in 2021 at a $9 billion valuation - an 80% discount from its peak. By November 2023, it filed for bankruptcy with $18.6 billion in debt. SoftBank told investors its cumulative loss on WeWork exceeded $14 billion, according to CNBC.

Rivian (2021). The electric truck maker went public at a valuation of $66.5 billion - surging past $86 billion on its first day of trading, briefly surpassing Volkswagen's market cap despite having delivered fewer than 1,000 vehicles. By spring 2024, the stock had sunk to single digits, representing a decline of over 90% from its post-IPO high. In 2025, Rivian agreed to pay $250 million to settle a lawsuit alleging it had concealed vehicle pricing problems in its IPO disclosures. The company has since shown improvement (reporting its first full-year gross profit of $144 million in 2025), but anyone who bought near the IPO is still deep underwater.

Lyft (2019). The ride-sharing company priced its IPO at $72 per share, opened at $87 on day one, then entered a long decline. Within months it was trading around $50 - a 43% drop from its opening-day high. It reported a loss of $644 million that quarter. As The Washington Post reported, Lyft's collapse "sent a cautionary message to other unicorns." By early 2026, the stock was trading around $14 - down nearly 80% from its IPO price.

Uber (2019). Priced its IPO at $45 in May 2019 and promptly fell below $26 by November - a decline of more than 40% - posting a $5.2 billion quarterly loss along the way.

None of these were obscure companies. They were the most anticipated, most covered, most hyped IPOs of their respective years. And in every case, the retail investors who bought early got the worst of it.

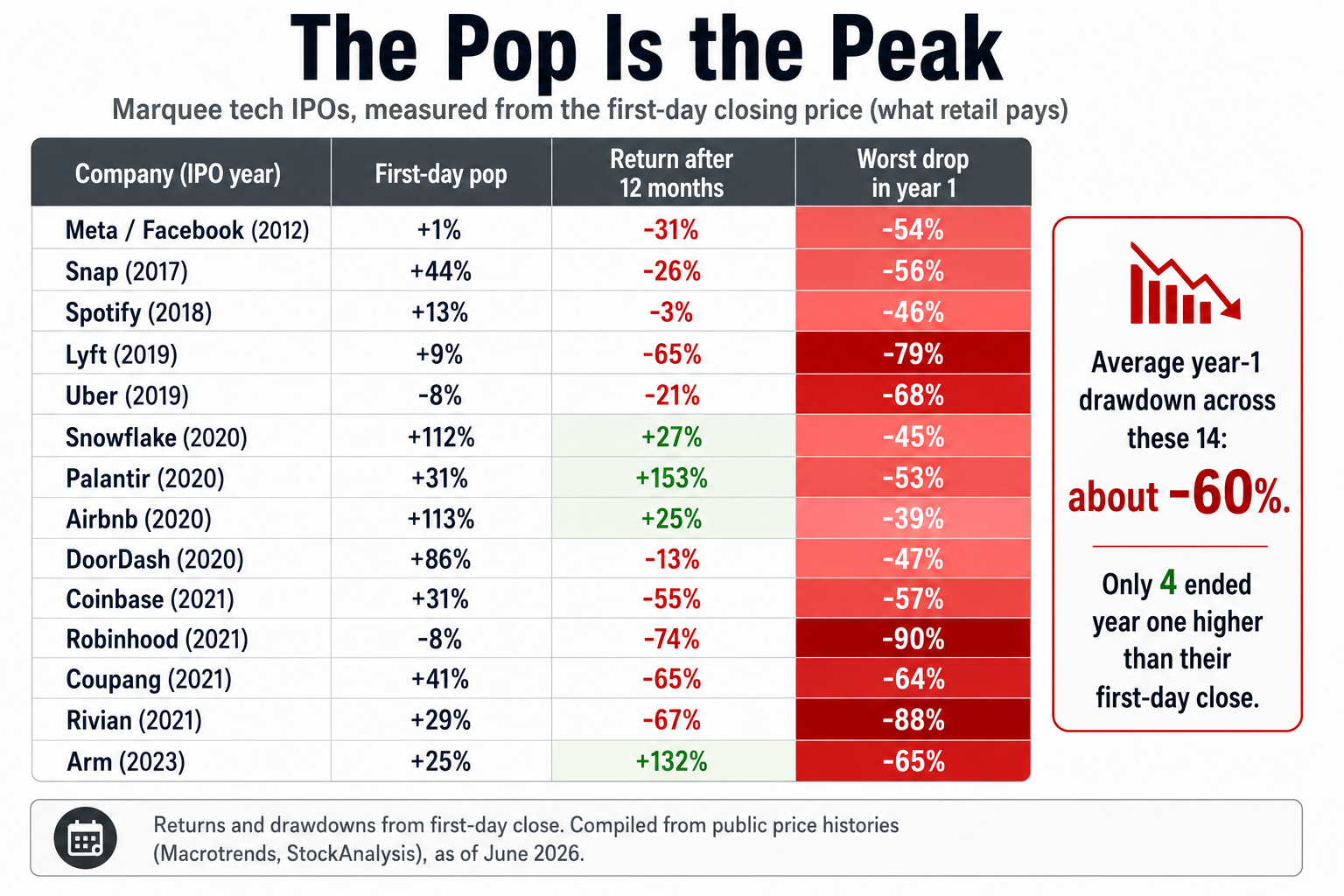

The pop is the peak

Line up fourteen of these debuts side by side and the pattern stops being anecdotal. The table below tracks marquee tech IPOs from the price retail investors actually pay - the first-day closing price, not the insider's offer price. The "first-day pop" column is the insider's reward. The two columns after it are what everyone who bought at the close lived through.

*Direct-listing reference price (Spotify, Palantir, Coinbase), not a traditional offer. Returns and drawdowns measured from the first-day closing price; "worst drop in year 1" is the largest peak-to-trough decline within the first 12 months. Compiled from public price histories (Macrotrends, StockAnalysis), data as of June 2026.

Read that last column again. Even the eventual winners - Snowflake, Palantir, Arm - put their first-day buyers through a 45% to 65% drawdown before paying off. Across these fourteen names, the average worst-case drop in the first year was about 60%, and only four of them were higher 12 months after their debut. The pop you saw in the headline was, more often than not, the best price the stock would see for a long time.

The 300-year-old scam that still works

The pattern isn't new. Not even close.

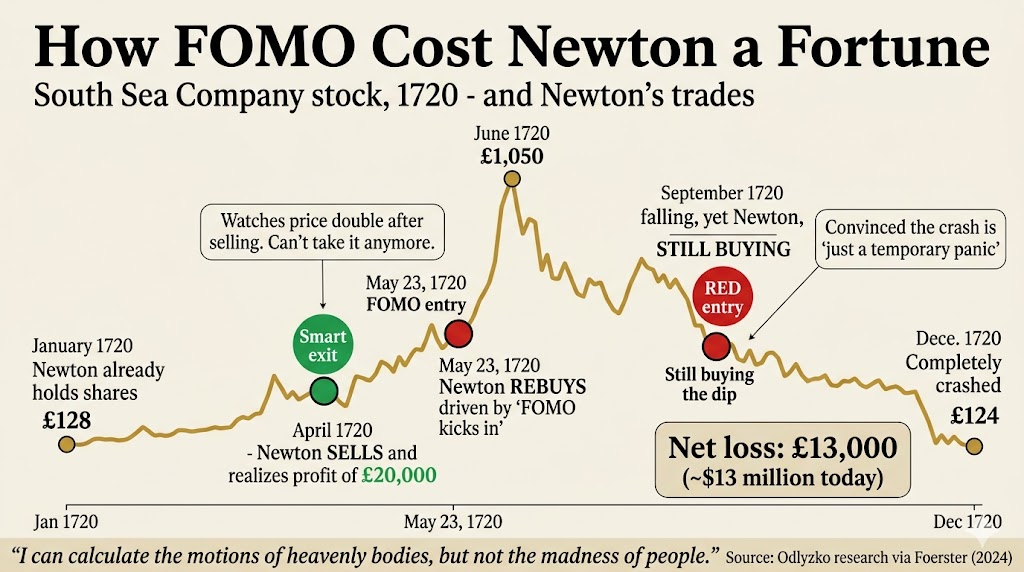

In 1720, during the South Sea Bubble in England, speculative mania was so intense that dozens of brand-new companies launched to capitalize on the frenzy. Charles Mackay catalogued 86 of them in his classic Extraordinary Popular Delusions and the Madness of Crowds. The offerings ranged from the mundane ("For supplying London with sea-coal") to the absurd ("For a wheel for perpetual motion") to the genuinely iconic: company number 17 on the list was described only as "For carrying on an undertaking of great advantage, but nobody to know what it is." The promoter sold shares on a deposit of just £2 per £100 share, raised his target amount in a single morning, and vanished.

That same year, South Sea Company stock rose from £128 in January to over £1,000 by summer. John Blunt, the company's founding director who orchestrated the scheme, operated by two maxims: "advancing by all means the price of the stock" and "the more confusion the better," as Edward Chancellor documents in Devil Take the Hindmost. The confusion worked - even savvy professionals at the Bank of England rushed in.

Then it all collapsed. By December, the stock was back to £124.

Isaac Newton - arguably the smartest person alive at the time - was among the casualties. According to research by mathematics professor Andrew Odlyzko, who uncovered Newton's actual trading records, the story is more painful than the popular version suggests. Newton held South Sea stock early and sold around April 1720 for a profit of roughly £20,000. Smart trade. But then he watched the price double in weeks. On May 23, gripped by what we'd now call FOMO, he poured all his profits - and proceeds from selling his other investments - back into South Sea stock. He kept buying through September, even as the price was in free fall, apparently convinced the crash was "just a temporary irrational panic."

The round trip cost Newton £13,000 (roughly $13 million today). He reportedly said he could "calculate the motions of heavenly bodies, but not the madness of people."

Fun fact: Newton still died rich in 1727, with an estate valued at £30,000. But as Stephen Foerster notes in Trailblazers, Heroes, and Crooks, the primary reason he died rich was that he was already rich before his South Sea misadventure. As the saying goes, the easiest way to make a small fortune is to invest a large fortune in the latest craze.

The difference between 1720 and 2026 is that today's promoters wear better suits and file with the SEC. The "undertaking of great advantage, but nobody to know what it is" now comes with a 200-page prospectus, a valuation model, and a CNBC interview.

Why this matters to you

You might be thinking: "I'd never fall for a South Sea Bubble." Fair enough. But consider how many times you've seen a headline like "Biggest IPO of the year!" and felt a twinge of excitement. That twinge is the same force that's been separating regular investors from their money since the 1700s.

Research by Anagol, Balasubramaniam, and Ramadorai - highlighted in the 2025 book Fixed: Why Personal Finance Is Broken by Campbell and Ramadorai - found that investors in India who were randomly allocated IPO shares through a lottery system, and whose shares happened to go up, reacted by trading furiously in other stocks. They mistook luck for skill. Getting "chosen" for a winning IPO didn't make them better investors. It made them overconfident ones.

The system is designed to make you feel like you're being let in on something special. In reality, the special access went to institutional investors weeks ago. By the time the stock hits the exchange, the insiders' profits are already baked in. (If you've noticed similar patterns in how your brain handles money decisions, you're not alone - these biases are well-documented.)

This doesn't mean every IPO is a disaster. Some companies - Apple, Google, Amazon - went on to deliver extraordinary returns after their IPOs. But those are survivorship bias at work. For every Amazon, there are dozens of companies that peaked on day one and spent the next five years proving that their IPO price was the most expensive ticket in the house.

The academic evidence is overwhelming. Malkiel summarizes decades of research: buying IPOs is "one of the easiest ways to lose money." Ritter's data shows consistent underperformance across thousands of offerings. The SSRN study confirms that retail attention predicts worse outcomes. The pattern holds across eras, industries, and market conditions.

If you want exposure to a company that just went public, the math suggests a simple strategy: wait. Let the hype fade, the lock-up expire, and the insiders sell. Then, if the company's fundamentals still look good at a lower price, consider buying. Or better yet, buy an index fund that will automatically add the stock once it's proven itself - no first-day FOMO required. (If you want to understand how these financial dynamics work on a company's books, our Accounting 101 guide breaks down the statements that reveal a company's real financial health.)

Even the cheerleaders are doing this math. Days after the SpaceX debut, The Motley Fool ran the historical averages and concluded that a $10,000 stake bought at the first-day price could be worth under $5,300 a year later - and flagged that SpaceX listed at roughly 115 times sales, the kind of valuation that leaves nowhere to go but down. The most exciting IPO of the decade and the most sober advice point in the same direction: there's no prize for being early.